[ad_1]

AaronAmat

Funding Thesis

BlackBerry’s (NYSE:BB) inventory jumps 8% premarket on the again of its fiscal Q1 2024 report.

And but, I stay bearish on this inventory. I contend that this cheer from buyers is little greater than a aid rally that its earnings outcomes weren’t worse.

Basically, I argue that this enterprise has too little in the best way of prospects. After which, to compound issues, the inventory is already priced at 87x this yr’s EBITDA.

For bullish buyers, their argument is that the inventory was as soon as larger and subsequently, that I am too bearish, as this inventory is primed to revert larger.

All in all, this quote from Warren Buffett neatly summarizes my opinion:

Ought to you end up in a chronically leaking boat, power dedicated to altering vessels is prone to be extra productive than power dedicated to patching leaks.

Fast Recap

Again in April, I mentioned,

[…] whereas BlackBerry’s fiscal This autumn 2024 outcomes current a combined image, with steering indicating higher prospects than initially perceived, I keep my bearish stance on the inventory.

Creator’s work on BB

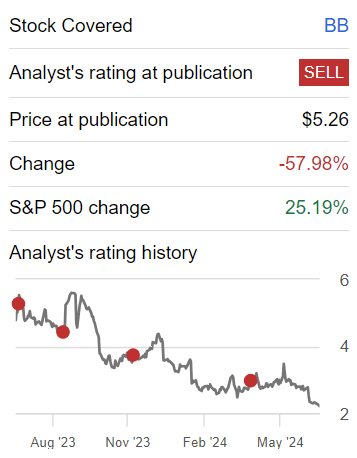

BlackBerry is a inventory that I have been bearish on for some time. And for its half, the inventory continues to slip, and is down about 50% (together with the premarket leap), whereas the S&P 500 is up roughly 25% in the identical time-frame.

Now, as we glance forward, I reiterate my stance.

BlackBerry’s Close to-Time period Prospects

BlackBerry at this time focuses on two important areas: Web of Issues (“IoT”) and cybersecurity.

Within the IoT division, BlackBerry’s QNX software program is utilized in automotive and varied embedded programs, offering essential functionalities like digital cockpits and superior driver help programs (“ADAS”).

The cybersecurity division focuses on securing communications and defending knowledge by way of options like Cylance, which leverages AI to defend in opposition to cyber threats, and SecuSmart, which provides encrypted communication options for high-security environments.

Within the close to time period, BlackBerry’s prospects are honest. The IoT division is performing satisfactorily, with wholesome income progress from automotive software program options and new design wins with main international automakers.

Moreover, the cybersecurity division is gaining traction, significantly within the small and medium-sized enterprise market, by way of its managed detection and response providers.

Nevertheless, BlackBerry faces challenges too. Within the IoT sector, the delay in automotive software program improvement applications as a result of trade’s transition to extra software-defined automobiles is a major headwind. The fluctuating demand for electrical automobiles and the complexities of integrating new applied sciences into conventional automaker operations add to those challenges.

In BlackBerry’s cybersecurity division, as has been a pervasive subject all through 2024 with commentary from CrowdStrike (CRWD), Palo Alto Networks (PANW), and different cyber gamers too, elongated gross sales cycles proceed to hamper progress on this sector.

Given this balanced background, let’s now talk about its fundamentals.

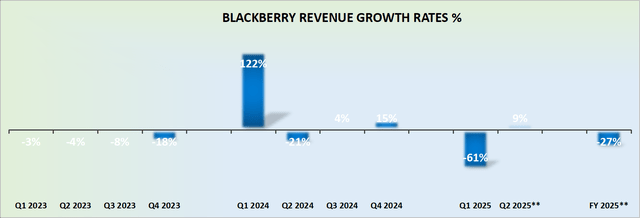

Income Development Charges Stay Underwhelming

BB income progress charges

BlackBerry does not present an easy comparability with the prior yr.

Nevertheless, if we do some tough calculations, we’ll see that by excluding the $218 million from inorganic patent gross sales in final yr’s Q1 2024, its income progress charges have been much less horrendous than the damaging 61% y/y income progress charges introduced within the graphic above.

Extra particularly, BlackBerry’s income progress charges are down 7% y/y, which BlackBerry’s administration reiterates on quite a few events all through the earnings name, was forward of their steering.

This means that whereas the enterprise is struggling, it’s nonetheless in a position to survive. Contemplating the various high-quality companies accessible for funding, I’ve to marvel what the enchantment of investing on this lower-quality enterprise is.

However at the same time as I ask this query, I do know the reply. It is the identical motive buyers have had for years with BlackBerry: the inventory is affordable. Nevertheless, I contend that that is an phantasm, which we’ll discover additional subsequent.

BB Inventory Valuation — 87x This 12 months’s EBITDA

BlackBerry holds about $230 million in money, money equivalents, and marketable securities, and the enterprise has no debt. That is the inspiration of the bullish thesis.

Nevertheless, my argument has been, and continues to be, that BlackBerry’s money solely has worth if the enterprise can use it to drive future worthwhile progress. In any other case, that money has no sensible worth.

BlackBerry has aggressively in the reduction of on its capital expenditures and lowered substantial prices from its operations.

Regardless of this, the latest narrative is that BlackBerry is pivoting in direction of investing in its IoT enterprise. But, with out important funding, how can its IoT enterprise develop? It might’t. For this reason its IoT enterprise was up solely 23% y/y, though it is not even producing $250 million in annual revenues.

In the meantime, Samsara (IOT), a inventory I personal, is projected to develop 30% this fiscal yr and already has $1 billion in revenues. This reinforces that there’s sturdy demand for IoT providers, however BlackBerry is struggling to realize important traction on this extremely aggressive sector.

Moreover, BlackBerry is projecting an adjusted EBITDA of roughly $10 million for fiscal 2025. This implies the enterprise is priced at roughly 87 occasions ahead EBITDA. Is that low-cost? I do not consider so. I consider this inventory is overvalued.

The Backside Line

Paying 87x ahead EBITDA for BlackBerry will not be a sexy funding as a result of the corporate faces important challenges in its key areas of focus, IoT and cybersecurity, whereas failing to point out substantial income progress.

Regardless of having a money reserve and no debt, BlackBerry’s lack of ability to successfully deploy its money to drive worthwhile progress undermines its valuation.

The IoT section’s modest progress and the aggressive pressures within the cybersecurity market additional spotlight the corporate’s battle to realize traction. This inflated valuation, in comparison with the restricted progress prospects and the underwhelming efficiency relative to trade friends, means that the inventory is overvalued. Readers can do higher elsewhere.

[ad_2]

Source link