[ad_1]

Joe Hendrickson

Quite a lot of shares are buying and selling at very excessive premiums proper now. The economic system is doing nice, the inventory market is doing nice. Discovering simple worth shares is not really easy proper now, and now we have to search for corporations which might be in a superb place to return worth to shareholders, even at larger costs.

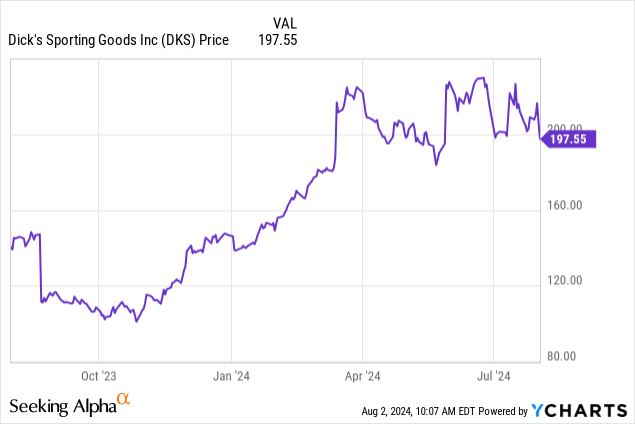

Immediately we’ll be taking a look at DICK’S Sporting Items (NYSE:DKS), an organization that’s buying and selling effectively on the north-end of the 52-week vary. We’ll be taking a look at them from a perspective of dividend development, inventory buybacks, and whether or not the potential return to buyers from their robust money steadiness is value paying the excessive costs the inventory is accessible at proper now.

Understanding DICK’S

DICK’S Sporting Items is a Pennsylvania-based chain of retail sporting items shops that features Golf Galaxy and different specialty idea shops. They’ve round 900 shops total nationwide.

10-Ok from SEC

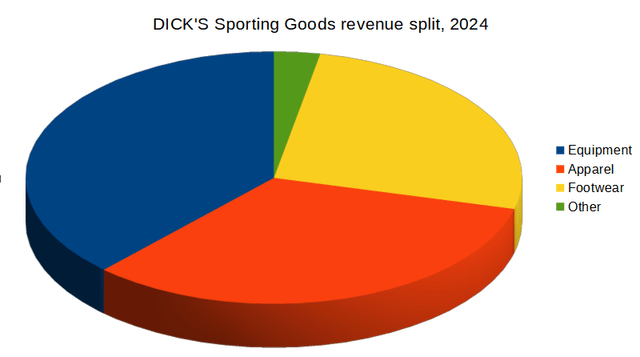

The corporate sells sports activities gear, attire, footwear and equipment. They promote a variety of model names, and have their very own home manufacturers for varied merchandise. The corporate sells at pretty stable margins which have remained roughly constant lately.

Along with the ever present DICK’S Sporting Items shops across the nation, the corporate is pushing some greater shops known as DICK’S Home of Sport. There are solely a handful of such shops proper now, however the firm says they intend to develop the quantity considerably within the subsequent few years.

Stability Sheet

Money and Equivalents

$1.65 billion

Complete Present Belongings

$5.16 billion

Complete Belongings

$9.7 billion

Complete Present Liabilities

$3.02 billion

Complete Lengthy-Time period Liabilities

$3.99 billion

Complete Shareholders’ Fairness

$2.69 billion

Click on to enlarge

(supply: most up-to-date 10-Q from SEC)

DICK’S Sporting Items has a reasonably stable steadiness sheet, and an interesting amount of money readily available. After surging costs in current months, the corporate is buying and selling at a reasonably substantial premium to e-book worth, with a worth/e-book about 6.20. They are going to have to indicate a variety of potential for development and earnings to justify such a premium.

The factor that is most interesting to me in regards to the steadiness sheet is the quantity of free money readily available. That is essential for returning worth to shareholders, within the type each of a rising dividend yield and potential share buyback applications, which we’ll cowl later.

The Dangers

All the pieces is developing roses for DICK’S Sporting Items, however there are nonetheless some considerations to look out for going ahead.

Sporting items are an intensely aggressive enterprise, and DICK’S has to compete not simply with different sporting items shops but additionally common retailers, on-line sellers, and probably most difficultly, distributors who’re beginning to promote direct to prospects, chopping retailers out of the image completely.

The inflationary atmosphere can be an issue, making product prices unpredictable. Will increase in prices may drive producers to move the prices on to retailers, and customers, which may have an effect on demand.

And that might be very tough for DICK’S, as adjustments in demand and purchasing patterns are exhausting to foretell, particularly when the corporate has been attempting to foretell what prospects are going to need to purchase to inventory in practically 900 shops across the nation. That is at all times going to be an issue, however up to now, DICK’S has been in a position to deal with it.

Statements of Operations – Rising the Enterprise

2022

2023

2024

2025 (Q1)

Internet Gross sales

$12.3 billion

$12.4 billion

$13.0 billion

$3.0 billion

Gross Revenue

$4.7 billion

$4.3 billion

$4.5 billion

$1.1 billion

Internet Revenue

$1.52 billion

$1.04 billion

$1.05 billion

$275 million

Diluted EPS

$13.87

$10.78

$12.18

$3.30

Click on to enlarge

(supply: most up-to-date 10-Ok and 10-Q from SEC)

As you possibly can see, DICK’S Sporting Items has seen its internet gross sales improve usually lately, and estimates are that that is going to proceed, with $13.24 billion anticipated within the present fiscal 12 months, $13.8 billion in 2026, and $14.5 billion in 2027. That may be a robust stage of development for an organization that’s already the largest sporting items chain in the US.

Earnings can be rising too, per estimates, with EPS at $13.73, $14.72 and $15.80, respectively. This places the P/E ratio of the present firm at round 14.42. That is not a foul ratio when one considers the inventory is buying and selling at such a premium to its e-book worth.

Later this month, DICK’S will announce its second quarter earnings launch, which is estimated at $3.42 billion and an earnings per share of $3.78. The corporate has been fairly spot on in making good on these estimates, although the earnings surprises have been constructive in current quarters, so there may be room for them to beat this time.

Returning Worth to Shareholders

Within the calendar 12 months 2023, DICK’S Sporting Items repurchased 5.4 million shares at a value of $648.6 million. That is $120 a share, fairly a premium to pay for the corporate, although fairly a bit cheaper than the place it trades now. That reveals some robust confidence within the firm going ahead. There’s a remaining authorization of $779.6 million, although it’s uncertain any repurchases will happen whereas the inventory is buying and selling in its present vary.

The as soon as place the place DICK’s may actually enhance return is dividends. They at the moment pay $1.10 per quarter, which is a yield of about 2.2%. That is a rise from $1.00 per quarter the prior 12 months. With $1.65 billion within the financial institution and earnings rising like they’ve been, they will actually afford to extend the payout going ahead, which makes this a possible dividend development decide.

Conclusion

I actually like DICK’S Sporting Items, they’ve turn out to be a formidable market chief within the sporting items market and are strongly worthwhile. The corporate has a superb money place and is ready to begin rising dividends at a constant charge in the event that they so select.

The one draw back to the inventory that I see is that it’s buying and selling up to now above its 52-week lows. They’ve pulled again a bit off their highs, however the inventory continues to be buying and selling at a wealthy premium, which I see because the distinction between a purchase and a maintain. Proper now, I am taking a look at maintain.

However like I say, I actually like DICK’S, and I will be conserving a detailed eye on the inventory with a hope that it’ll fall right into a extra pleasant purchaser’s vary. Beneath $150 per share, I’ll begin to be very .

[ad_2]

Source link