[ad_1]

Vithun Khamsong/Second through Getty Photos

As I method my sixty fifth birthday in a few days my ideas flip to my very own well being (which remains to be good, fortuitously!) and the state of worldwide healthcare for the reason that finish of the worldwide Covid-19 pandemic. Though the pandemic prompted plenty of injury and compelled everybody to consider the significance of fine healthcare much more than they did earlier than the pandemic, it has additionally sparked a flurry of innovation and medical analysis that was unprecedented previous to 2020. And though the healthcare sector of the inventory market didn’t carry out very properly in 2023, it seems that prospects for outperformance in 2024 are trying encouraging. Actually, to this point in January, the healthcare sector is essentially the most bullish of all in response to a latest BofA international fund supervisor survey. In the second week of January, the healthcare sector noticed the biggest quantity of internet shopping for previously 5 months, in accordance to Goldman Sachs.

In search of Alpha

For buyers with a longer-term horizon, the healthcare sector reveals promise with an ageing inhabitants that’s dwelling longer in each developed international locations and in lots of growing nations resulting in an ever-growing demand for improved healthcare. In keeping with this latest perception from fund supervisor, abrdn, the cell and gene remedy trade presents particularly promising progress alternatives:

The cell and gene remedy trade is ready to develop at a compound annual progress fee of 34% from 2021-2027. The US Meals and Drug Administration predicts that it will likely be approving some 10 to twenty cell and gene remedy merchandise every year by 2025, in comparison with a complete of simply 21 as of September 2021.

One instance of this latest innovation and a promising progress alternative is represented by the introduction of the brand new GLP-1 class of medicine to deal with weight problems and diabetes. The preliminary outcomes have been really exceptional and supply a complete new class of medicine to probably influence a large space of illnesses past weight reduction because of the cardiovascular and renal advantages of the incretin drug remedy. Actually, some Wall Road analysts predict that the market dimension for this class of medicine might exceed $100B.

Immediately, GLP-1s are utilized by round 10-12% of T2D sufferers within the U.S. “We mannequin GLP-1 utilization increasing to round 35% of diabetics within the U.S. in 2030 and wouldn’t be shocked to see upside to this quantity, particularly as outcomes information continues to emerge,” Schott famous. “As well as, we forecast that round 15 mn overweight sufferers can be on GLP-1s by the top of the last decade.” Total, whole GLP-1 customers within the U.S. could quantity 30 mn by 2030 – or round 9% of the inhabitants.

The GLP-1 market is at present dominated by 2 gamers – Eli Lilly (LLY) and Novo Nordisk (NVO). And whereas the present drug pipeline is totally stocked and growing internet gross sales for each firms, new AI-based drug discovery strategies supply the potential to additional improve the analysis and growth of safer and simpler new medication. Actually, the success of the GLP-1 medication led to LLY changing into the biggest drug maker by market cap (at present $565B), surpassing JNJ final 12 months.

Healthcare CEFs

Making an attempt to choose one or two robust healthcare shares to spend money on will be difficult. As a long-term investor taken with income-producing investments together with some capital appreciation, I’ve discovered that well-managed CEFs can supply excellent returns when bought at an acceptable low cost and when the fund is actively managed to reply to market whims.

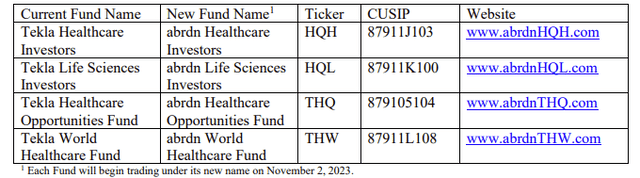

For these long-term buyers taken with reaching a sexy return on a healthcare fund, a closed-end fund that invests in healthcare firms could also be a very good possibility. Traders in CEFs could also be accustomed to the title abrdn, but when you weren’t already conscious, the 4 healthcare funds previously managed by Tekla Capital Administration have been acquired by abrdn in October 2023. These 4 funds are proven within the desk from the press launch, and though the names modified the ticker symbols didn’t.

abrdn

Whereas every of the 4 funds has its execs and cons, THQ and THW supply month-to-month dividends whereas HQH and HQL pay quarterly. On this article, I’ll give attention to abrdn Healthcare Alternatives Fund (NYSE:THQ), which I really feel is properly positioned for the longer term with its prime holdings in healthcare and the promise of robust returns within the sector, whereas the fund trades close to its historic low cost.

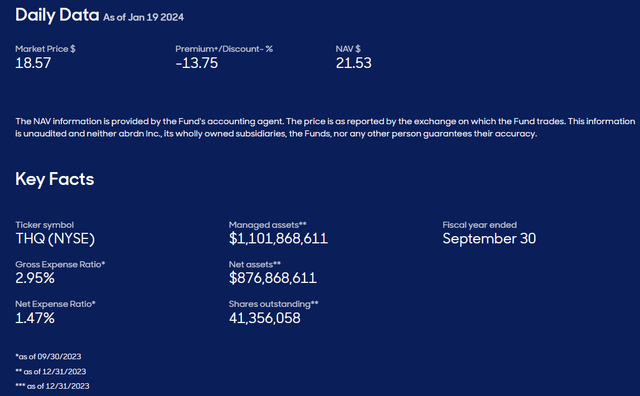

Listed below are some key information concerning the fund from the web site:

abrdn web site

The THQ fund is at present buying and selling at a reduction of -13.75% as of market shut on January 19. That’s near the widest low cost that the fund has seen previously 5 years. That low cost has simply began to slim over the previous few weeks even because the NAV has begun to rise once more from its October 31 low.

CEFconnect

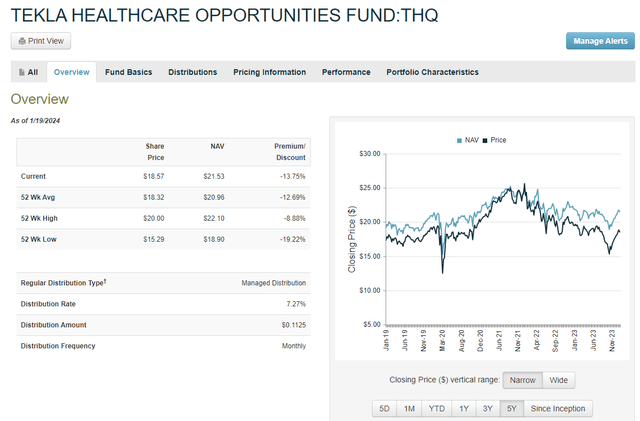

Whereas THW presents the next yield (about 11%), the full return from THQ has been even higher than THW over the previous one-year interval with a optimistic 2.5% whole return in comparison with -5.5% for THW, in addition to over the previous 3 years at 7.9% for THQ vs -2.3% for THW. Nevertheless, for brand spanking new buyers who wish to the longer term, previous returns are solely useful in realizing what beforehand occurred however don’t predict what’s going to occur. Let’s take a more in-depth have a look at the portfolio holdings for THQ to attempt to decide what the longer term returns may appear to be.

THQ High Holdings

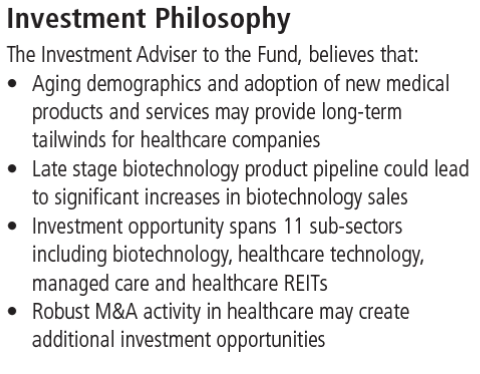

In keeping with the fund’s Annual Report, THQ employs a flexible progress and revenue technique throughout all sub-sectors of the healthcare trade and throughout the complete capital construction (each fairness and debt). The funding philosophy of the fund is defined:

abrdn

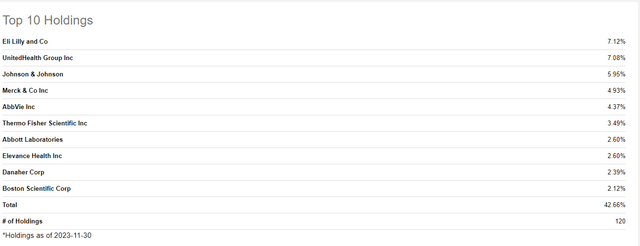

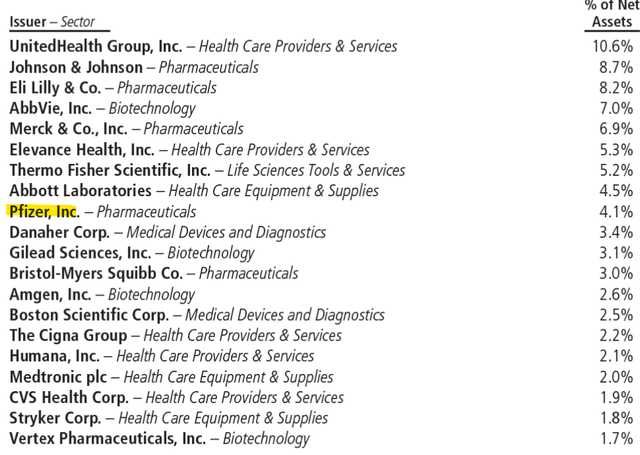

As of 11/30/23 the highest 10 holdings within the fund characterize almost half of the full portfolio and embrace many main firms within the healthcare trade.

In search of Alpha

As of the top of November, LLY was the fund’s prime holding which is smart given the inventory’s momentum and progress prospects from the GLP-1 medication described above. UnitedHealth (UNH) is one other prime holding that has carried out very properly over the previous 5 years and delivered stable outcomes for Q423 when it reported earnings final week.

Managed care bellwether UnitedHealth exceeded Wall Road forecasts with its financials for This fall 2023 on Friday because the group’s quarterly earnings per share rose ~16% YoY regardless of rising prices in its insurance coverage arm and Optum enterprise.

JNJ is subsequent up on the checklist of prime holdings at almost 6% of the portfolio worth. At a market cap of almost $390B it’s a Dividend King and will get principally Purchase scores from analysts regardless of struggling over the previous 12 months because of lawsuits over talc-based child powders.

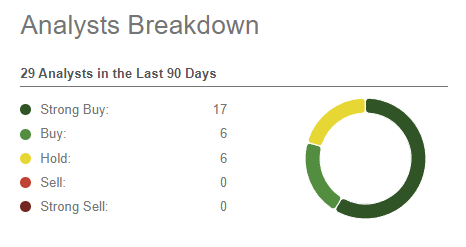

Merck & Co. (MRK) is one other $300B market cap pharmaceutical firm with good potential for robust returns. Actually, 17 Wall Road analysts fee MRK a Sturdy Purchase, whereas 6 fee it a Purchase and 6 give it a Maintain ranking.

MRK scores from Wall Road (In search of Alpha)

The fifth-largest holding at almost 4.5% is AbbVie (ABBV). With a market cap of about $290B, ABBV can be extremely rated by Wall Road analysts with 8 Sturdy Purchase, 8 Purchase, and 13 Maintain scores.

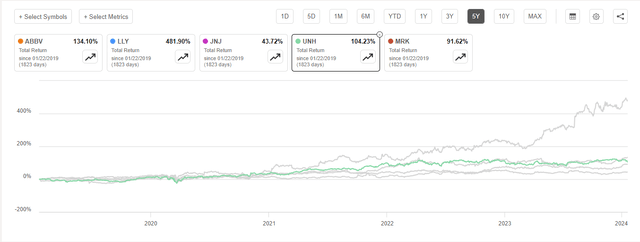

Taking a look at outcomes for the highest 5 holdings over the previous 5 years, solely JNJ has a complete return of lower than 90% over that timeframe. The latest bounce in LLY inventory has propelled that inventory to generate the best return with most of that bounce coming within the second half of 2023.

In search of Alpha

Distributions and Protection

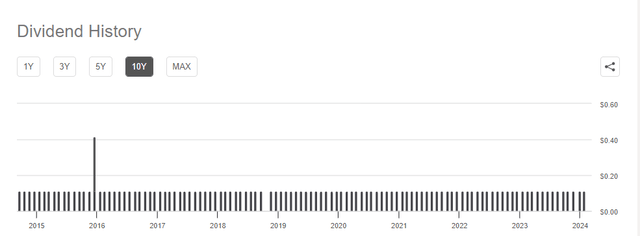

Much like different CEFs that I’ve just lately written about, the Tekla funds make use of a managed distribution coverage that gives a stage distribution to shareholders whatever the internet revenue or capital positive aspects acquired from the fund’s investments. Within the case of THQ, the month-to-month distribution has remained the identical for the reason that inception of the fund in 2014 (aside from a particular dividend paid in December 2015).

In search of Alpha

From the most recent part 19 discover issued on January 10, 2024, that is the reason for that coverage:

Every Fund has adopted a distribution coverage to supply buyers with a steady distribution out of present revenue, supplemented by realized capital positive aspects and, to the extent crucial, paid-in capital.

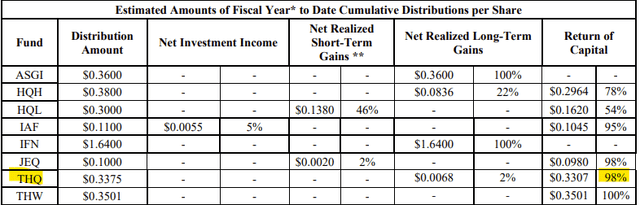

Sadly, within the case of THQ the quantity of ROC (return of or “paid-in” capital) is sort of 100% YTD for the reason that finish of the earlier fiscal 12 months on 9/30/23.

abrdn

The place the estimated quantities above present a portion of the distribution to be a “Return of Capital,” it implies that Fund estimates that it has distributed greater than its revenue and capital positive aspects; subsequently, a portion of your distribution could also be a return of capital. A return of capital could happen for instance, when some or all the cash that you simply invested in a Fund is paid again to you. A return of capital distribution doesn’t essentially mirror the Fund’s funding efficiency and shouldn’t be confused with “yield” or “revenue.”

For at the least the previous 3 months, the fund has not been incomes the 7% distribution that it has been paying out and that may be a concern going ahead. That concern might also clarify why the low cost has continued to stay traditionally huge if buyers worry a dividend reduce is forthcoming. This isn’t an encouraging pattern and is particularly unlucky given the latest robust efficiency of the fund’s prime holdings throughout that point.

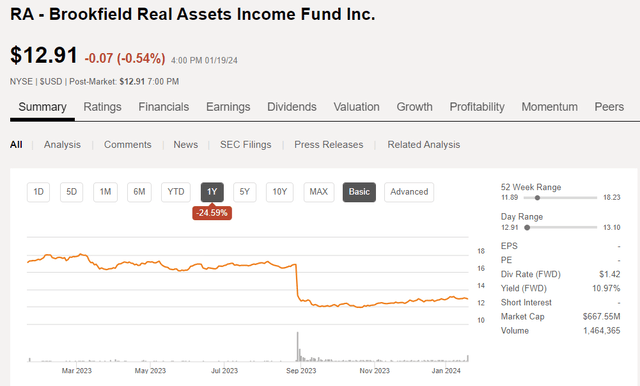

Though a distribution reduce might not be the worst end result, it will seemingly have the impact of inflicting an excellent greater improve within the low cost and an enormous drop within the worth of the fund. That’s primarily what occurred final 12 months with the RA fund from Brookfield when that fund reduce its distribution after paying the identical month-to-month quantity for the 7 years up till it reduce final 12 months. The worth of the RA fund dropped dramatically and has not since recovered.

In search of Alpha

Abstract and Conclusion

Whereas the healthcare sector struggled to maintain tempo with the remainder of the market in 2023, the THQ fund that was managed by Tekla till October when abrdn took over additionally had a troublesome time overlaying the regular month-to-month distribution as evidenced by a considerable amount of ROC in the newest distributions.

abrdn Annual Report

Modifications to the highest holdings will be seen when reviewing what the highest holdings have been as of 9/30/23 from the fund’s Annual Report, in comparison with what the highest holdings at the moment are (as of 11/30/23, which is the most recent that I might discover). For instance, Pfizer is now not a prime holding the place it was greater than 4% of internet property again in September. Moreover, there’s much less focus within the largest holdings with no single holding representing greater than 7.5% now in comparison with UNH making up greater than 10% of internet property beforehand.

As 2024 unfolds and the healthcare sector is demonstrating a robust restoration with good prospects going ahead it stays to be seen whether or not THQ can proceed to pay out the identical month-to-month distribution of $0.1125 that it has paid for almost 10 years now.

I’m cautiously optimistic about the way forward for THQ given its robust place inside the healthcare trade as represented by the fund’s prime holdings and abrdn has confirmed to be a very good fund supervisor. However I fee the fund a Maintain given the massive quantity of ROC in the newest distributions and want to see the fund efficiency enhancing for a number of extra months earlier than being motivated to start out a brand new place. If one at present holds shares of THQ, the worth, and NAV tendencies are encouraging and I’d not be seeking to promote shares at the moment, particularly as healthcare reveals indicators of restoration in 2024.

[ad_2]

Source link

{kind=link}