[ad_1]

The monetary sector is seeing an increase in challenger suppliers focusing on the distinctive wants of its 47M+ immigrant inhabitants in america. These innovators are addressing key challenges immigrants face in banking, reminiscent of constructing credit score, overcoming language obstacles, and accessing appropriate cost providers. Comun, a digital banking platform, stands out on this house by providing immigrant-focused monetary providers. Their choices embrace no-fee accounts with no minimal steadiness necessities, entry to an enormous money deposit community, and remittance providers to seventeen Latin American nations. This strategy has resonated strongly, leading to a formidable 52% month-over-month development in lively prospects since launching. By tailoring their providers to the precise wants of immigrant communities, Comun will not be solely tapping into a big market alternative but additionally selling higher monetary inclusion in america.

AlleyWatch caught up with Comun Cofounder and CEO Andres Santos to be taught extra concerning the enterprise, the corporate’s strategic plans, newest spherical of funding, which brings the corporate’s whole funding raised to $26M, and far, rather more…

Who had been your traders and the way a lot did you increase?Our traders had been Redpoint Ventures, ANIMO Ventures, Costanoa Ventures, FJ Labs, RTP International, and South Park Commons. Redpoint Ventures led our Sequence A funding spherical of $21.5M.

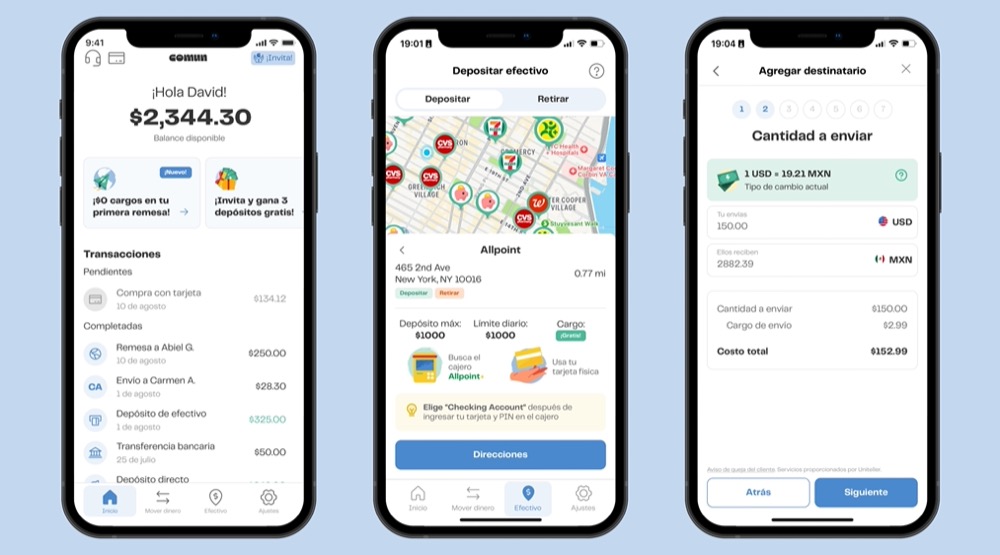

Inform us concerning the services or products that Comun provides.At Comun, we provide an inclusive, low-fee, digital monetary resolution that features an FDIC-insured US checking account, VISA debit card, instantaneous remittance service, entry to Zelle, and entry to the most important money deposit community within the U.S., all accessible through a user-friendly, Spanish-first cellular app.

What impressed the beginning of Comun? My cofounder, Abiel Gutierrez, and I had been impressed to start out Comun after going through monetary exclusion within the U.S. once we migrated from Mexico. Once we each got here to the US to review, we confronted a number of challenges opening a checking account, from a language barrier to ID necessities.As we appeared into this matter, we discovered the Latino group has been underserved in accessing monetary services that match their distinctive wants. Many don’t have social safety numbers or credit score scores within the US, so the extra conventional methods banks assess and perceive potential prospects don’t work for this group. Along with these obstacles, entry to monetary providers within the US may be extraordinarily pricey. Latinos are 3x extra more likely to go unbanked and pay a mean of 5x greater charges for fundamental providers. All these elements, together with our personal experiences, impressed us to start out Comun. We need to present all Latinos within the US with easy-to-access and reasonably priced banking options and assist them obtain upward mobility.

My cofounder, Abiel Gutierrez, and I had been impressed to start out Comun after going through monetary exclusion within the U.S. once we migrated from Mexico. Once we each got here to the US to review, we confronted a number of challenges opening a checking account, from a language barrier to ID necessities.As we appeared into this matter, we discovered the Latino group has been underserved in accessing monetary services that match their distinctive wants. Many don’t have social safety numbers or credit score scores within the US, so the extra conventional methods banks assess and perceive potential prospects don’t work for this group. Along with these obstacles, entry to monetary providers within the US may be extraordinarily pricey. Latinos are 3x extra more likely to go unbanked and pay a mean of 5x greater charges for fundamental providers. All these elements, together with our personal experiences, impressed us to start out Comun. We need to present all Latinos within the US with easy-to-access and reasonably priced banking options and assist them obtain upward mobility.

How is Comun totally different?Prospects can open an account with over 100 IDs from Latin America – now we have a really complete KYC system that has allowed us to take away lots of the friction factors immigrants usually face whereas additionally blocking fraudulent actors.

Our accounts don’t embrace charges – There’s a $0 opening price, $0 minimal steadiness, $0 month-to-month price, and $0 membership price.

One of many largest and reasonably priced money networks – our customers can deposit and withdraw money at ~100k places across the US without spending a dime or at industry-leading costs.

Worldwide transfers (remittances) to 17 nations in Latin America – members of the family in LATAM can obtain funds at a checking account or via a money community of over 300k retailers throughout the area at industry-leading costs in comparison with incumbents like Western Union.

Spanish-first buyer help – prospects can contact Comun 24/7 by telephone, e mail, chat, and WhatsApp with native audio system.

Peer-to-peer instantaneous cost community – prospects of Comun can ship cash simply to family and friends who even have Comun accounts for no price.

What market does Comun goal and the way large is it?At Comun, our mission is to empower immigrants and their households to show their exhausting work into upward mobility. At present, the Hispanic inhabitants within the U.S. is greater than 63M and is anticipated to succeed in 111M by 2060.

What’s your enterprise mannequin?Just like different fintech providers like Chime, our income comes from interchange charges and different product choices like our remittance program and money deposit community.

How are you getting ready for a possible financial slowdown?We’re lucky that our remittance service and expanded money deposit community have diversified our income streams, decreasing our reliance on interchange charges and demonstrating resilience towards 2025’s unsure macroeconomic headwinds. Our focus this yr is to proceed providing the most effective product expertise and increasing our remittance program into different nations in Latin America. We now have additionally been very considerate in increasing our group and have remained lean regardless of our development.

What was the funding course of like?To be frank, we weren’t seeking to increase our subsequent spherical. We began receiving preemptive provides from traders, which led us to launch a full course of. We acquired considerably extra curiosity than we might settle for, and each earlier investor determined to double down.

What are the most important challenges that you simply confronted whereas elevating capital?We really feel very lucky that our traders consider in our mission, which sparked this funding spherical.

What elements about your enterprise led your traders to put in writing the test?We acquired constructive suggestions from our traders. A standard theme amongst traders was our development. Many VCs informed us that we had been one of many fastest-growing shopper fintech corporations that they had seen lately. We had been additionally informed we had superior unit economics than most different corporations they evaluated.

What are the milestones you propose to realize within the subsequent six months?We now have aggressive objectives set for this yr that may assist deepen our relationship with our prospects. That features offering prospects with further options on how they fund their accounts, enhancing our fraud detection capabilities, ensuring each buyer has an incredible product expertise, and together with extra nations in Latin America the place prospects can ship cash.

What recommendation are you able to provide corporations in New York that do not need a recent injection of capital within the financial institution?Be laser-focused on what really issues. At Comun, we stripped away something non-essential and zeroed in on our core mission. We stayed near our prospects and ruthlessly prioritized solely what would considerably transfer the needle. In powerful occasions, the flexibility to prioritize ruthlessly could make all of the distinction.

The place do you see the corporate going now over the close to time period?We envision Comun because the one-stop trusted monetary companion for immigrants within the US. Nevertheless, to get there, we acknowledge that immigrants want entry to credit score options, the information on learn how to construct an incredible credit score rating and ongoing monetary recommendation, whether or not it’s round saving for retirement, shopping for a home, or constructing an emergency fund. We consider we’re well-positioned to grow to be that trusted companion for our prospects.

What’s your favourite summer time vacation spot in and across the metropolis?I like occurring highway journeys with my spouse and daughter and discovering new locations round New York. There’s at all times one thing new to discover only a brief drive from town.

[ad_2]

Source link

{kind=link}