[ad_1]

mgstudyo/E+ through Getty Photos

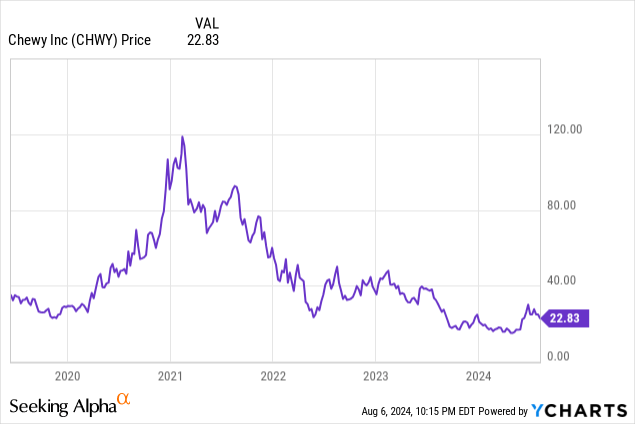

Chewy (NYSE:CHWY) inventory has been in bother for the reason that starting of 2021. After falling greater than 75%, the corporate is lastly producing actual money flows and discovering working leverage. This, mixed with some sluggish progress, makes the inventory a cautious purchase in the intervening time.

What has occurred with CHWY?

Chewy is one in all what I name a traditional pandemic inventory. These are, in my view, corporations that acquired some vital progress in the course of the pandemic period as a result of they solved any logistical downside. Their valuations and inventory costs skyrocketed, solely to fall mercilessly after the world’s actual financial system began to recuperate, and that preliminary progress vanished.

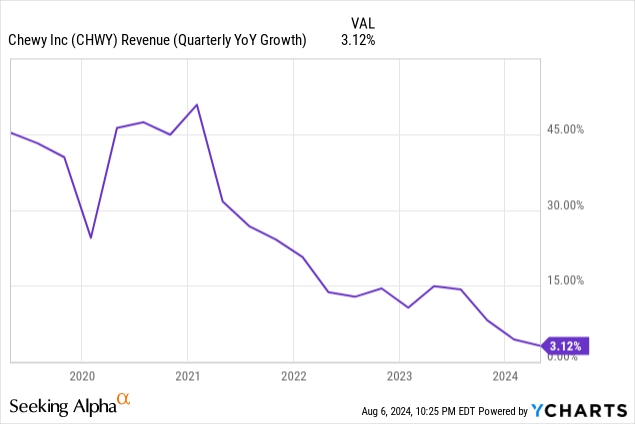

Chewy solved an vital downside: getting meals in your pets with out leaving dwelling. Sadly for Chewy’s shareholders, income progress collapsed after 2021 from 45% to the present 3%.

This fall in income progress, in my view, destroyed the inventory value however finally made Chewy’s administration search for profitability. Now, the corporate counts with actual earnings, though adjusted earnings that exclude share-based compensation have been optimistic since Q1 2022.

Chewy’s enterprise mannequin

Let’s check out the 2023 10K submitting. Chewy is a pet business retailer firm identified primarily for its digital presence across the US. The corporate’s enterprise progress is meant to be supported by long-term traits like pet humanization that improve the quantity spent by purchasers for his or her pets. In line with the doc, Packaged Information tasks this pet market to develop by 7% CAGR till 2027, which may be an fascinating tailwind.

One other vital enterprise attribute of Chewy’s enterprise mannequin is that the pet business is definitely fairly resilient in macroeconomic downturns, as talked about within the doc. The corporate does not experiment seasonality both. Moreover, CHWY is operationally proficient and aggressive, with the ability to serve as much as 80% of America’s inhabitants in a single day and near 100% in simply two days.

Chewy additionally has an vital loyalty program: Autoship, which consists of offering prospects with periodic pet meals and medication shipments whereas additionally offering some reductions. It is a very arduous barrier to interrupt for rivals, in my opinion.

Lastly Working Leverage

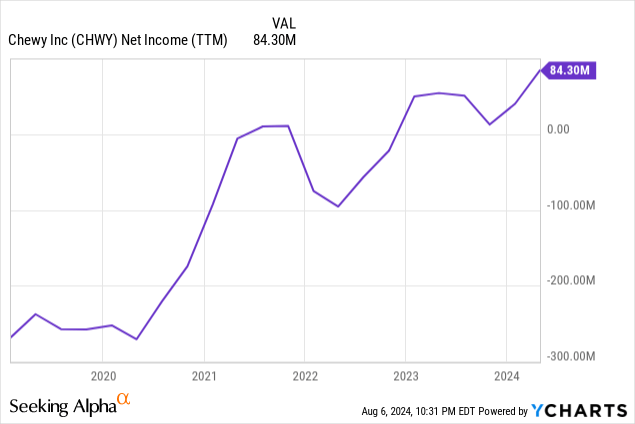

Though working leverage would possibly seem to be a flowery expression, in brief, it refers back to the scenario when an organization can generate extra revenues with out rising its working bills an excessive amount of. That is what Chewy is exhibiting in its newest Q1 2024 earnings outcomes. Right here, Chewy elevated gross sales by a shy 3% YoY, or $87 million, however adjusted earnings elevated by a powerful 56%, or $49 million. This occurred as a result of the corporate elevated working bills by simply $21 million, leaving plenty of area for the underside line to develop.

As talked about earlier than, the corporate has some tailwinds that would proceed driving revenues larger, not less than in a modest method. If the corporate manages to keep away from shedding prospects, I believe this could present a critical alternative for working leverage to develop internet revenue margins considerably.

As an illustration, within the final presentation, Chewy reported that internet gross sales per buyer grew by 9.5%, however the variety of customers fell from 20.4 million to twenty million. It is a bittersweet consequence as a result of, on the one hand, the corporate may purchase income and working leverage, however with few prospects, it’s certainly tougher to forecast wholesome monetary progress in the long run. In any case, in the latest earnings name, the administration expressed that it expects the corporate to develop by round 4-6% by 2024 yr’s finish.

From a steadiness sheet perspective, the corporate shouldn’t be in monetary misery, having a wholesome relationship between present property of $2.12 billion and $2 billion in present liabilities. The corporate doesn’t have long-term debt, however some leases which are effectively coated by long-term property.

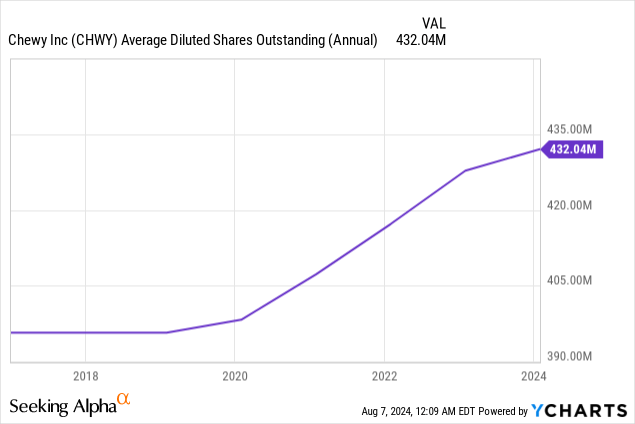

Sadly, the corporate has carried out, and continues to take action, some share dilution. Presently, the dilution tempo is at round 1.5% a yr, which, though annoying, has been in a position to hold the steadiness sheet wholesome and assist the corporate’s money place to be considerably accurately invested. Not too long ago, the corporate introduced that it’s shopping for again $500 million in shares from BC Companions.

What ought to occur with the inventory?

The administration has additionally knowledgeable the general public about some totally different extra tasks for getting new revenues. For instance, Chewy Plus is a subscription mannequin that gives free delivery, amongst different advantages. Presently, this performance is in beta mode. One other fascinating initiative is the Chewy Vet Care Clinics, of which the corporate opened 4 the final quarter. I believe that Chewy Vet can improve revenues finally, not solely from providers, that are a better margin enterprise often than retailing, however from extra gross sales within the standard retailer enterprise.

Contemplating all these components, the inventory has some good views, however it’s nonetheless fairly speculative, in my view. Investing in Chewy may present good outcomes if the corporate continues to extend revenues with working leverage. For this particularly, revenues per buyer must go larger if the full variety of prospects does not develop. In fact, the optimum case situation is rising the shopper base whereas rising income per buyer, however the business appears to have stabilized market shares, in my view.

Now, if income progress shouldn’t be achieved, both by getting new prospects or extra income per buyer, the inventory would possibly stagnate or slowly go down.

Valuation

As I discussed earlier than, I believe there’s a critical, constant path to an funding in CHWY. It is very important keep in mind that this can be a fairly speculative inventory with speculative assumptions, that I contemplate would possibly understand. If, for some motive, the revenues stagnate or start to go unfavorable, it’ll be a tough time for Chewy buyers.

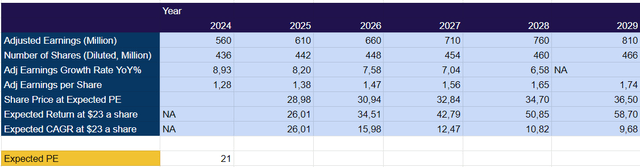

Now, I present a valuation framework with a $50 million improve in nominal earnings from 2024 to 2029. I do that as a result of I need to present a extra conservative perspective on these already speculative assumptions. In any case, if the corporate manages to extend revenues by greater than 5%, I might count on adjusted internet revenue will increase of greater than $150 million year-over-year, which may trigger a major improve within the share value slightly shortly.

Different assumptions I made are a continued 6 million share dilution and a 21 anticipated PE ratio, which may be cheap for a low-growth firm, in my opinion.

Writer

This mannequin throws a near 11% CAGR with these conservative projections on these speculative assumptions. I believe the inventory is a purchase, however buyers should be fairly cautious for the reason that inventory would possibly present some vital volatility if revenues stagnate or the variety of prospects goes down. It is very important bear in mind I’m not contemplating buybacks on this framework mannequin.

Dangers

The principle threat to this funding thesis is that the corporate can’t improve income per person. This could destroy earnings progress and, consequently, contract valuation multiples.

Different vital dangers are modifications typically traits that would impression the shopper base instantly, like much less pet humanization or elevated competitors by different web sites like Amazon or Petco and even brick-and-mortar retailers.

One other uncommon threat is that CHWY has been the epicenter of some meme-stock exercise, which could generate some speedy modifications in volumes and volatility slightly out of the blue. Traders want to pay attention to this funding and never solely let it’s unseen for months.

Conclusion

Chewy is a comparatively strong firm with some vital working leverage alternatives. The corporate has some good tailwinds and is situated in place to capitalize on earnings progress alternatives.

I contemplate the inventory a speculative purchase, though a small place may be applicable in a well-diversified portfolio.

[ad_2]

Source link