[ad_1]

Pgiam/iStock by way of Getty Photos

Funding thesis

Dream Finders Properties (NYSE:DFH) has publicity to high-growth development markets and operates an “asset-light acquisition technique”, per firm filings. It’s within the enterprise of constructing and promoting single-family houses throughout a spread of factors alongside the worth chain, particularly 1) entry-level, 2) first-time move-up, 3) second-time move-up, and 4) the marketplace for actively looking for adults. A key issue that drew me to DFH is its tolerable debt load [1.3x debt/equity end of Q2] and the substantial runway that administration can deploy funds over into the long run better off over homebuilding business friends. Critically, the enterprise’s main capital commitments to develop are in working capital (vs. tangible/fastened belongings) as properly, including to the funding economics in my opinion.

I a purchase on DFH on account of 1) administration reinvesting ~75% of NOPAT on avg. at >12% ROICs with intensive runway on this, 2) embedded expectations impartial as finest [1.5x EV/IC, price momentum curled over], however 3) high quality + implied valuations are excessive getting us to $43–50/share on a number of valuation estimates. Internet-net, charge purchase.

Determine 1.

TradingView

Enterprise traits

For my part, the corporate’s working mannequin is good to uniquely place it properly in a difficult macroeconomic atmosphere marked by an unsure inflation/charges axis. Critically, the Infrastructure Funding and Jobs Act (2021) approved $550Bn of infrastructure + development spending and $1.2 Trillion for transportation and infrastructure spending in complete. These are gargantuan numbers which have any clever portfolio supervisor taking a look at homebuilding and/or development shares on account of this financial tailwind.

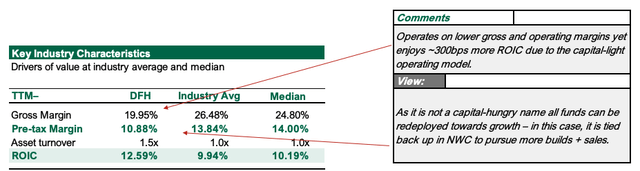

We have seen proof for this in DHF since FY’21 as ROICs are +360bps to 12.6% within the trailing 12mo constructed from ~200bps post-tax margin and ~0.2x development in capital turns. The enterprise is each extra worthwhile and extra environment friendly. The listed homebuilding business is comparatively small with quite a few operators. DFH’s working is not a capital hungry one, in contrast to many friends that allocate surplus money flows in the direction of purely fastened and/or tangible. DFH’s focus is on 1) fast turnover of capital [via affordable “move-ins”] and a pair of) complementing this with gross sales incentives to cut back prices for consumers. Merely, customers have a bonus utilizing DHF’s providers in my opinion. This mannequin ensures the enterprise operates on decrease gross and working margins vs. friends but enjoys ~300bps extra ROIC than the business avg. as a result of capital-light working mannequin [seventh behind (NVR), (PHM), (IBP), (GRBK), (BLD), (DHI) and (TOL), respectively].

Determine 2.

Searching for Alpha

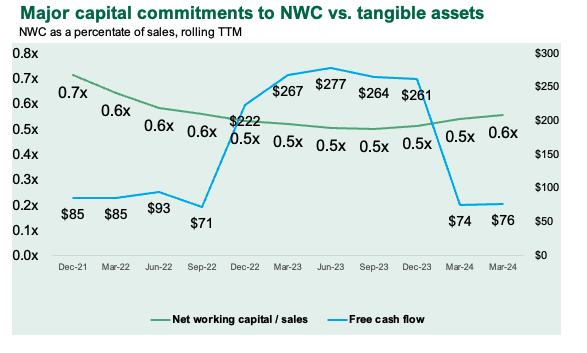

As a result of it isn’t a capital-hungry title all funds could be redeployed in the direction of development – on this case, it’s tied again up in NWC to pursue extra builds + gross sales. NWC averages >0.5x gross sales each rolling 12mo (Determine 3) and was as excessive as 0.7x with the pull-through of the IIJA. DFH throws off ~$75–$90mm in FCF every interval as properly and has redeployed freely obtainable funds produced all through FY’22/’23 again into the enterprise [reinvestment rates jumped to >75% in FY’23/’24 vs. <50% previously]. This creates a optimistic flywheel the place 1) funds are put to work within the working cycle as WC, 2) gross sales + earnings are acknowledged on these investments, and three) producing FCFs to repeat the method.

Determine 3.

Firm filings, Creator

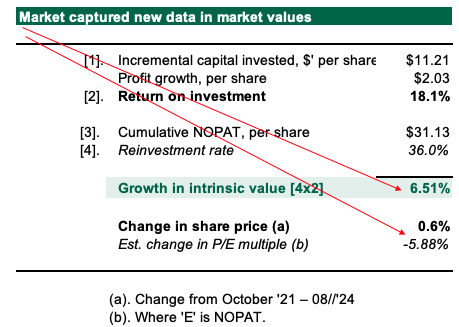

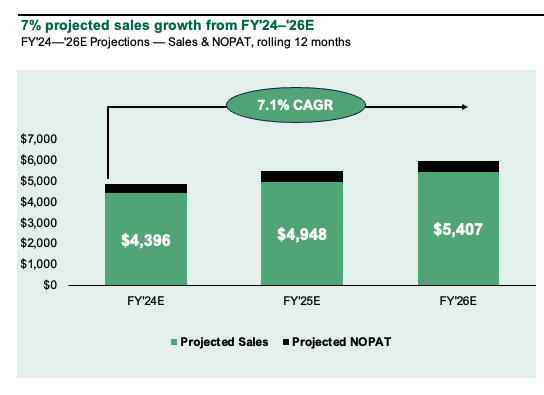

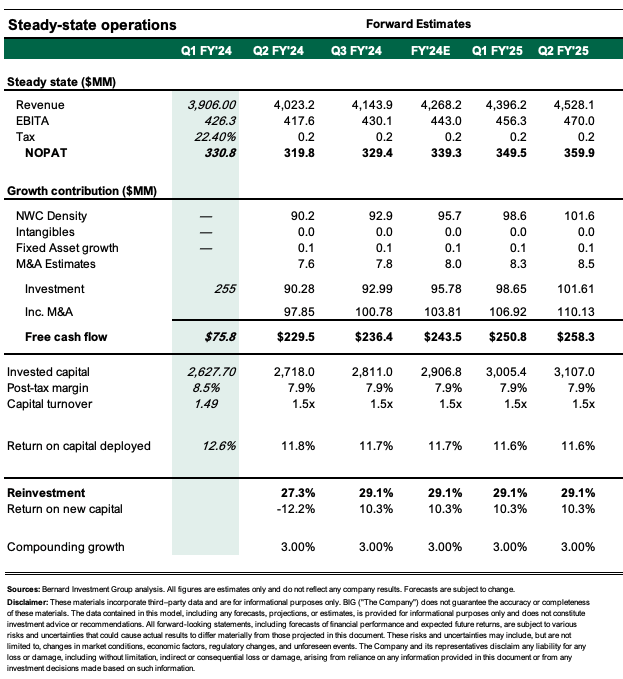

The gross sales ramp has flattened in latest occasions however administration has reinvested ~$650mm again into the enterprise since FY’23 (TTM foundation) and with avg. ROICs of ~12% I can see +$78mm in NOPAT on this per 12 months (~$4.20/share in 5yrs). Critically although, incremental earnings on new investments since FY’21 returned ~18% and administration dedicated ~36% of complete NOPAT produced since FY’21, compounding the intrinsic value of the enterprise by ~6.5% over this time (Determine 4). Beginning multiples in FY’21 had been excessive, nonetheless, so the inventory has returned <1%, with ~6% contraction in multiples balancing the TSR (Determine 5). Basic momentum is sound too – Q2 FY’24 homebuilding revenues had been +12% YoY to $1.1Bn pushed by +10% development in closings. Common gross sales costs (“ASPs”) had been ~+10K YoY to $513.8K – so a wholesome dose of pricing and demand fuelling the top-line. It pulled this to gross of ~19% and earnings of $0.83/share (+18% YoY). Therefore it loved ~1.5x earnings leverage on gross sales (a testomony to its comparatively fastened working prices). My ahead estimates [see: Appendix 1] undertaking ~7% CAGR in gross sales to ~$5.4Bn by FY’26E which is ~$700mm forward of consensus (Determine 6). The place I differ vs. the Road in my opinion is on backlog – DFH left the quarter with backlog ~$2.1Bn fabricated from ~4,200 houses [vs. $2.3Bn / 4,524 homes in Q1] with an avg. ASP of $505,022 within the pipeline. It expects to ship ~1,088 houses from FY’25, leaving 3,177 for completion by the tip of subsequent 12 months. It additionally had ~1,712 new orders in Q2 vs. 1,655 this time final 12 months with ~13% cancellation charge. That is a further $2.5Bn in working capital to come back in over the following 2+yrs and with asset turns of ~1.5x this might produce a further $3.7Bn in gross sales in my opinion.

Determine 4.

Firm filings

Determine 5.

Firm filings, writer

Determine 6.

Creator estimates

Attractively valued with low embedded expectations

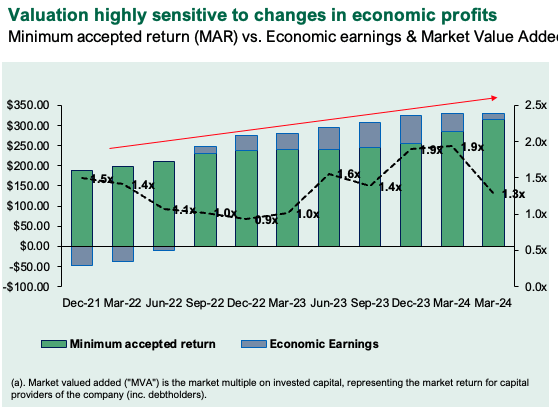

Low embedded expectations with good high quality interprets to excessive margin of security to me. The bar will not be set to excessive, however given the standard issue, there’s a beneficial distribution of outcomes. Critically, DFH’s market values are extremely delicate to financial income it produces above a set hurdle charge (we make use of 12% right here to symbolize the chance value of the market benchmarks). The enterprise is priced ~1.3x EV/IC as I write which is in-line with historic vary. These are 1) low expectations, as talked about, and a pair of) present scope to commerce larger with upside surprises. My view is the change for a draw back shock a low chance occasion, such that it could drive the valuation <1x EV/IC.

Determine 7.

Firm filings, writer

Valuation insights

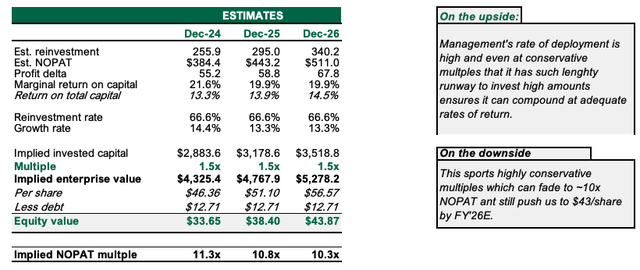

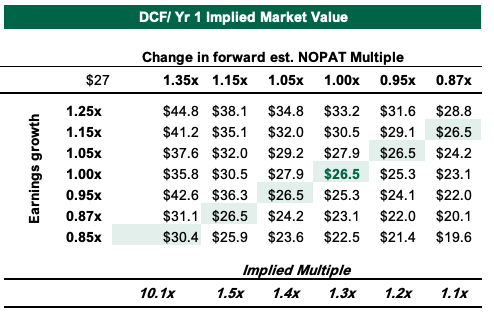

My funding thesis is extremely predicated on the actual fact administration has an intensive funding runway to deploy funds over within the subsequent 5 years. I see it doing this at pretty advantageous charges of return, offering the funds to repeat the method at scale. This doesn’t require excessive multiples of capital to see the valuation compound. As an alternative, it’s a perform of the sums administration can make investments. As an illustration, investing $1 at 1.3x = $1.30 available in the market. Nonetheless, an funding of $2 is valued at $2.60 available in the market underneath these assumptions. Therefore, on the upside 1) administration’s charge of deployment is excessive and a pair of) even at conservative multiples, it has such prolonged runway to take a position proportionally excessive quantities, this 3) ensures it might compound its intrinsic enterprise valuation at sufficient charges of return. Furthermore, as I’ve talked about a number of occasions, the investments are comparatively “un-sexy”, however are predictable and have a transparent goal – to roll out inexpensive single-family houses rapidly. These easy economics appeal to the easy funding cortex as mine is. On the draw back, this sports activities extremely conservative multiples which may fade to ~10x NOPAT ant nonetheless push us to $43/share by FY’26E. I’m trying to ~13-14% earnings development charge to FY’26E which permits for ~5% contraction on this to 1.2x EV/IC (Determine 9).

Determine 8.

Creator

Determine 9.

Creator’s estimates

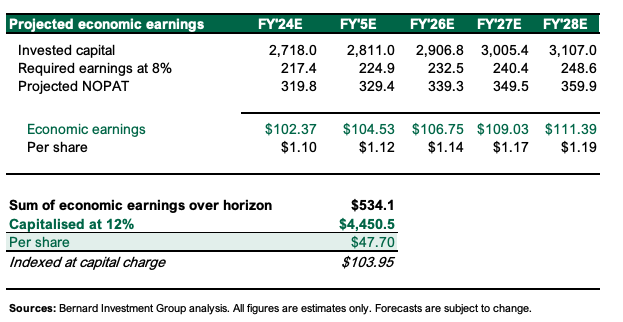

Lastly, the discounted worth of freely obtainable money {that a} personal proprietor of DFH may strip out of the enterprise quantities to ~$47 per share underneath the assumptions proven in Appendix 1. Critically, that is money circulate produced above an 8% threshold charge and discounted at our 12% hurdle charge to set a tremendously excessive ‘ranked’ valuation for the enterprise above different investments with comparable danger on the market. That is ~77% implied upside by FY’28 or ~21% CAGR over this time, supporting a purchase. On the draw back, operating extra conservative assumptions on gross sales (1.5% vs. 3%) and on NWC (30% funding vs. 77%) yields >35/share.

Determine 10.

Creator estimates

Dangers to thesis

Draw back dangers to the thesis embrace 1) administration not changing on the backlog at sufficient tempo or at <ASPs (<$495K places a dent in my modelling), 2) <1% gross sales development with <25% NWC reinvestment as this means truthful worth at present, 3) the inflation/charges axis continues to be a problem, and 4) the broader set of macro and market dangers which might be plaguing equities at this cut-off date.

These dangers have to be thought of in full earlier than continuing any additional.

Briefly

DFH is a purchase in my opinion on account of 1) basic momentum in +300bps ROICs vs. FY’21 and ~200bps post-tax margin because the identical, 2) low embedded expectations at ~1.3x EV/IC and 10x NOPAT, and three) a high-quality enterprise franchise that has an intensive reinvestment runway to redeploy funds again into its enterprise to develop the earnings produced on capital employed. My view is the enterprise is value ~$32/share at present with compounding means to ~$43-$47/share by FY’26E. Fee purchase.

Appendix 1.

Creator estimates

[ad_2]

Source link