[ad_1]

Torsten Asmus

November final 12 months, I wrote an article on Vanguard Excessive Dividend Yield ETF (NYSEARCA:VYM) making a case to keep away from investing on this ETF. The explanation was easy – elevated danger of incurring an disagreeable alternative value by deploying capital into this particular car.

What I imply by alternative value is an inadequate yield unfold relative to the S&P 500 to compensate buyers for de-emphasizing progress names. On prime of this, there’s additionally a component of an elevated danger that stems from introducing a extra pronounced tilt in direction of greater yielding shares.

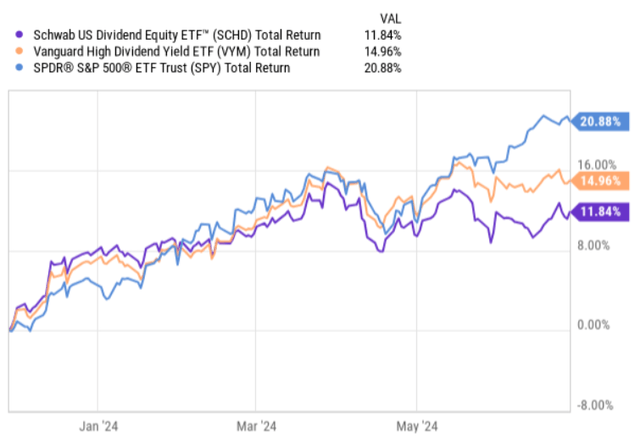

Nonetheless, for the reason that publication of my article, VYM has delivered moderately stable returns, outperforming a broadly common ETF – Schwab U.S. Dividend Fairness ETF (NYSEARCA:SCHD) -, which has an reverse technique as VYM (i.e., progress and never yield centered).

Ycharts

But, in comparison with the S&P 500 itself each VYM and SCHD have lagged behind by a comparatively first rate margin.

With this in thoughts seeing that VYM has managed to register fairly acceptable returns and likewise considering a number of adjustments the general market situations, let’s assessment the thesis to find out whether or not VYM has grow to be a extra attractive ETF to contemplate.

Thesis assessment

All in all, whereas VYM has certainly demonstrated a stable efficiency, I nonetheless don’t see a justified rationale to speculate on this ETF. There are three main factors I want to emphasize on this context.

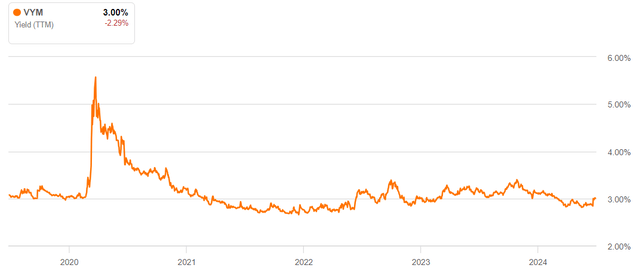

First, if we have a look at the yield unfold between, for instance, VYM and SCHD it has turned damaging of ~ 60 foundation factors. Particularly, the expansion oriented SCHD, which invests in strong companies that embody robust progress potential presently yields 3.6%, whereas VYM, which is inherently a excessive yield centered ETF supplies solely 3% in yield.

Along with this, the prevailing dividend yield of VYM is sort of according to its 5-year historic common (adjusted for the momentary surge in the course of the early moments of COVID-19).

Looking for Alpha

Provided that the rates of interest at the moment are materially greater than earlier than 2022 rendering the yields of many prime quality names far more enticing, accepting a 3% yield by way of an ETF, which per design is supposed to seize irregular dividend streams, whereas not dropping the give attention to massive cap names appears as suboptimal selection.

Second, and that is considerably of an enlargement of the earlier comparability to SCHD, we now have to grasp that by coming into into VYM, a component of alternative value comes into play. I’d divide this into two classes:

The overarching subject is that there are simply too many prime quality and better yielding options on the market. For instance, relying on the maturity section we give attention to, investing in risk-free charge devices buyers can entry way more predictable yields that provide extra enticing present earnings streams of round 120 – 220 foundation factors. The extra particular subject is expounded additionally to the foregone potential in relation to the underlying dividend progress. Theoretically, one may make an argument that it’s value investing in VYM (and sacrifice some yield) because it supplies rising distributions that over time can compensate the buyers. Nonetheless, the historic 5-year and even 10-year dividend CAGR of VYM is barely at ~6%, whereas for SCHD (which presently affords greater yield) the related determine stands at roughly 12%.

Third, the rate of interest outlook has grow to be more and more extra unsure than in comparison with the time when my article was issued. Again then, the market had a robust conviction that there will likely be at the least a number of rate of interest cuts in 2024 that will rapidly cut back the financing prices and thus chill out the strain on the money flows of capital intensive companies. Now we’re speaking about one or two cuts this 12 months that will then be adopted by extra ones in 2025, thereby steadily bringing the general rate of interest degree to ~ 3% territory.

FOMC; St. Louis Fed

Nonetheless, we must always take these projections with a grain of salt and recognize the chance that we are going to not expertise such a normalization in rates of interest any time quickly (or that it’s going to happen slower than what’s presently baked into the cake).

For VYM these sort of dynamics don’t bode nicely.

The main motive is that VMY is closely tilted in direction of capital intensive companies that carry notable quantities of debt on their books with out having that important progress consider place. This might be simply implied by the truth that there’s solely 11.7% publicity to expertise names, and that the High 10 is generally dominated by established pharma, power and monetary corporations.

The underside line

In a nutshell, VYM nonetheless stays a suboptimal funding selection that’s principally defined by the dearth of clear benefit that will come from being invested on this ETF.

Theoretically, VYM is structured to place a heavier emphasis on excessive yielding dividend names with out stepping out of the S&P 500 universe. The logic tells that the dividend that buyers may entry right here must be comparatively enticing, particularly contemplating the considerably lowered publicity in direction of excessive progress expertise names.

But, the precise scenario is that the dividend provided by VYM is much from being attractive and even decrease than progress centered ETF automobiles like SCHD present. On prime of this, the bias in direction of worth and comparatively greater yielding names throughout the S&P 500 area comes with a significant alternative value of not with the ability to take part within the upside that will probably be pushed by the S&P 500 progress oriented corporations.

On account of this, I nonetheless don’t see a justified foundation for going lengthy Vanguard Excessive Dividend Yield ETF.

[ad_2]

Source link