[ad_1]

Katrina Wittkamp

I’ll hold this transient: I consider Common Mills, Inc. (GIS) is an underrated firm with robust fundamentals. The corporate constantly pays substantial, rising dividends and generates billions in free money move (FCF) every year, exhibiting a strong upward pattern. At present, GIS is buying and selling at decrease P/E and EV/EBITDA ratios in comparison with lots of its friends, and it has a enterprise mannequin constructed on recession-resistant income streams. In any case, even in robust financial occasions, meals is likely one of the final issues folks in the reduction of on—particularly in relation to merchandise as addictive as these from Common Mills. Talking as a former Fortunate Charms addict, I can attest to that! That is evidenced by resilience in GIS’s efficiency throughout robust occasions introduced by the 2008 Recession and the 2020 COVID Recession. Regardless of these strengths, GIS typically flies underneath the radar as an funding, and present analyst sentiment seems combined. Regardless of robust however comparatively lackluster outcomes throughout FY 2024, I consider the long-term prospects for this firm are very sturdy. My discounted money move (DCF) mannequin, comparable firms (comps) evaluation, and dividend low cost mannequin (DDM) all point out that GIS is considerably undervalued, even underneath probably the most pessimistic situations. Most notably, my DDM means that GIS would nonetheless be barely undervalued even when it didn’t improve its quarterly dividend for the following 5 years—a state of affairs that appears not possible on condition that it raised it in 4 of the final 5 years. Total, GIS is an underrated firm that, I consider, is a robust long-term purchase. Don’t get me fallacious, I don’t anticipate the inventory to skyrocket inside the subsequent couple of months or something like that, however I believe the inventory ought to respect by a strong quantity within the long-term, and even when it doesn’t, at the least you’re getting a pleasant dividend within the meantime.

Firm Overview & Qualitative Evaluation

Does Common Mills, Inc. (NYSE: GIS) even want an introduction? Within the international meals business, GIS is a huge holding a commanding presence with a portfolio that exceeds 100 robust underneath the corporate’s home of manufacturers—Cheerios, Häagen-Dazs, Pillsbury, Blue Buffalo. Consider your go-to snacks and, most likely, whether or not or not it’s grain and fruit snacks, ready-to-eat cereals, or ice cream, they arrive from GIS. Its 4 main working segments are North America Retail, Worldwide, Pet, and North America Foodservice.

A key energy of GIS is the excessive degree of brand name loyalty constructed through the years for its manufacturers. A lot have these manufacturers change into an element and parcel of individuals’s on a regular basis lives that it has offered a large aggressive edge to GIS over different market gamers. The corporate has been in a position to faucet into all aspects of client wants, from health-conscious buyers on the lookout for whole-grain cereals to pet homeowners wanting premium vitamin for his or her pets. This has helped them maintain floor in opposition to fixed competitors from heavyweights like Kellogg, Nestlé, Mondelez Worldwide, and PepsiCo.

Innovation has all the time been on the coronary heart of GIS’s technique. The corporate invests closely in analysis and improvement to remain forward of client tendencies, significantly in well being and wellness. For example, GIS has been proactive in providing merchandise that align with the rising demand for pure and natural meals, with the corporate claiming to be the biggest supplier of pure and natural packaged meals within the U.S. GIS can be making strides in areas like regenerative agriculture and decreasing greenhouse gasoline emissions, efforts that resonate with shoppers more and more involved about environmental points.

Nevertheless, GIS isn’t with out its challenges. One of many greatest hurdles is its heavy dependence on developed markets like North America and Europe. These markets are secure but in addition saturated, which limits progress potential. Moreover, GIS has been slower than a few of its rivals in embracing digital applied sciences, significantly in areas like e-commerce and digital advertising and marketing. Furthermore, working in a extremely regulated business implies that GIS should navigate stringent meals security requirements and labeling necessities, each at dwelling and overseas, including complexity and value to its operations. GIS’s comparatively restricted presence in rising markets presents each a problem and a chance. Whereas the corporate has a stronghold in developed areas, increasing its footprint in high-growth areas like Asia, Africa, and Latin America might open new avenues for progress.

Financials

GIS has constantly demonstrated robust monetary efficiency, exhibiting resilience and progress even in difficult financial environments. Between 2017 and 2024, the corporate’s revenues have elevated nearly yearly, rising from round $15.62B in 2017 to roughly $19.86B in 2024. Whereas it is true that income barely dipped from $20.09B in 2023 to $19.86B in 2024, marking the primary decline since 2017, this can be a minor setback within the broader context of steady progress. Web revenue has additionally adopted a typically constructive pattern. In 2019, GIS reported a internet revenue of about $1.75B, which grew to $2.18B in 2020 after which to $2.34B in 2021. By 2022, internet revenue had elevated to $2.71B, although it barely decreased to $2.59B in 2023 and $2.50B in 2024. EBITDA has been on a basic upward pattern as properly. From $3.14B in 2019, EBITDA elevated to $3.55B in 2020, $3.75B in 2021, $4.05B in 2022, barely leveling off at round $3.98B in each 2023 and 2024. It’s vital to notice that for the sake of brevity, I’ve solely been itemizing the latest 5 years, however in case you take a better take a look at GIS’s financials over an extended interval, you’ll see that this upward pattern has been ongoing for dozens of years. Whereas internet revenue, income, and EBITDA did expertise slight declines in 2024, which probably contributed to the drop in inventory worth from $68 to $63 following the June 2024 earnings report (although it has since recovered to over $70), these dips are minor when you think about the larger image. Related modest declines in different particular person years have occurred however have in the end been inconsequential when seen inside the context of GIS’s general long-term monetary trajectory. GIS has additionally constantly outperformed expectations, particularly relating to EPS. In response to Looking for Alpha, GIS has overwhelmed EPS expectations in 18 of the final 20 quarters and exceeded income expectations in 13 of these quarters. That stated, there are a few areas that warrant consideration. Over the previous few years, the corporate’s complete debt has just about stagnated round $12B-$13B. However money available has decreased from $1.68B in 2020 to $418M in 2024. Capital expenditures (capex) have elevated from $530.8M in 2020 to $774.1M in 2024. Nevertheless, I consider these points are comparatively minor when seen within the context of GIS’s general monetary well being, particularly because the firm’s free money move (FCF) stays robust and has been on a basic upward pattern. GIS generated roughly $2.66B in FCF in 2024, $2.87B in 2023, $2.71B in 2022, $2.34B in 2021, and $3.56B in 2020. As my discounted money move (DCF) mannequin in a while on this article will display, an organization constantly producing FCFs at this degree needs to be buying and selling at a far larger worth than GIS’s present market worth of $70.38.

Considered one of GIS’s most underrated strengths is its resilience throughout financial downturns. As I discussed earlier, even in robust occasions, meals is maybe the very last thing folks in the reduction of on—particularly in relation to merchandise as in style and addictive as these from Common Mills. This resilience is clearly mirrored in its financials throughout the 2008 Recession. From 2006 to 2009, GIS’s internet gross sales constantly grew from roughly $11.71B to $12.44B, $13.65B, and in the end $14.69B. Equally, internet earnings elevated steadily from about $1.09B to $1.14B, $1.29B, and at last $1.30B over the identical interval. Much more spectacular is how the corporate’s inventory worth remained comparatively secure throughout the 2007-2009 interval, staying within the mid-20s to low 30s—a outstanding feat in comparison with the broader market’s efficiency. Equally, throughout the early phases of the COVID-19 disaster, GIS’s inventory worth jumped from the low 50s to the low 60s. GIS noticed important will increase in each income and internet revenue from 2019 to 2020. After all, it’s no shock that GIS can be one of many few firms to profit throughout such an occasion.

Total, GIS is likely one of the uncommon firms that not solely withstands however typically thrives throughout financial downturns and crises, making it a robust contender for long-term funding.

Valuation

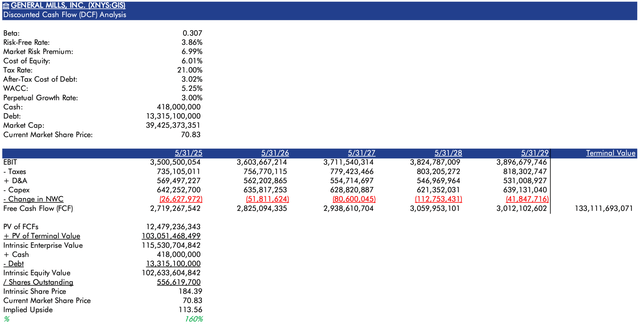

Let’s begin with my discounted money move (DCF) mannequin. In developing this mannequin, I attempted being unusually pessimistic. I calculated GIS’s beta at roughly 0.307 (5-year every day). To additional mood the outcomes, I assumed a market threat premium (MRP) of 6.99%, which is larger than the typical MRP of 5.5% as of 2024 (in line with Statista). For the risk-free charge, I used the US 10-12 months Treasury Charge on 8/22/2024 of three.86%, leading to a price of fairness of 6.01%. For GIS’s price of debt, I derived it by dividing their FY 2024 curiosity expense by their FY 2024 complete debt and adjusting for a tax charge of 21%, which gave me a price of debt of three.02%. By weighting the price of debt and fairness appropriately, I arrived at a WACC of 5.25%, which is in keeping with varied estimates out there on-line. For context, GuruFocus estimates GIS’s WACC at 3.27%, ValueInvesting.io supplies a variety of 5.2% to 7.6% (with a mean of 6.4%), FMP at 4.21%, and Alpha Unfold at 6.42%. To challenge EBIT, D&A, Capex, and adjustments in NWC, I utilized historic knowledge from 2010 onward and employed Prophet, a forecasting device developed by Fb’s knowledge scientists. For taxes, I assumed an annual tax expense of 21% of EBIT, which is larger than what they’ve really paid (for instance, their revenue tax expense was ~17.3% of their EBIT in FY 2024), in step with my effort to be extra cautious in my assumptions. These projections yielded estimated FCFs of roughly $2.7B, $2.8B, $2.9B, $3.1B, and $3.0B for 2025 by means of 2029, which align intently with GIS’s present FCF trajectory. My mannequin assumes a perpetual progress charge of three%, the everyday determine utilized in DCF mannequin. Usually, DCF fashions calculate the terminal worth by taking the ultimate yr’s forecast, rising it by the perpetual progress charge, and dividing this by the distinction between the WACC and the perpetual progress charge. However as a substitute of utilizing the final yr’s forecast (~$3.0B), I used the typical of the 5 FCF forecasts (~$2.9B), additional skewing the outcomes in opposition to GIS. Regardless of all these pessimistic assumptions, my mannequin nonetheless signifies that GIS is considerably undervalued, with an intrinsic share worth of $184.39—implying a considerable +160% upside in comparison with the present market worth of $70.83.

Writer’s Calculations

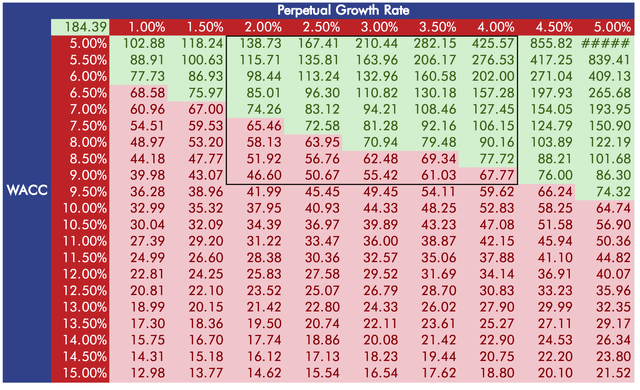

If you happen to’re involved in regards to the outcomes being skewed by seemingly arbitrary assumptions like WACC and perpetual progress charge, my sensitivity evaluation under demonstrates that GIS would stay undervalued throughout most WACC-perpetual progress charge mixtures inside the realm of chance. Though I examined WACCs from 5% to fifteen% in 0.5% increments, I consider any WACC above 9.0% might be disregarded. Absolutely the highest WACC estimate I might discover on-line for GIS is 7.6% (the high-end of ValueInvesting.io’s WACC vary for GIS). And even the very best price of fairness estimate I discovered on-line was simply 8.8% (the high-end of ValueInvesting.io’s price of fairness vary for GIS).

And remember the fact that many sources estimate GIS’s WACC to be underneath 5%. Moreover, perpetual progress charges usually vary between 2% and 4%, and something outdoors this vary is probably going irrelevant. Within the desk under, I positioned a field round values for WACCs between 5% and 9% and perpetual progress charges of two% to 4% because the “realm of chance.” This vary clearly exhibits GIS can be undervalued in most situations. Provided that absolutely the highest WACC estimate I discovered was 7.6%, not 9%, it will even be cheap to disregard WACCs above 7.5%. GIS stays undervalued in nearly each WACC-perpetual progress charge mixture inside the 5% to 7.5% and a couple of% to 4% ranges (apart from a 7.5% WACC paired with a 2% perpetual progress charge).

Writer’s Calculations

Please word that values under GIS’s present market worth on the time of writing of $70.83 are highlighted in pink, whereas these above this determine are highlighted in inexperienced.

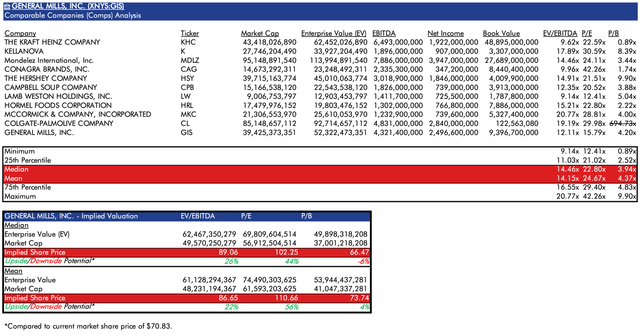

Subsequent, let’s dive into my comparable firms (“comps”) evaluation. For this mannequin, I used the businesses listed as GIS’s friends in line with Capital IQ: KGC, Ok, MDLZ, CAG, HSY, CPB, LW, HRL, MKC, and CL. Based mostly on the median and imply EV/EBITDA ratios of GIS and its friends, GIS’s implied share worth can be $89.06 and $86.65, respectively—each considerably larger than the present market worth of $70.83 on the time of writing. Equally, utilizing the median and imply P/E ratios of GIS and its friends, the implied share worth can be $102.25 and $110.66, respectively, additional indicating substantial upside.

For the price-to-book (P/B) ratios, I selected to exclude CL’s outlier P/B ratio of 694.73x. With out CL, the median and imply P/B ratios recommend GIS’s implied share worth can be $66.47 and $73.74, respectively, with the previous indicating a slight draw back and the latter exhibiting a modest upside. For these curious, together with CL would lead to an implied share worth of $67.52 utilizing the median P/B ratio and a wildly exaggerated $1,133.25 utilizing the imply P/B ratio. Total, my comps evaluation means that GIS is considerably undervalued when contemplating EV/EBITDA and P/E, whereas showing roughly pretty valued when utilizing P/B.

Writer’s Calculations

Sources: Market cap values have been obtained from Refinitiv, whereas Capital IQ offered the money and complete debt figures used to calculate every enterprise worth, in addition to the entire EBITDA, internet revenue, and ebook worth figures. Please word that the EBITDA and internet revenue values are for the trailing twelve months (TTM), whereas the ebook worth figures are from the latest quarter (MRQ).

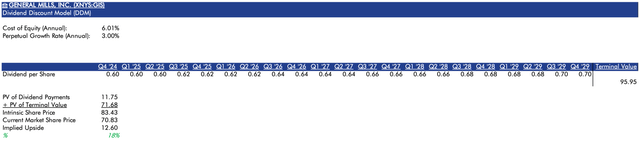

Subsequent, let’s check out my dividend low cost mannequin (DDM). I consider that GIS’s robust and steadily rising dividend yield is one in every of its most compelling options. In DDM fashions, the price of fairness is used because the low cost charge somewhat than the WACC. Over the previous few years, GIS has constantly elevated its dividend funds. For example, in Q3 2024, they raised their quarterly dividend from $0.59 to $0.60 (+$0.01); in Q3 2023, from $0.54 to $0.59 (+$0.05); in Q3 2022, from $0.51 to $0.54 (+$0.03); and though the dividend held regular at $0.51 all through 2021, it was elevated from $0.49 to $0.51 (+$0.02) in This fall 2020.

In my first DDM mannequin under, I’ve assumed that GIS will proceed this pattern by rising its quarterly dividend by $0.02 in Q3 of every of the following 5 years, which appears cheap given their historical past. For the terminal worth, I used a perpetual annual progress charge of three%, a typical assumption in DDM and DCF fashions. With these inputs, my mannequin suggests an intrinsic share worth of $83.43, implying a strong $12.60 (+18%) upside from the present worth of $70.83.

Writer’s Calculations

Please word that the PV of the dividend funds was calculated utilizing Excel’s XNPV operate to precisely account for the timing of quarterly dividend funds with an annual low cost charge. Equally, the terminal worth was calculated primarily based on the annual dividend for the ultimate forecasted yr ($2.80), not the quarterly dividend ($0.70).

What’s much more noteworthy is how the DDM mannequin performs in a worst-case state of affairs. Contemplating GIS has raised its dividend in 4 of the final 5 years, it’s extremely unlikely they wouldn’t accomplish that at the least as soon as over the following 5 years. Nevertheless, in my extra pessimistic mannequin under, I’ve assumed that the quarterly dividend stays flat at $0.60 for your complete interval. The terminal worth remains to be calculated with a 3% perpetual progress charge. Below these assumptions, the mannequin signifies an intrinsic share worth of $72.37. Even on this absolute worst-case state of affairs, GIS nonetheless seems barely undervalued in comparison with its present worth.

Writer’s Calculations

Total, even underneath probably the most pessimistic assumptions, GIS seems undervalued in line with quite a lot of totally different valuation strategies.

The Foremost Draw back

Regardless of all of the positives I’ve highlighted, there’s one main draw back: the present inventory worth of GIS is certainly not a cut price when seen within the context of its general buying and selling historical past. At $70.83, the share worth is hovering near its 52-week excessive of $74.45. The inventory reached an all-time excessive of $90.89 on Might 15, 2023. Whereas I really feel that the intrinsic worth of GIS is approach larger than the present worth, I extremely doubt the inventory will rise past $90 within the close to future. The short-term view from analysts can be extra cautious. The typical short-term worth goal from the most recent 18 analysts, in line with Zacks, is $68.18, with targets ranging between $62 on the low finish and $76 on the excessive finish.

My perspective could also be comparatively extra optimistic in relation to the overwhelming majority of others, and the consensus among the many analysts appears combined. Whereas the latest 2 analyst rankings are Robust Buys, of the 19 complete analysts, solely 4 charge it as a Robust Purchase, whereas the opposite 15 charge it as a Maintain. However remember the fact that this combined sentiment displays the inventory’s short-term potential. Like I’ve talked about earlier than, I’m not anticipating GIS to surge within the brief time period. However I do consider that the inventory is basically undervalued. Whereas it’d take time for the market to understand this, I anticipate that GIS’s worth will respect considerably in the long run. It will not be the strongest short-term purchase, however for traders with a long-term perspective, I consider that GIS stands out as probably the greatest alternatives out there.

Conclusion

To sum all of it up, I actually do consider that GIS is an underrated gem for long-term traders. Sure, the inventory’s present worth isn’t a cut price, hovering close to its 52-week excessive and never removed from its all-time peak. Nevertheless, I see this as a minor subject within the grand scheme of issues. The corporate’s robust fundamentals, constant dividend progress, and strong FCF era make it very interesting. Although the inventory won’t soar within the brief time period—one thing that’s mirrored within the combined analyst sentiment—I’m assured that GIS is basically undervalued. My fashions, whether or not DCF, comps, or DDM, all level to the identical conclusion: GIS is undervalued and there’s important upside. Though it could take time for the market to understand this, I consider affected person traders can be rewarded. And even when the inventory would not rocket larger within the close to future, at the least you are still getting a fairly good and dependable dividend.

[ad_2]

Source link