[ad_1]

carterdayne

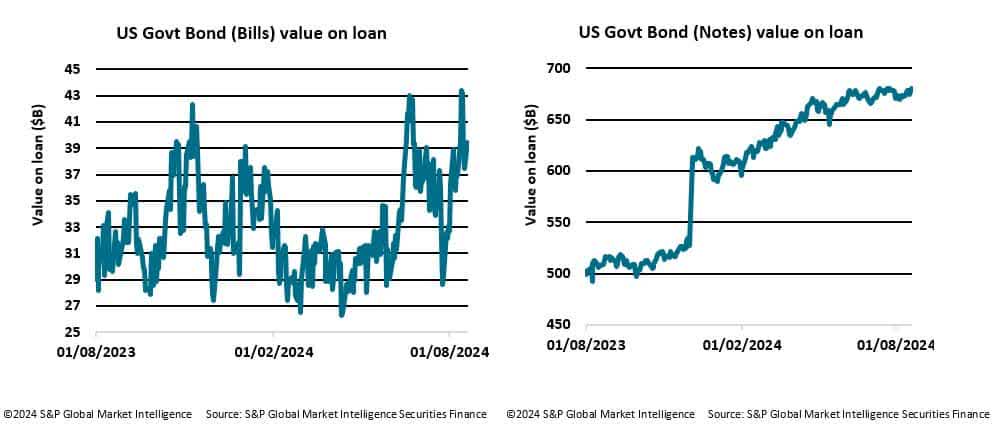

Uncertainty concerning the potential for a considerable rate of interest reduce by the Federal Reserve in September has pushed borrowing in short-dated U.S. Treasuries to current highs.

In current weeks, borrowing exercise within the price-sensitive short-term U.S. Treasury market has intensified. Regardless of combined financial knowledge, markets are at present pricing in a 100% chance of an rate of interest reduce in September. Nonetheless, the magnitude of this reduce stays unsure. Some market individuals anticipate {that a} slowing U.S. financial system will immediate a considerable 50-basis level discount, whereas others argue that current sturdy retail gross sales figures cut back the chance of an imminent recession, thereby supporting the case for a smaller 25-basis level reduce.

This uncertainty concerning the scale of the forthcoming fee reduce has led to a rise within the worth of U.S. Treasury Payments (with maturities of lower than one 12 months) and Notes (with maturities of lower than ten years) on mortgage. Fastened-income belongings with shorter maturities are notably delicate to cost fluctuations and infrequently reply extra acutely to any market mispricing. Buyers are doubtless borrowing short-dated Treasuries in anticipation of varied potential eventualities which will unfold within the coming weeks.

Anticipation of a smaller-than-expected reduce

If some traders consider that the market is overly optimistic and anticipating a big fee reduce, they may quick bonds, anticipating that the precise reduce might be smaller than anticipated. A smaller-than-expected reduce might disappoint the market, resulting in larger yields (and decrease bond costs), making a brief place worthwhile.

Market overreaction and correction

When there’s uncertainty, markets can generally overreact to the opportunity of a major reduce, pushing bond costs larger than what is likely to be justified by financial fundamentals. If traders count on the market to right after the precise fee reduce choice is introduced (particularly if the reduce is smaller or if there is not any reduce in any respect), they may quick bonds in anticipation of falling costs.

Hedging in opposition to fee hike dangers

In an setting of uncertainty, there’s all the time a threat that as an alternative of a reduce, the central financial institution would possibly select to maintain charges unchanged and even hike them if inflation or different financial knowledge surprises to the upside (any hike appears unlikely within the present scenario). Shorting bonds could be a solution to hedge in opposition to this threat, as bond costs would fall if charges weren’t reduce as anticipated or if there’s an sudden hike.

Yield curve dynamics

Uncertainty concerning the measurement of the speed reduce can result in diversified expectations concerning the yield curve’s form. If some traders consider {that a} smaller reduce or no reduce will result in a steepening yield curve (the place long-term charges rise greater than short-term charges), they may quick shorter-term authorities bonds as a part of a technique to revenue from this motion.

Contrarian play

In a extremely unsure setting, if nearly all of the market is positioning for a big fee reduce, a contrarian investor would possibly quick bonds on the expectation that the consensus view is incorrect, and that both the speed reduce might be smaller or that different components will trigger bond costs to fall regardless of the reduce.

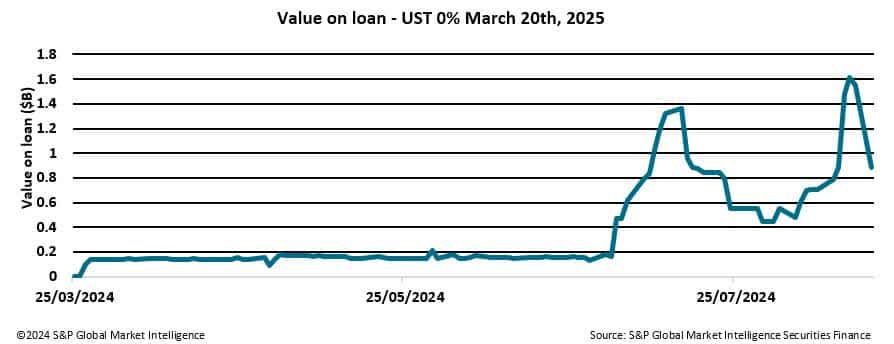

One of the vital sought-after US Treasuries within the securities lending market is the 0% 03/20/25. Worth on mortgage has been rising because the starting of July, with balances fluctuating with market exercise. S&P International Market Intelligence Repo Knowledge Analytics additionally exhibits this concern buying and selling particular within the repo market, with volumes peaking at all-time highs on August 14th at over $520B.

Whatever the final result of the September Federal Reserve assembly, prevailing market sentiment will proceed to affect exercise throughout the securities finance markets. The continued uncertainty surrounding the long run trajectory of rates of interest, together with hypothesis concerning the eventual terminal fee, is predicted to intensify volatility in mounted earnings markets within the coming weeks and months. Buyers are prone to proceed positioning themselves to handle threat and probably capitalize on market mispricing inside this unstable and unsure rate of interest setting, leveraging the liquidity offered by the securities lending market.

Authentic Submit

Editor’s Observe: The abstract bullets for this text had been chosen by Looking for Alpha editors.

[ad_2]

Source link