[ad_1]

On the time of this writing on Could 17, 2024, with the VIX at an all-time low for the yr at 11.98, I’d say this can be a good time for the double diagonal – so long as it’s configured accurately.

Contents

Configuring the double diagonal is just not a trivial process.

It’s because the double diagonal is essentially the most versatile four-legged choice unfold ever invented.

It has at the very least six levels of freedom.

The double diagonal consists of promoting a put choice and promoting a name choice at a near-term expiration.

Then it has an extended put and an extended name at an extra dated expiration.

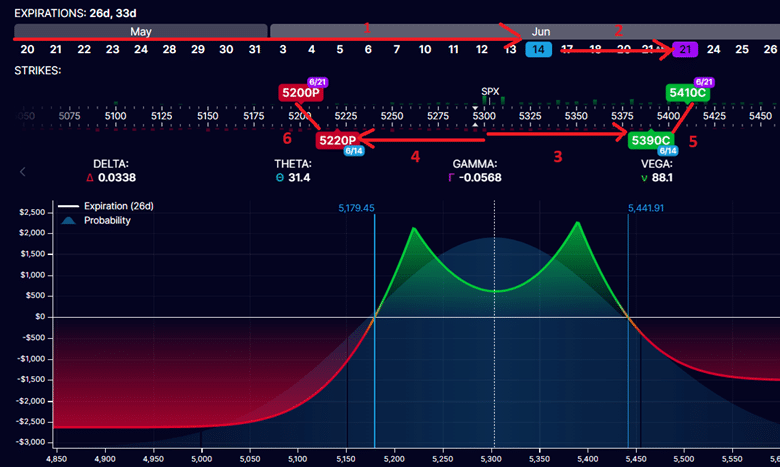

Take a look at the next double diagonal on the SPX when it trades across the 5300 on Could 17.

Purchase one Jun 21 SPX 5410 callSell one Jun 14 SPX 5390 callSell one Jun 14 SPX 5220 putBuy one Jun 21 SPX 5200 put

The P&L graph on the near-term expiration of Jun 14 seems like this:

What is good about modeling the double diagonal in OptionStrat is that we are able to simply drag the brief and lengthy places and calls round and see how the graph and the Greeks change.

Word that the online Greeks proven is just not accessible within the free model of OptionStrat.

There are six variables for me to regulate and play with:

The time until the near-term expiration (on this case, 26 days)

The time distinction between the near-term and far-term expiration (on this case, one week)

The strike worth of the brief name (5390)

The strike worth of the brief put (5220)

The width of the brief name to the lengthy name (on this case, 20 factors)

The width of the brief put to lengthy put (additionally 20 factors)

It’s typical that the wing width (on this case, 20 factors) is similar for the calls and the places.

What’s all the time a given is that the lengthy choices all the time expire later than the brief choices, just like that of calendars.

For the double diagonals, we’re contemplating immediately, the lengthy put and the lengthy name strike costs are additional away from the SPX worth than the brief put and brief calls.

Nevertheless, they don’t have to be.

For the brand new practitioners of the double diagonals, you need the expiration graph to be pretty symmetrical; they need to look just like the above, making certain that the graph’s middle curvature doesn’t dip under the zero-profit horizontal.

The double diagonal commerce is a market-neutral technique the place we would like the underlying worth to be range-bound, ideally between the 2 expiration graph peaks.

Entry 9 Free Possibility Books

For the superior practitioners of double diagonals, you need to think about volatility and the vega/theta ratio.

Double diagonals have constructive theta and generate earnings through the passage of time.

The double diagonals that we’re contemplating immediately all have constructive vega, though it’s attainable for double diagonals to have detrimental vega.

The quantity of constructive vega represents the quantity of volatility publicity (or danger) within the commerce.

Theoretically, if volatility will increase, the commerce ought to revenue (if all different elements stay unchanged).

If volatility decreases, this is able to damage the P&L.

On this sense, the bigger the vega, the better the volatility danger.

But when the volatility of the SPX, as indicated by the VIX, is at an all-time low, then the dealer can cause that volatility won’t drop a lot decrease.

Therefore, much less hazard of volatility dropping and hurting the P&L.

That is precisely why double diagonals are a very good commerce when volatility is low.

Another excuse is that the choices’ implied volatility, extrinsic worth, and worth are associated.

When volatility is low, the implied volatility of the choice is low.

This impacts the extrinsic worth of the choice and the value of the choice.

Each can be decrease.

As a result of the value of choices is decrease, it’s okay to spend cash to purchase extra extrinsic worth choices.

That’s the reason we’re shopping for the lengthy name and the lengthy put, which have additional expirations.

We’re keen to spend cash to purchase these choices with extra time.

Word that the double diagonal is comparable in construction to the iron condor, besides that the lengthy name and lengthy put are at an extra expiration.

Within the iron condor, they’re on the identical expiration because the brief choices.

As a result of the lengthy name and lengthy put of the double diagonal are additional dated, they’re extra highly effective and supply extra safety.

As such, we’re keen to deliver the decision and put spreads nearer to the cash.

We like to put the brief choices of the double diagonal round 25 to 35 delta on the choice chain.

In the meantime, they’re usually on the 10 to fifteen delta within the iron condor.

We will study a couple of issues concerning the double diagonal configuration variables by enjoying with the six double diagonal.

1. Reducing the time until expiration will increase the theta. This usually reduces the vega/theta ratio as a result of theta is now getting large enough to compensate for vega.

2. Growing the time distinction between the near-term and far-term expiration will increase the vega volatility publicity. It has the impact of accelerating the vega/theta ratio.

3. Transferring the decision unfold additional away from the present worth will increase the expiration breakeven level.

4. Transferring the put unfold additional away from the present worth will increase the expiration breakeven. The trade-off is that it decreases theta barely.

5. Growing the width of the decision wing decreases the vega/theta ratio.

6. Growing the width of the put wing decreases the vega/theta ratio. In impact, you’re shifting the lengthy put additional away from the cash. It turns into much less highly effective, and the vega is decrease.

By understanding how every of those six knobs impacts the Greeks, we are able to tune every knob to get the Greeks that we would like.

As we advance in our apply of choices, we begin to take volatility into consideration (not simply worrying about delta as we used to once we had been simply beginning).

By realizing the volatility of our underlying, we are able to resolve how a lot volatility publicity we need to give the double diagonal.

When volatility is low, as within the case now when VIX is low, we’re keen to provoke a constructive vega double diagonal commerce on the SPX, realizing that volatility shouldn’t go a lot decrease.

We will tolerate the next vega/theta ratio when volatility is low.

Some double diagonals can have vega/theta ratios as excessive as 8.

When volatility is excessive, and there’s a good chance of dropping, a vega/theta ratio of even 5 might symbolize an excessive amount of of a volatility danger for some merchants.

In that case, they’ll dial down the vega/theta ratio to 2 or 1 and even much less.

Some might even configure a double diagonal to have detrimental vega in the event that they really feel that volatility will drop.

As configured above in our instance double diagonal, its vega/theta ratio is 2.8, calculated by 88.1 / 31.4 = 2.8

The double diagonal is a complicated technique.

If all that is too complicated, don’t fear.

Examine the iron condor first.

Then, the double diagonal is the following stage up.

We hope you loved this text on the double diagonal.

In case you have any questions, please ship an electronic mail or go away a remark under.

Commerce protected!

Disclaimer: The data above is for instructional functions solely and shouldn’t be handled as funding recommendation. The technique offered wouldn’t be appropriate for traders who will not be aware of alternate traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.

[ad_2]

Source link