[ad_1]

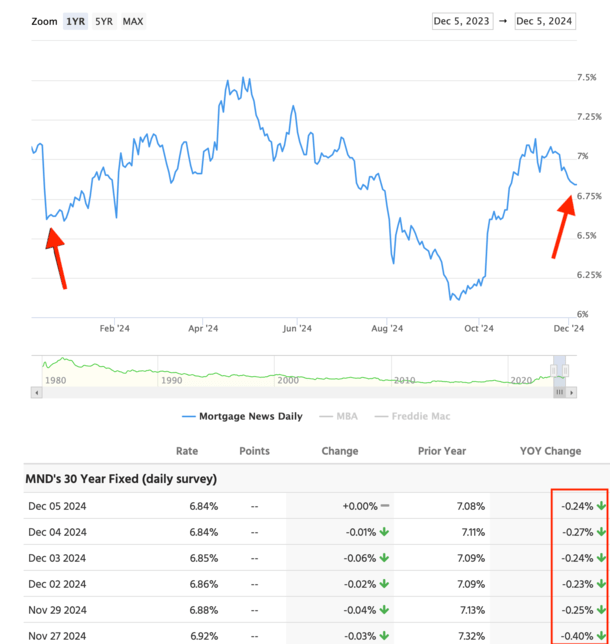

It’s been a wild experience for mortgage charges this 12 months. The 30-year mounted started 2024 at round 6.625% and is at present not removed from these ranges.

Regardless of that, charges have been as little as 6% and as excessive as 7.50%. So there was fairly a spread over the previous 50 weeks or so.

Charges rallied final December after the Fed revealed it was able to pivot and start loosening financial coverage.

However as at all times, they ebbed and flowed alongside the way in which, as an alternative of merely falling decrease and decrease, with the previous couple months fairly the rollercoaster increased.

Nevertheless, we stay in a falling charge surroundings, even when charges aren’t at present at their 2024 lows. Permit me to clarify.

Mortgage Charges Are Higher Than Their Yr-In the past Ranges

Many issues, together with residence costs and mortgage charges, are measured each month-to-month and year-over-year.

The latter can provide you an even bigger image of the place one thing is trending, whether or not it’s residence costs or mortgage charges.

For instance, residence costs may fall month-to-month, however nonetheless register year-over-year beneficial properties because of stronger months alongside the way in which.

With regards to mortgage charges, I’ve argued since mid-September that we remained in a falling charge surroundings.

Why did I’ve to? As a result of charges on the 30-year mounted climbed from about 6% to 7% within the span of lower than two months.

This had many fearing for the worst. That the current enchancment in charges was one other head pretend. And a return to eight% or increased was imminent.

In spite of everything, we’d seen this film earlier than, as just lately as spring of this 12 months, when the 30-year mounted climbed from 6.5% to 7.5%.

However my argument has at all times been that we’ve seen decrease highs. So first it was 8%, then 7.5%, and most just lately 7%.

As well as, mortgage charges have been besting their year-ago ranges, exhibiting a longer-term development versus some short-lived noise.

However They’ll Must Preserve Dropping Because of a Current Uptick

Simply to summarize the previous couple months, the Fed reduce charges in mid-September, which led to just a little promote the information bounce in charges.

Merely put, the reduce was baked in as evidenced by charges falling practically two share factors from October 2023.

Then we received a one-off scorching jobs report that additional propelled mortgage charges increased, adopted by a presidential election.

As soon as it turned clear that Trump was the frontrunner to win, charges moved even increased nonetheless, as his insurance policies like tariffs are anticipated to be inflationary.

However finally that large run up in charges ran out of steam and so they appeared to get again on their downward monitor.

In the end, the financial knowledge is what issues and it continues to point out cooling inflation and a few concern about rising unemployment.

That has pushed mortgage charges again from 7.125% to round 6.75% once more. The massive query now’s if they’ll maintain going decrease.

As proven within the chart above from MND, the 30-year mounted plummeted in early December 2023 when the Fed implied it was finished mountaineering and able to reduce charges in 2024.

That required the 30-year mounted to be sub-6.82% to beat its year-ago ranges, which it barely achieved thanks to a different smooth labor report this previous Friday.

It now faces a fair greater take a look at because the 30-year mounted was 6.65% in mid-December 2023, that means we’ll have to see charges enhance additional over the subsequent week to match/beat these ranges.

In fact, it doesn’t must be good.

Can Mortgage Charges Get Again to Sub-6% By February?

Whereas charges definitely appear to be trending in the proper route after the mud settled from the election, they’ve nonetheless started working to do.

To be able to proceed to stay beneath year-ago ranges, they’ll have to fall one other 10 foundation factors over the subsequent week, which appears cheap.

However to achieve decrease highs in 2025, they’ll have to maintain exhibiting enchancment and get into the 5s, contemplating we noticed a charge of 6.125% earlier this 12 months.

They’ve time to do this, however mortgage charges are usually lowest in winter, so maybe it’ll occur sooner slightly than later.

The final time the 30-year mounted was sub-6% was truly on February 2nd, 2023, when it hit 5.99%, per MND. It was very short-lived, and charges jumped to 7% that very same March.

Nevertheless, it’s doable charges might proceed to float that manner into 2025, divvied up between some enhancements this month and in January.

And it’s not likely an enormous ask when you think about that the 30-year mounted was 6.125% in mid-September. Additionally notice that charges are likely to fall for a number of years after a Fed pivot.

Conversely, the most important danger to mortgage charges climbing within the short-term, aside from any sturdy financial knowledge equivalent to increased inflation or decrease unemployment, can be inauguration-related noise.

There’s been a relative calm of late, however with that date steadily approaching, the federal government spending and inflation rhetoric might ratchet up once more in early 2025.

Nonetheless, it wouldn’t shock me to see mortgage charges proceed to development decrease in 2025 and stay in a falling charge surroundings.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Comply with me on Twitter for warm takes.

[ad_2]

Source link

{kind=link}