[ad_1]

ISerg

Buyers usually ask what’s the optimum variety of shares to carry in a single’s portfolio, and the reply is that it’s not a one measurement suits all situation. For one factor, typically it is exhausting to justify greenback value averaging into current positions when they’re buying and selling at truthful or lofty valuations.

That’s why I at all times maintain an eye fixed open for worth shares that pay excessive and well-covered dividends. Moderately than merely reinvesting dividends into the identical inventory, I discover it extra interesting and rewarding to take these dividends and make investments the place the very best alternatives are.

This brings me to the next 2 picks, which give mission-critical infrastructure that is unlikely to exit of style any time quickly. Each assist excessive yields at affordable valuations, providing doubtlessly sturdy complete returns, so let’s get began!

#1: Brookfield Renewable Companions

Brookfield Renewable Companions (BEP) points a schedule Okay-1 and is without doubt one of the largest pure-play house owners of renewable property, together with hydropower, wind, photo voltaic, and batter storage applied sciences. BEP can also be well-diversified by geography, with publicity to North and South America, Europe, and Asia.

BEP has a powerful monitor file of delivering development and worth for unitholders, with 12% FFO per share CAGR since 2016 and 6% CAGR on its distribution for over twenty years. It enjoys regular income streams from long-lived property that keep it up common 13 12 months contracts, and 70% of its revenues are listed to inflation.

BEP delivered sturdy efficiency throughout Q2 2024, with FFO per share rising by 6.3% YoY to $0.51. This development was pushed by sturdy contributions from current acquisitions, asset improvement, and favorable pricing within the clear energy market.

Notably, BEP’s core portfolio of hydroelectric property, which comprise 47% of the portfolio is seeing sturdy demand, whereas the wind and photo voltaic property had been bolstered by platform additions in key markets throughout North America, U.Okay., and India. This enabled BEP to fee 1.4 GW of recent capability in the course of the quarter, furthering its market-leading place.

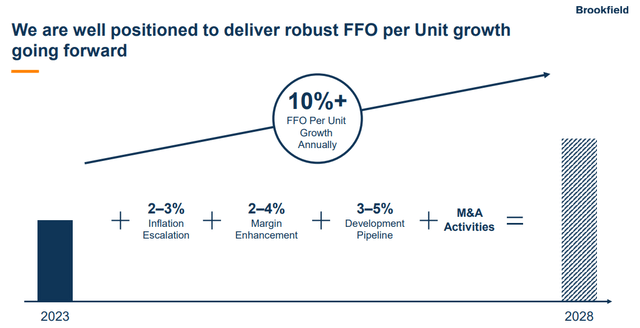

Administration is guiding for double-digit FFO per unit development this 12 months, reflecting favorable dynamics the renewable business. As proven beneath, this suits into BEP’s plan to develop FFO per unit by 10% yearly by way of 2028.

Investor Presentation

BEP’s technique is concentrated on leveraging its differentiated capabilities and entry to capital to capitalize on development alternatives in high-demand markets. This contains seemingly insatiable development within the information middle market, as highlighted beneath in the course of the current convention name:

Indicative of this, simply this previous week, PGM, a prime marketplace for information middle improvement and a market the place we’ve got important presence, had its capability public sale for 2025 and 2026 supply.

On this public sale, costs hit file highs, rising virtually 10x from the final public sale indicative of provide and demand dynamics available in the market. Information middle funding continues to speed up globally and it’s broadly estimated that information facilities might attain as much as 10% and 20% of electrical energy consumption globally and in the US, respectively, by the tip of the last decade.

In the meantime, BEP carries a BBB rated steadiness sheet with $4.4 billion in complete liquidity. It additionally expects to generate a further $1.3 billion in asset gross sales this 12 months to fund opportunistic investments. Plus, 95% of BEP’s debt is held at mounted charges, and it has an extended weighted common remaining debt time period of 12 years with no debt maturities this 12 months and simply $300M of maturities subsequent 12 months.

BEP is attractively valued at its present worth of $24.38 with a 5.8% distribution yield. The distribution can also be well-covered by a 70% FFO payout ratio. I discover the 13.3 ahead P/FFO to be affordable, contemplating administration’s steerage for 10% annual FFO/share development over the subsequent 5 years. With a near-6% yield and the aforementioned FFO per share development expectations, BEP might ship market-beating returns from right here.

#2: Plains All American

Plains All American (PAA) additionally points a Okay-1 and is an vitality midstream firm that owns a big community of pipelines, traversing throughout the Permian Basin, Canada, Rocky Mountains, Mid-Continent and South Texas/Gulf Coast.

PAA is a hidden sturdy performer with a complete return that is overwhelmed that of the S&P 500 (SPY) and friends Williams Firms (WMB), Enterprise Merchandise Companions (EPD), and Kinder Morgan (KMI) over the previous 3 years. As proven beneath, PAA’s complete return of 138% compares favorably over the others.

PAA vs Friends Whole Return (3-Yr) (In search of Alpha)

PAA is executing nicely, reaching Adjusted EBITDA development of 13% YoY to $674 million in Q2 2024, pushed by increased tariff volumes and market-based alternatives within the crude oil enterprise. Furthermore, PAA noticed favorable spreads in its NGL section and lower-than-expected working bills.

Whereas administration expects for a few of the financial savings in H1’24 to be reversed within the second half of the 12 months, they anticipate to stay value disciplined. Because of this, administration raised Adjusted EBITDA steerage for the total 12 months by $75 million to $2.75 billion on the midpoint, and reiterated money circulation steerage of $1.55 billion.

This leaves PAA with loads of money to fund each the distribution and capital tasks. It presently yields 7.1% and the distribution is very-well coated by a 190% DCF-to-Distribution protection ratio. PAA grew its annual dividend fee by $0.20 this 12 months to $1.27, and expects to boost it by $0.15 yearly till a 160% protection ratio is achieved.

This additionally leaves it with loads of retained capital to fund development tasks, together with shopping for a further 0.7% stake within the Wink to Webster pipeline for $20 million, and $150M to $200M in investments into an built-in NGL worth chain that features gathering, fractionation, storage and transportation.

This positions PAA nicely to seize development on this market, as NGL demand is predicted to develop by $19.6 billion between now and 2028 at a 6.5% CAGR. A key driver of this demand comes from the commercial section, as pure fuel liquids are a serious feedstock for petrochemical manufacturing.

Importantly, PAA carries a powerful steadiness sheet to navigate the present rate of interest setting, with BBB credit score scores from S&P and Fitch. Its web debt to EBITDA ratio of three.1x places it on par with that of huge gamers Enterprise Merchandise Companions and MPLX LP (MPLX), and it carries a large $3.2 billion in complete liquidity.

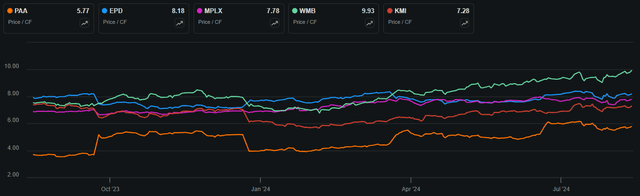

Lastly, PAA seems to be bargain-priced at $17.85 with a Worth-to-Money Stream of simply 5.8x. As proven beneath, this sits markedly decrease than that of friends EPD, MPLX, WMB, and KMI, which carry P/CF ratios within the 7.3x to 10x vary.

PAA vs Friends P/CF (In search of Alpha)

With a 7.1% distribution yield that is very well-covered by money flows, ample capital for development funding, a powerful steadiness sheet and my expectations for a baseline annual DCF per share development within the mid-single digit vary, PAA might moderately ship market beating complete returns from right here.

Investor Takeaway

Brookfield Renewable Companions and Plains All American are two shares that could be underneath the radar for a lot of traders and current engaging alternatives to place new capital to work. This is because of their excessive yields, sturdy development prospects, and stable monetary positions inside their respective infrastructure sectors.

BEP, a number one renewable vitality participant, advantages from its diversified portfolio, inflation-linked revenues, and a sturdy development pipeline within the increasing clear vitality market. PAA, an vitality midstream firm, has an in depth pipeline community, disciplined value administration, and really well-covered distribution, all supported by its sturdy steadiness sheet and strategic investments within the rising NGL sector.

Collectively, BEP and PAA present traders with mission-critical infrastructure publicity that’s positioned to ship steady earnings and market-beating complete return potential.

[ad_2]

Source link