[ad_1]

Designing Strong Pattern-Following System

It isn’t simple to construct a strong trend-following technique that may stand up to completely different troublesome market situations and produce constant outcomes. The creator of at the moment’s work was not frightened by this job and delivered a full framework on how you can design a strong trend-following technique step-by-step.

The strategy presents sensitivity evaluation and robustness checks by numerous time horizons and pattern selections. It additionally accounts for transaction prices (when one rebalances typically, they creep in and eat out a big chunk of income) and takes a multi-asset strategy to maximise intently watched threat metrics from PMs (portfolio managers).

Dobromir Tzotchev’s framework might be summarized into the next steps:

Want for a clear Pattern-following Sign: The paper proposes a trend-following time-series momentum sign based mostly on statistical concept and investigates its properties. It reconciles theoretical outcomes with stylized details about trend-following investing, together with the hyperlink to straddles and the higher efficiency of so-called “slower” indicators.

Sound Design and Prototype Answer: Based mostly on theoretical outcomes, the paper introduces a prototype trend-following resolution that makes use of a unified strategy throughout belongings and diversifies throughout time frames. By simulation examples, it highlights efficiency versus benchmarks and diversification properties for long-only portfolios.

Threat Administration Strategies: The paper elaborates on portfolio and threat administration for trend-following methods. It adapts risk-budgeting and Hierarchical Threat Parity (HRP) approaches to the trend-following framework. Moreover, it discusses strategies to handle transaction prices and implications of the carry element in futures and FX forwards.

Authors: Dobromir Tzotchev

Title: Designing Strong Pattern-following System: Behind the Scenes of Pattern-following

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4677166

Summary:

Pattern-following has actively been on traders’ radar for the previous few a long time. The J.P. Morgan primer on momentum methods (Kolanovic and Wei, 2015) supplies an in depth overview of the momentum methods. The present paper focuses on a concrete trend-following resolution and analyzes its properties alongside the sensible implementation.

As at all times we current a number of fascinating figures and tables:

Notable quotations from the tutorial analysis paper:

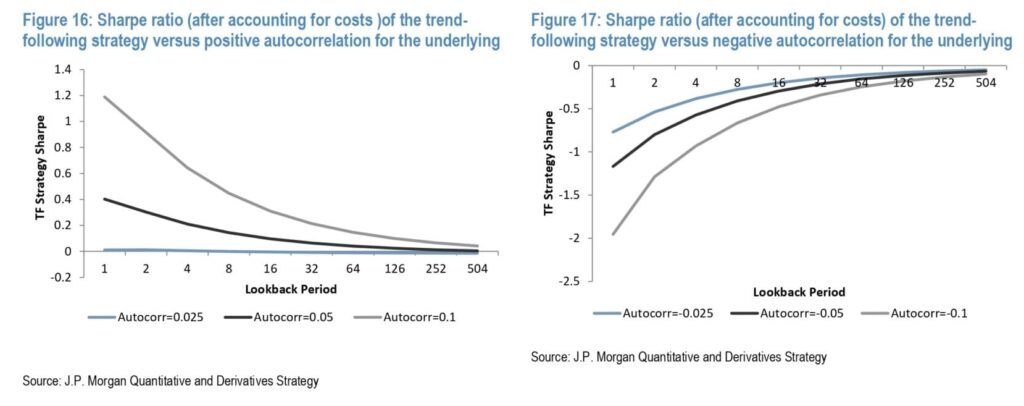

“We begin by presenting a sign that’s based mostly on statistical speculation testing. We present that underneath sure situations the trend-following sign is the additionally the delta of a straddle. Therefore we make express the extensively propagated hyperlink between trend- following and lengthy straddle positions (see for instance Fung and Hsieh 2011).Subsequently, we analyze the revenue drivers for the trend-following technique based mostly on the proposed sign. We present that the technique (equally to a straddle) is worthwhile at any time when there are traits in both path. Therefore we show that the so-called “CTA smile” (see for instance Hurst et. al. 2014) might be justified inside a theoretical mannequin as effectively. Moreover, the technique displays convexity. Absolutely the worth of the Sharpe ratio of the underlying asset is of important significance for the profitability of the technique and the upper the quantity, the larger the convexity embedded within the technique. Moreover, indicators based mostly on longer estimation intervals possess ceteris paribus higher profitability than indicators based mostly on shorter lookback intervals.Subsequent, the time-series properties of the underlying asset are explicitly taken into consideration. We present that the autocorrelation is vital just for the profitability of indicators based mostly on quick lookback intervals (sometimes lower than a month). Naturally constructive autocorrelation results in income whereas even small values of adverse autocorrelation induce substantial losses. Then again the profitability of the indicators based mostly on longer lookback intervals is unaffected by the time-series properties of the underlying.

Because of the non-linear nature of the expressions for the anticipated P&L and transaction prices, it’s troublesome to derive the brink Sharpe ratio of the underlying that renders the profitability of a sign based mostly on a sure lookback interval. However, numerical outcomes shed some fascinating caveats for this relationship. In Determine 13 we have now plotted the Sharpe ratio based mostly on the web P&L of the trend-following technique versus the Sharpe ratio of the underlying for numerous lookback intervals. We use the transaction value construction for S&P and assume a each day volatility of 1% (roughly 16% annualized). It’s evident that indicators based mostly on quick time period lookbacks can solely be worthwhile if the Sharpe ratio of the asset is sort of sizable in both path. For instance, for a sign based mostly on 2 days we’d like a Sharpe ratio above 2 and under -2 to guarantee the profitability of the technique. For a sign based mostly on 32 days, the Sharpe ratio needs to be above 1 or under -1. Even a sign based mostly on a 1 yr lookback interval requires absolutely the worth of the Sharpe ratio to be larger than 0.5 in order that profitability is assured.

Moreover, we count on the Sharpe ratio of trend-following technique to be under absolutely the worth of the Sharpe ratio of the asset. A large constructive or adverse Sharpe ratio of the underlying and long run lookback interval are each needed for the Sharpe ratio of the trend-following technique to exceed absolutely the worth of the Sharpe of the underlying. For instance, we’d like the Sharpe ratio of the underlying to be larger in absolute worth than 1.5 in order that trend-following is extra worthwhile than both holding or shorting the asset.If the drift of the asset is steady (stays fixed over an extended interval), it’s way more worthwhile and cost-efficient to make use of indicators based mostly on longer lookback intervals. For instance, if we count on equities to exhibit a constructive drift because of the embedded fairness threat premia, it’s preferable to make use of indicators with longer lookback intervals. The attraction of the shorter time period lookback intervals arises in two eventualities. Firstly, the period of the development may be smaller than an extended lookback interval. For instance, if the development modifications path each 6 months making use of a sign based mostly on 1 yr lookback might be detrimental. Secondly, throughout market reversals indicators based mostly on shorter lookback intervals are extra reactive and ultimately mitigate the drawdowns of the slower trend-following methods.

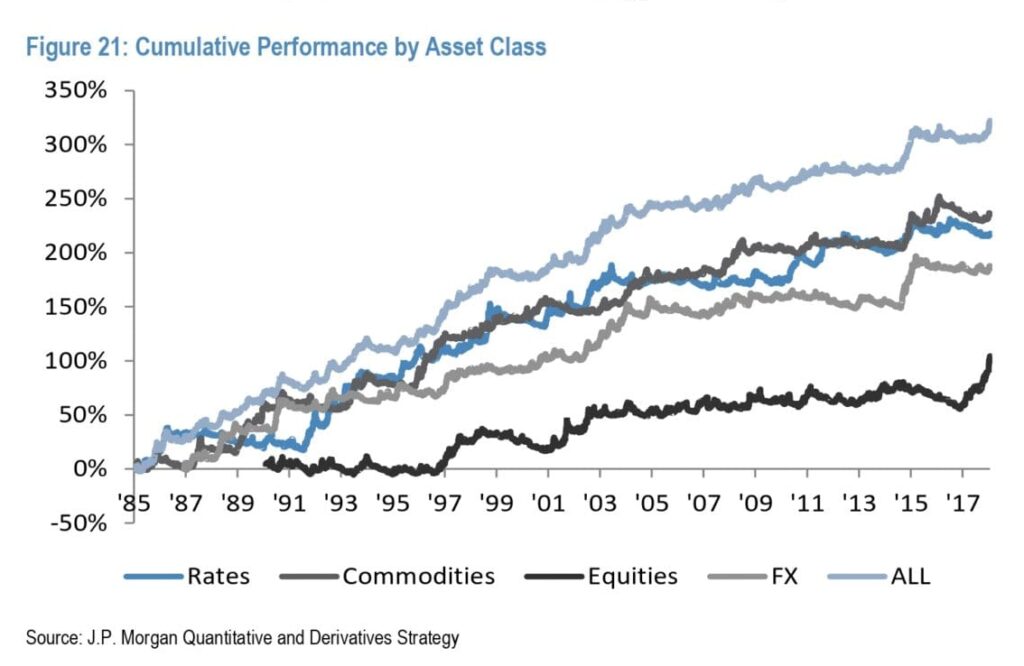

[On Figure 21: Cumulative Performance by Asset Class] the cumulative efficiency of the benchmark strategy in numerous asset courses in addition to the efficiency of the mixed portfolio are shown14. Commodities have traditionally had probably the most interesting trend-following track-record (commodities are additionally the asset class upon which the CTA trade originated). The asset class that has been traditionally been probably the most difficult for the trend-following strategy is equities.

Along with the enticing function of constructive skewness that the trend-following methods possess, trend-following methods deliver substantial diversification advantages for the long-only portfolios. As we have now already proven within the theoretical sections, trend-following methods exhibit convexity and when the transfer on the draw back is sizable sufficient the return of the trend-following technique will greater than compensate the loss within the underlying. It has additionally been well-known that the magnitude of the sell-offs is usually fairly sizable and subsequently the offset with the trend-following methods is sort of interesting.To confirm this speculation empirically we have now constructed portfolios that include lengthy positions within the underlyings from our asset universe. The portfolios are effectively focused to have an annualized volatility of 10% and make the most of the identical threat weights for the person belongings as in our benchmark resolution. We now have additionally constructed mixed portfolios that make investments 50% within the long-only portfolio and 50% within the trend-following system. The diversification advantages are fairly evident in all asset courses aside from mounted revenue. In mounted revenue, the directionality of the market has led to a whole lot of overlap between the positions of the trend-following system and people of the long-only portfolio.”

Are you on the lookout for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you need to study extra about Quantpedia Premium service? Verify how Quantpedia works, our mission and Premium pricing provide.

Do you need to study extra about Quantpedia Professional service? Verify its description, watch movies, overview reporting capabilities and go to our pricing provide.

Are you on the lookout for historic knowledge or backtesting platforms? Verify our record of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookSeek advice from a pal

[ad_2]

Source link

, Boeing (NYSE:BA)")

")

{kind=link}