[ad_1]

Combining Discretionary and Algorithmic Buying and selling

The realm we need to discover at this time is an fascinating intersection between quantitative and extra technical approaches to buying and selling that make use of instinct and expertise in strictly data-driven decision-making (fully omitting any elementary evaluation!). Can simply years of display time and buying and selling expertise enhance the metrics and profitability of buying and selling methods by means of discretionary buying and selling actions and choices?

An fascinating experiment yielded a stunning outcome: Researchers took a discretionary dealer and gave him a scientific buying and selling technique, permitting him to override alerts based mostly on “intestine instincts”. Discretionary dealer might resolve which sign to take, which to not, and the best way to set cease losses (SLs) and revenue targets (PTs) based mostly on the inventory’s earlier value motion… The outcomes are thus far attractive — the dealer improves a mean non-profitable technique right into a worthwhile one.

How was the experiment arrange?

To make the method rigorous, (Zarattini and Stamatoudis, 2024) used specialised software program to anonymize charts and get rid of extraneous data to make sure an unbiased analysis of the dealer’s choices. By rigorously analyzing 9,794 hole occasions from 2016 to 2023, they demonstrated that the instinct of skilled merchants can improve the profitability of buying and selling methods. The important thing findings reveal that when shares hole up, making use of discretionary buying and selling choices, carried out on this investigation utilizing specialised anonymizing software program, results in substantial enhancements in buying and selling efficiency. The discretionary dealer’s number of roughly 18 % of the hole occasions leads to increased common commerce profitability than purely mechanical approaches. The discretionary dealer’s capability to acknowledge favorable patterns, comparable to early gaps in momentum cycles and multi-week or multi-month vary breakouts, performs a pivotal function in bettering commerce choice. Elementary the explanation why inventory reacted with the hole should not that vital. All in all, it boils right down to place administration and rigorous setting of cease losses and risk-taking.

This underscores the vital function of instinct and expertise in figuring out and capitalizing on market alternatives that automated methods may overlook. The structured (micro)administration methods, comparable to exact entry factors, cease losses, and revenue targets, additional improve commerce outcomes by optimizing risk-reward ratios and making certain disciplined commerce execution. This revolutionary method isolates the results of bias from exterior elements and prevents any forward-looking bias, permitting the dealer’s discretionary instinct to be integrated right into a quantitative empirical investigation. The cumulative PnL achieved on the discretionarily chosen and traded gaps exhibits a major progress trajectory, with the hypothetical portfolio attaining a complete return of practically 4,000% over eight years. This efficiency demonstrates the potent mixture of human instinct and systematic buying and selling guidelines.

Authors: Carlo Zarattini and Marios Stamatoudis

Title: The Energy Of Value Motion Studying

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4879527

Summary:

Evaluating the effectiveness of technical evaluation has all the time been a difficult job. Translating every technical sample right into a quantifiable measure is commonly unfeasible, resulting in the notion of technical evaluation as extra artwork than science. Proving its utility rigorously stays elusive. This examine goals to analyze the worth added by incorporating discretionary technical buying and selling choices throughout the context of shares experiencing vital in a single day gaps. By making a bias-free simulated buying and selling atmosphere, we assess the profitability enchancment of a easy computerized buying and selling technique when supported by an skilled technical dealer. The dealer’s function is to limit the algorithm to commerce solely these shares whose each day charts seem extra promising. Moreover, we conduct a check the place the skilled dealer micromanaged the open positions by analyzing, in a bias-free atmosphere, the each day and intraday value motion following the in a single day hole. The outcomes introduced on this paper recommend that discretionary technical buying and selling choices, no less than when performed by a talented dealer, might considerably improve buying and selling outcomes, reworking seemingly unprofitable methods into extremely performing ones. This paper gives empirical proof supporting the combination of discretionary judgment with systematic buying and selling approaches, providing worthwhile insights for enhancing buying and selling outcomes in monetary markets.

As all the time we current a number of fascinating figures and tables:

Notable quotations from the tutorial analysis paper:

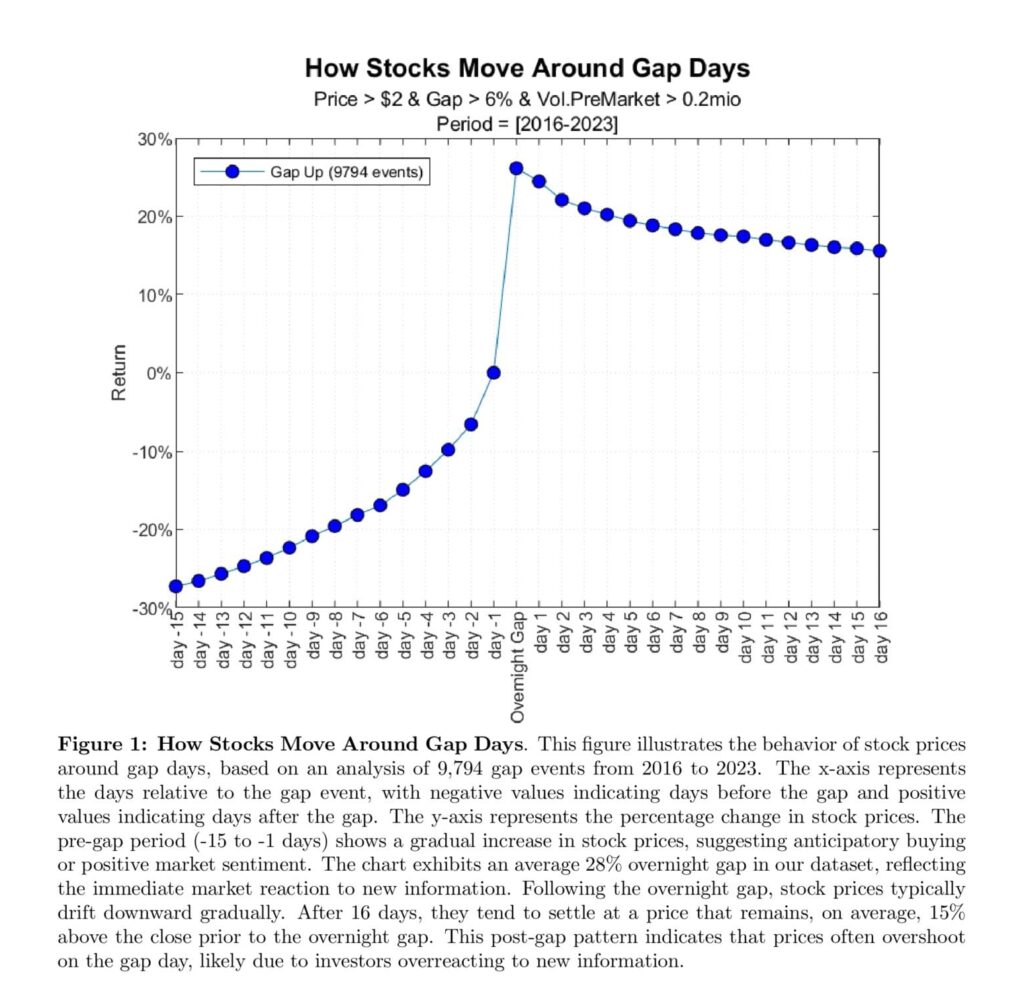

“Outcomes are exhibited in Determine 1. Pre-Hole Habits (-15 to -1 days)

Within the fifteen days previous a spot occasion, inventory costs exhibit a gradual improve, ranging from roughly -26% and transferring in the direction of 0%. This pattern suggests a interval of anticipatory shopping for or constructive market sentiment. Merchants probably place themselves forward of anticipated constructive information, contributing to a gentle value rise. The development from -26% to 0% signifies a scientific build-up in inventory costs as market contributors reply to alerts and data that precede the hole occasion.

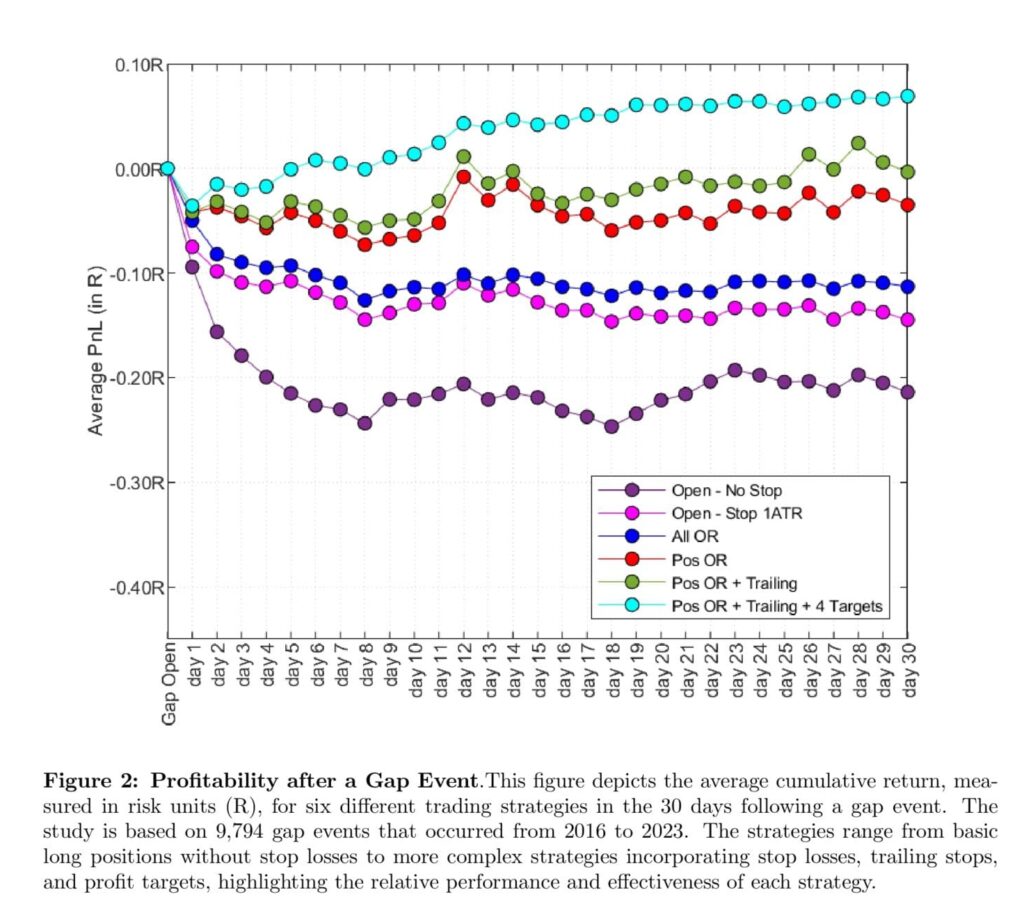

The profitability of every technique is assessed over a 30-day interval, considering various inventory volatilities. Profitability is measured by way of the commerce danger unit (R), offering a standardized metric to match efficiency throughout totally different methods. For instance, if a commerce is entered at $100 with a cease positioned at $98, the implied danger unit is $2. If after n days the unrealized PnL is $8, it’s thought of a PnL of 4R ($8/$2). For the Open – No Cease technique, the chance unit is about to 1 ATR.

As exhibited in Determine 2, the technique of shopping for all gaps with no cease loss, denoted as Open – No Cease, demonstrates a major damaging edge, with cumulative each day losses reaching a minimal of -0.25R after 8 days. This means that buying and selling with no cease loss might result in constant losses.

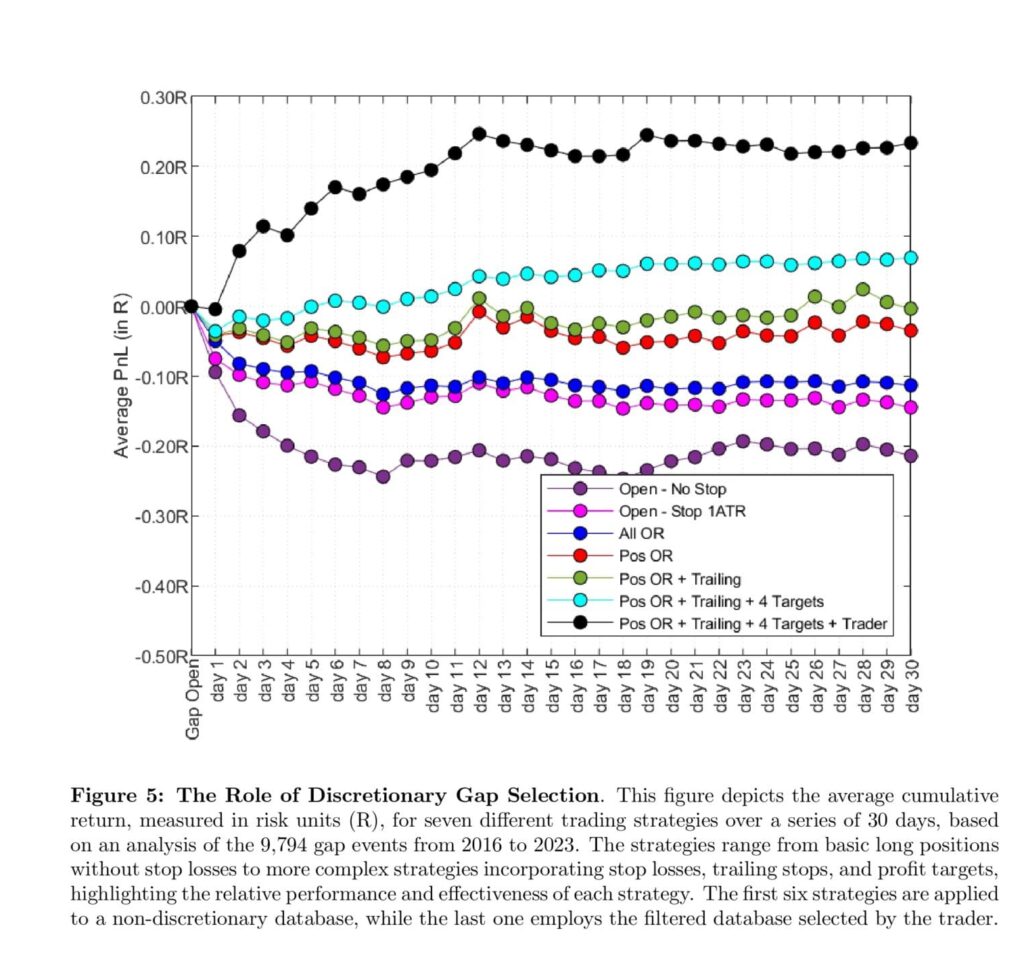

Determine 5 depicts the efficiency trajectory of this technique, termed Pos OR + Trailing + 4 Targets + Dealer. The typical profitability demonstrates a marked enchancment, because it will increase progressively, reaching a peak at 0.25R, 12 days after the entry day (the hole day). This consequence means that the discretionary choice by an skilled technical dealer can improve the profitability of an in any other case unproductive rule-based buying and selling technique.

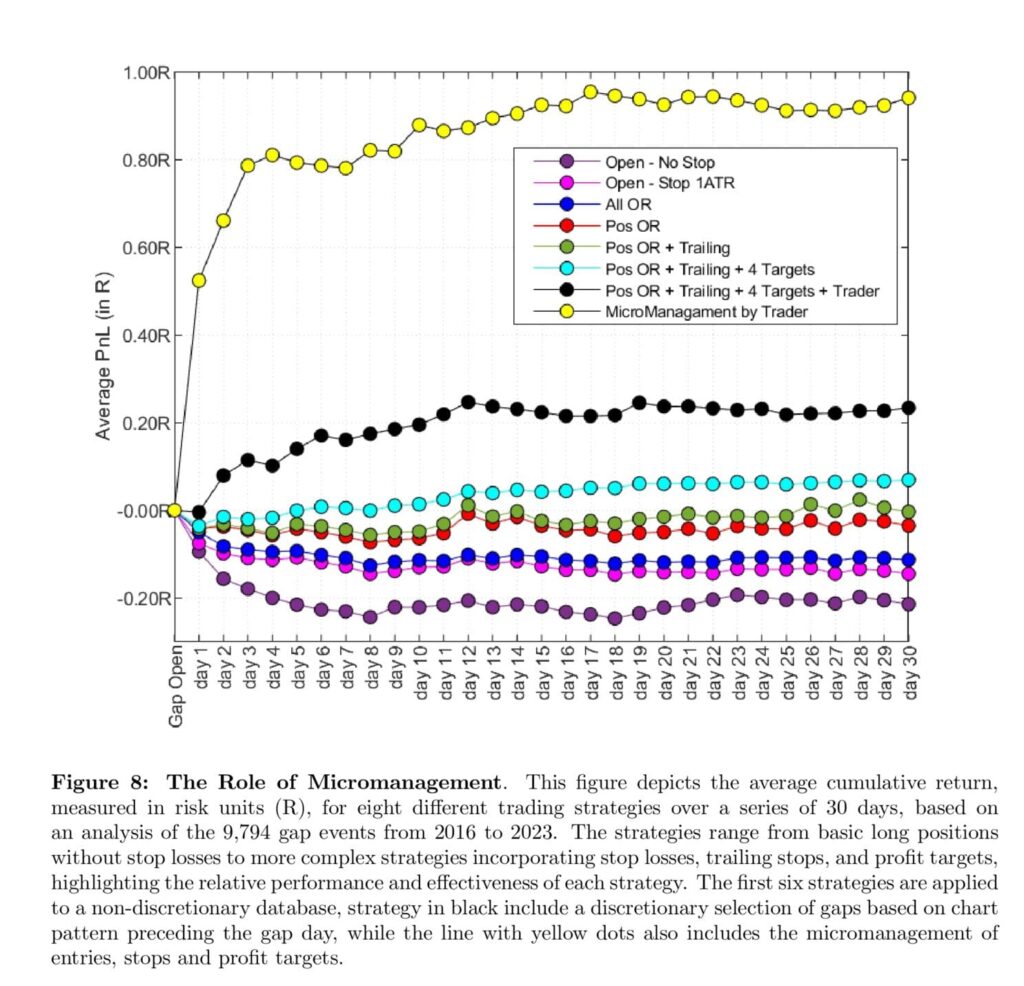

By utilizing the database of all of the trades taken and micromanaged by the dealer within the bias-free atmosphere, we replace Determine 5 and plot the typical cumulative PnL in R-multiples. As proven in Determine 8, there’s a vital enchancment within the common profitability. The typical profitability on the hole day will increase to 0.55R, reaching an area most of 0.80R on day 4. After 3 days of a shallow pullback, profitability begins rising once more, however at a slower charge. That is probably as a result of the dealer permits the total place to run for the primary three days, then reduces danger by taking partial income and letting 1 / 4 place path on an extended transferring common.

As recommended by the dealer, these trades are normally sized in order that if a cease loss is hit, the ensuing loss on the portfolio stage equates to 0.25%. We thus remodel the cumulative PnL time-series right into a financial time-series, assuming an preliminary fairness of $100,000 and a danger funds per commerce of 0.25%. The trajectory of the simulated account is exhibited in Determine 10. A $100,000 portfolio grows to greater than $4,000,000, yielding a complete return of three,968% in 8 years.”

Are you on the lookout for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you need to study extra about Quantpedia Premium service? Examine how Quantpedia works, our mission and Premium pricing supply.

Do you need to study extra about Quantpedia Professional service? Examine its description, watch movies, evaluation reporting capabilities and go to our pricing supply.

Are you on the lookout for historic knowledge or backtesting platforms? Examine our listing of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookSeek advice from a good friend

[ad_2]

Source link

, Boeing (NYSE:BA)")

, BrandywineGLOBAL-Dynamic US Large Cap Value ETF (NASDAQ:DVAL)")

{kind=link}