[ad_1]

da-kuk/E+ through Getty Pictures

Costly inventory retains rising

Arm Holdings (NASDAQ:ARM) had an important This autumn quarter and monetary 2024. The corporate’s income reached $928 million, a 47% YoY improve, pushed by sturdy v9 chip adoption and semiconductor restoration. Gross margin for the quarter was 97% and non-GAAP working margin stood at 42%, according to firm steerage and market expectations.

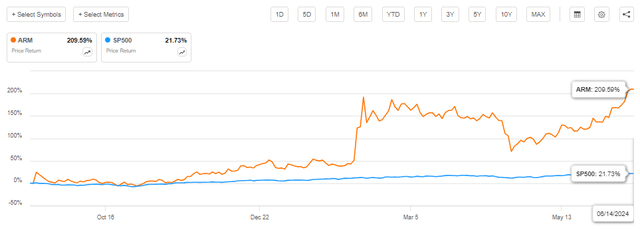

The inventory was already up 100% from its IPO worth earlier than earnings. After the earnings, the inventory continued to rise, and appreciated one other 50%. It has now returned 200% since its IPO, making it top-of-the-line performing shares available in the market (see beneath).

ARM worth efficiency (Searching for Alpha)

Because the inventory continues to rise, many SA analysts have turned bearish, ranking it a ‘Promote’ resulting from overvaluation considerations. Nonetheless, the market stays bullish, driving the inventory worth even larger.

This example has caught our consideration, so we determined to take a better look. We wished to see what the market was pricing in and verify if expectations had been aligned with actuality or not. We examined ARM’s long-term progress prospects to know if its excessive valuation might be justified.

The results of our evaluation is that Arm’s progress drivers and market place are among the many strongest within the trade. The corporate dominates the cell and IoT markets and is quickly gaining market share in datacenters, PCs, and automotive sectors. With restricted competitors on the horizon, we expect that ARM is positioned to change into the dominant international computing platform in a couple of years. The corporate is on an accelerated progress path, and that is doubtless what the market is pricing in right this moment.

The Semi Market Restoration Will Gas Royalty Charges

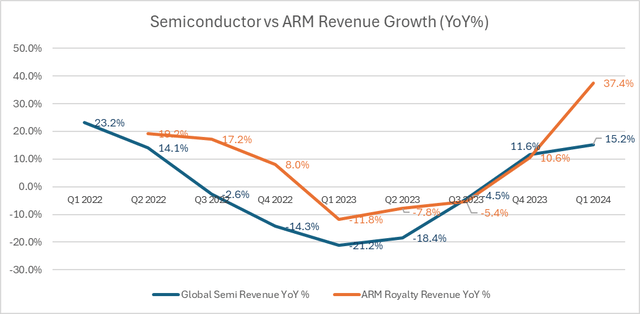

The explanation we need to take a look at the semi market is that ARM has greater than 50% share of the worldwide chip market. The semi gross sales developments give us indication of ARM’s royalty income. After an 8% decline in 2023, the worldwide semiconductor trade has began to recuperate. Based on the SIA, in This autumn 2023, semi gross sales turned optimistic with 12% YoY progress, and achieved 15% YoY progress in Q1 2024 (see beneath chart). ARM’s royalty income has carefully tracked international semi gross sales, with each declining in FY23 and recovering within the final quarter of 2023. In Q1, semi progress was 15%, whereas ARM income elevated 37%. As a consequence of its multiplier impact (extra CPUs per chip and better v9 royalty charges), the corporate is ready to develop a lot sooner than the semi trade.

Semi income YoY% vs ARM Royalty income (Creator)

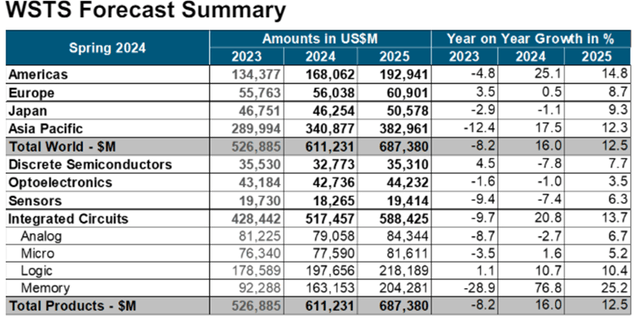

SIA expects the sturdy development to proceed all through 2024 and 2025. It’s sizing the market at $611 billion and projecting 16% progress in 2024 and 12.5% in 2025 (see beneath).

International semiconductor forecast (SIA)

Because of the favorable semi market circumstances, the corporate anticipates royalty income to develop by roughly 20% this 12 months. Nonetheless, we see important upside potential for royalty income resulting from its compounding impact.

ARM Taking Over The Cloud Datacenter

ARM’s CPUs are quickly gaining traction within the datacenter phase. Decrease energy consumption and high-core density options of Arm CPUs are interesting to cloud service suppliers. As of 2022, the corporate had a ten% share of the cloud computing market, and it’s anticipated to develop its share to 22% in 2025.

The principle driver for this progress is the demand for customized silicon. ARM has a particular customized silicon program which is known as Compute Subsystem (CSS) and permits corporations like Microsoft, Amazon and Google to design and manufacture customized Arm-based chips. This program permits the corporate to seize extra of the worth chain and will increase its income per unit (bypassing chip producers as properly)

By way of CSS program progress, Amazon’s Graviton 4 Arm chip was introduced final 12 months and Nvidia introduced that its Arm-based CPU Grace can be a part of the Blackwell superchip. Google introduced Axion, their first Arm-based chips for GCP workloads and Microsoft has just lately introduced its Azure VM collection operating by itself Cobalt 100 Arm-based processor. This practice silicon development is anticipated to proceed, as the corporate will increase its market share within the datacenter. From the This autumn earnings name:

Rene Haas (CEO):

I believe now with NVIDIA’s most up-to-date announcement, Grace Blackwell, you’re going to see an acceleration of ARM of the info heart in these AI functions. One of many advantages that you simply get by way of designing a chip resembling Grace Blackwell is by integrating the ARM CPU with the NVIDIA GPU, you are capable of get an interconnect between the CPU and the GPU that enables for a a lot larger entry to reminiscence, which is among the limiting components is for coaching and inference functions. In a traditional system the place you would possibly connect with an X86 externally, you need to do this over a PCI bus, which is way slower. So by utilizing a customized bus within the NVIDIA instance like NVLink, you get a lot larger reminiscence bandwidth.

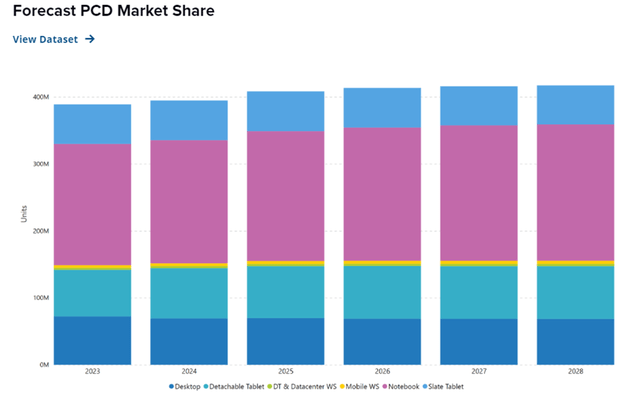

The Home windows On ARM Alternative

The AI PC goes to revolutionize the PC market, and Arm appears to be the best platform for it. The corporate has key benefits resulting from its low-power utilization, light-weight design and pace. The corporate already powers all Mac PCs, which has 15% PC market share. Arm is now pushing for Home windows on Arm along with Microsoft and a number of other OEMs. Microsoft just lately launched its Arm-based Copilot PCs in partnership with Acer, ASUS, Dell, HP, Lenovo and Samsung (all powered by Qualcomm’s Snapdragon X processor). Arm CEO Rene Haas is predicting that the corporate can seize over 50% of the Home windows PC market inside 5 years.

Based on IDC, PC shipments are projected to achieve 420 million items by 2028, with Home windows holding a 74% market share. This presents a major TAM alternative for ARM, equal to roughly 310 million units (see beneath).

IDC PC market progress (IDC)

Traditionally, ARM obtained comparatively low royalty charges for its Armv8 and older chips on Mac units. Nonetheless, with the introduction of Armv9, it’s now charging larger royalty charges. As Home windows Copilot PCs can be based mostly on Arm v9, we anticipate Home windows on ARM to change into a major progress driver for the corporate within the coming years.

Observe: There’s at present a lawsuit between ARM and Qualcomm (QCOM), the place ARM is suing Qualcomm for breach of licensing settlement associated to Qualcomm’s acquisition of chip design firm Nuvia. This ongoing authorized concern has led Arm to request all of the Snapdragon-based Home windows PC shipments to be halted. Presently, Qualcomm is the unique supplier of Arm CPU’s for Home windows PCs, however this exclusivity will expire in 2025. At that time, different chip corporations will be capable to manufacture Arm chips for Home windows PCs.

The Automotive Alternative

ARM has a various progress technique. The corporate shouldn’t be solely increasing its choices with higher-value providers resembling ATA (Arm Whole Entry) and CSS applications (compute sub system), but in addition broadening its portfolio with verticalized choices with a purpose to goal high-growth markets like automotive and industrial IoT.

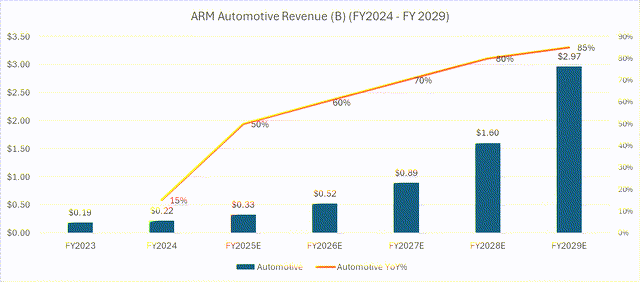

The Automotive phase is one in every of ARM’s fastest-growing areas, pushed by the rising demand for autonomous and related automobiles. The corporate has launched many new merchandise, which can drive accelerated demand within the subsequent a number of years. The automotive phase additionally has larger royalty charges in comparison with smartphones and IoT units, leading to the next progress multiplier for the corporate. In FY 2023, income from the automotive phase was roughly $200 million, and we anticipate this determine to develop considerably because the autonomous automobile trade accelerates. By FY 2029, we anticipate auto income to achieve $3 billion (see beneath).

Automotive income mode (Creator)

Valuation

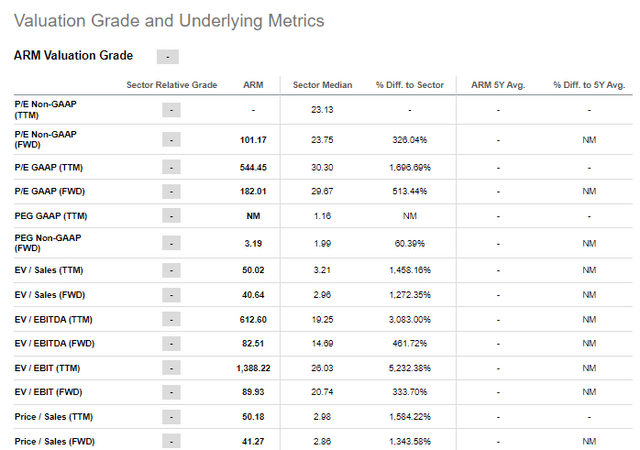

ARM is among the costliest shares available in the market, buying and selling at very excessive valuations, with a gross sales a number of of 41 and an earnings a number of of 101. Administration is guiding for 17% – 27% progress in FY2025, and 20%+ progress in the long term, which nonetheless would not justify the excessive multiples (see beneath).

ARM Valuation metrics (Creator)

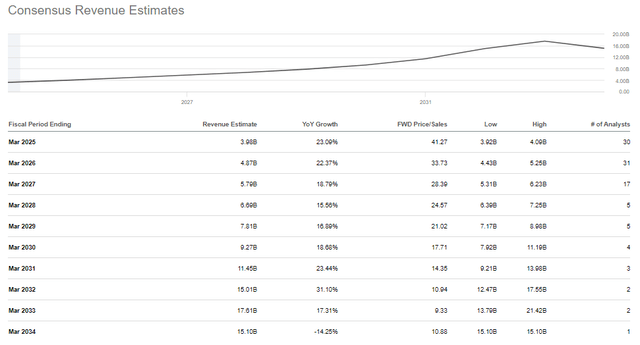

Curiously, the market can be ignoring analysts’ forecasts, that are fairly modest, as proven beneath.

ARM analysts’ consensus (Searching for Alpha)

We expect that the market is pricing ARM at such a excessive premium resulting from its distinctive and dominant place. With restricted competitors and a number of progress levers, it has a really important upside potential, which the market is already factoring.

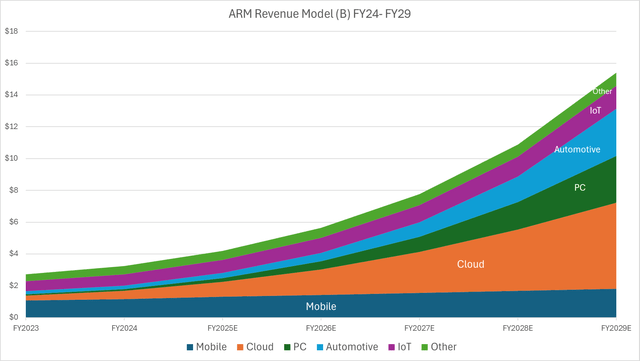

To grasp the upside potential, we’ve got modeled Arm’s potential income for the following 5 years. Our mannequin initiatives a 37% CAGR till FY2029. We venture 30% progress in FY2025 as a result of semi restoration and accelerated Armv9 transition. Past FY2026, we anticipate a number of progress levers to kick in, together with Home windows on Arm, cloud, AI and automotive, creating an accelerated progress path for the corporate (see beneath).

ARM Income mannequin FY 2029 (Creator)

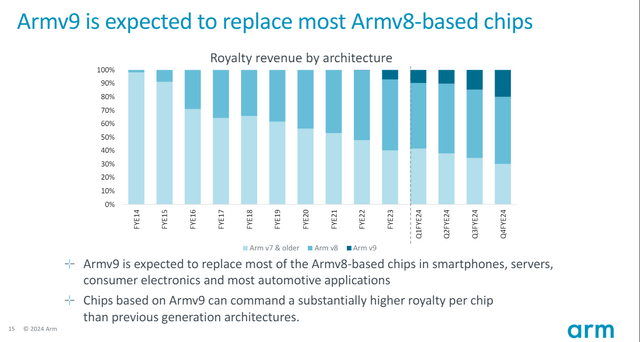

Our mannequin initiatives Arm’s cell phase to develop at 9% CAGR over the following 5 years, outpacing the two.4% CAGR forecasted by IDC for the cell market. The first driver of this progress is the continuing ARMv9 transition, which has double the royalty charges of v8 and nonetheless has roughly 50% adoption to go (see beneath). Moreover, the Apple telephone refresh cycle is anticipated to speed up, pushed by the Apple’s AI bulletins at WDC final week. Some analysts anticipate a ten% improve in iPhone gross sales in 2025, which might additionally increase the corporate’s royalty charges.

Arm v9 transition (ARM)

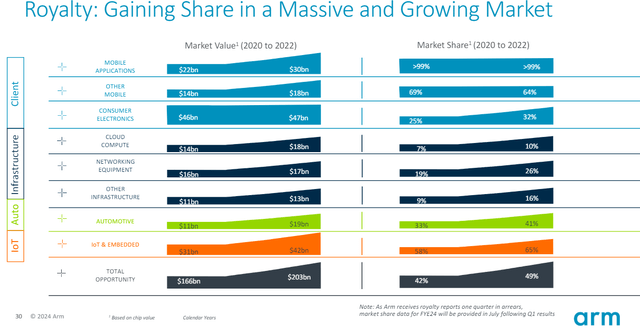

ARM’s cloud phase is its fastest-growing, pushed by sturdy demand from hyperscalers and chipmakers. The hyper-scaler compute market is rising at 23% CAGR, and the corporate is successful share on this quickly rising market. In FY 2023, ARM’s cloud income was roughly $300 million, equal to 10% market share (see beneath). Analysts predict that ARM’s market share will attain 22% by 2025. Our estimation is that ARM will obtain 30% cloud market share by FY 2029, producing $5.4 billion income.

ARM Market share (ARM)

Pushed by the Home windows on ARM push, we anticipate Arm’s PC market share to achieve 60%, with Home windows accounting for 45% and macOS 15%, respectively. We venture a 75% CAGR over the following 5 years, leading to $3 billion PC Arm income by FY 2029. Within the automotive sector, we estimate ARM’s market share will improve from 42% in FY 2023 to no less than 60% by FY 2029, equal to $3 billion income. For IoT we estimate a 15% CAGR, aligned with the worldwide IoT market progress. In conclusion, we imagine the corporate has the potential to achieve $15 billion income by FY 2029.

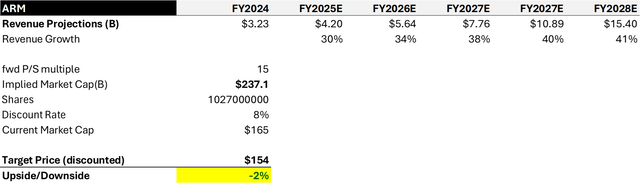

We need to do a ahead gross sales a number of valuation based mostly on the $15 billion projected income for FY 2029. We’re assuming a 37% CAGR and assigning a ahead gross sales a number of of 15 resulting from excessive progress. Based mostly on a reduction price of 8%, our worth goal is $154, which means that the inventory is at present pretty valued contemplating its excessive progress potential.

ARM Valuation mannequin (Creator)

Dangers

The principle threat for ARM is the RISC-V platform. RISC-V is an open-source competitor to Arm and is supported by main expertise corporations like Google, Nvidia, and Qualcomm. RISC-V is gaining recognition within the trade, however we do not assume it may be a major risk to Arm. Arm has an awesome dominance available in the market resulting from its diversified portfolio, its broad ecosystem and superior R&D capabilities. For greater than 30 years, the corporate has constructed an unlimited ecosystem of companions and prospects. This ecosystem is crucial to Arm’s success, and it could be very troublesome for RISC-V to duplicate it.

Conclusion

We imagine that Arm is a particular firm and has key attributes that no different firm has. The corporate brings innovation to the trade, is benefiting from all the most important secular developments, has a number of progress levers and is gaining fast market share throughout main end-markets. As a consequence of its distinctive market place, the corporate is able to capitalize on giant AI alternatives.

Our evaluation exhibits that ARM has the potential to achieve $15 billion income by FY 2029, which is twice the present consensus. Nonetheless, our valuation mannequin suggests the market has already priced on this progress potential, because the inventory is at present buying and selling near our goal worth. However we additionally acknowledge that corporations like ARM will not be simple to valuate, as they’ve a number of secular progress drivers and are on the heart of an ongoing AI-driven paradigm shift. This complexity makes it troublesome to precisely assess the corporate’s future efficiency. Subsequently, we advocate profiting from any worth weak spot or market correction to put money into the inventory, as its potential upside outweighs the valuation uncertainty.

[ad_2]

Source link