[ad_1]

Zuberka

Introduction

Because it has been some time since I mentioned Eagle Level Credit score (NYSE:ECC) and its perpetual most well-liked shares, I wished to regulate the corporate’s capability to proceed to cowl the popular dividend funds. The yield on the popular shares has elevated to eight.7% and I nonetheless assume this provides a very good danger/reward ratio.

The earnings reported by ECC stay robust

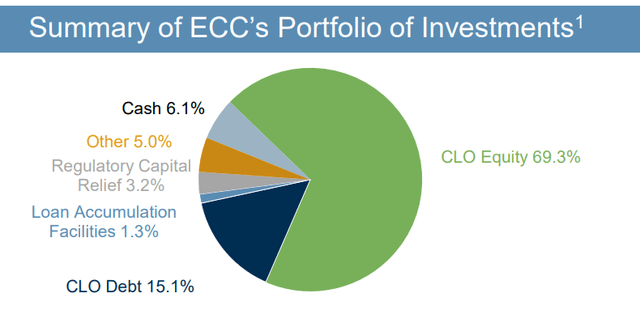

In Eagle Level Credit score’s case, the vast majority of the portfolio consists of CLO Fairness. These investments are on the backside of the CLO meals chain and solely acquired the ‘leftovers’ by way of revenue. Solely in any case funds on the CLO Debt securities have been coated, the CLO Fairness will obtain a payout. In fact these increased danger securities include a better reward because the CLO Fairness investments are inclined to have a return of round and even over 20% nowadays.

ECC Investor Relations

Given the upper danger ingredient in CLO Fairness versus CLO debt, it’s essential to maintain observe of the default charge of the CLO issuers, as it is rather unlikely CLO Fairness will get better something within the occasion of a default. However because the 12-month trailing default charge was simply 0.92% on the finish of June (a lower from the year-end 2023 default charge), and that in fact is a really manageable share that might simply be absorbed by the incoming money flows from the performing securities.

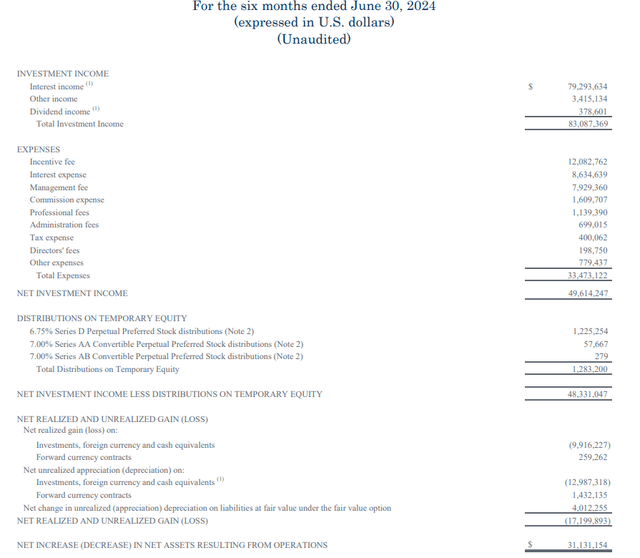

As proven under, Eagle Level Credit score generated a complete funding revenue of $83.1M within the first half of this 12 months. In the meantime, the overall bills got here in at $33.5M (and this contains the curiosity funds in addition to the dividend funds on the time period most well-liked inventory) leading to a web funding revenue of $49.6M.

ECC Investor Relations

As proven above, the $1.22M in most well-liked dividend funds on the Sequence D most well-liked inventory, leading to a web funding revenue of $48.3M after the distributions.

The revenue assertion above tells us two issues. To begin with, the payout ratio of the Sequence D most well-liked dividends versus the online funding revenue is lower than 3%. That’s nice. Secondly, it additionally exhibits that the corporate may cowl virtually $100M per 12 months in defaults earlier than reporting a web loss. So whereas CLO Fairness is riskier than CLO debt, in ECC’s case the upper CLO revenue is greater than enough to cowl the influence of the potential defaults.

The revenue assertion additionally exhibits there was a realized lack of $9.9M on investments, which signifies that the online funding revenue minus realized losses was roughly $38.4M. Divided over 97.8M shares, this ends in a results of roughly $0.39/share. I’m not together with unrealized losses right here, as these losses both A) do materialize and find yourself within the class of realized losses or B) don’t materialize, and the market value trades nearer to par worth nearer to the maturity date of the securities. So primarily based on the present outcomes and default charge, the popular dividends are very properly coated.

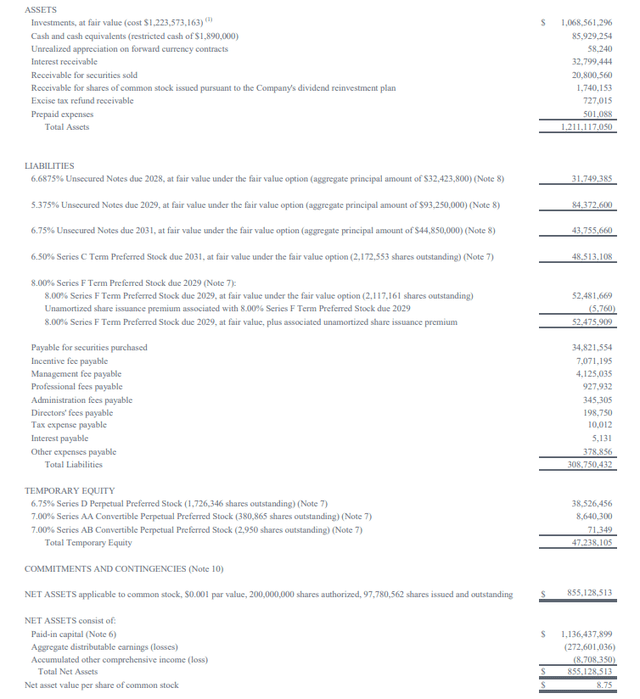

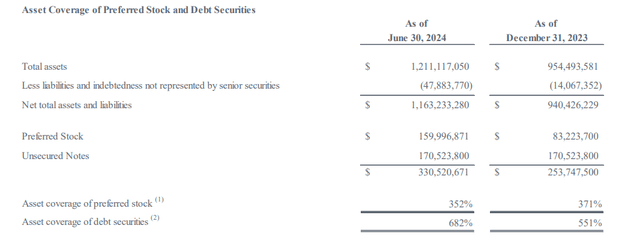

The asset protection ratio stays wonderful as properly. As you’ll be able to see under, there are 1.73M most well-liked shares excellent (excluding the time period most well-liked shares that are included within the liabilities phase and aren’t counted as fairness), leading to most well-liked fairness of $47M to which the $855M in widespread fairness ranks junior.

ECC Investor Relations

And due to the strong stability sheet, the corporate additionally handsomely meets the minimal 200% most well-liked inventory asset protection ratio, with a complete protection ratio of 352% as of the top of June.

ECC Investor Relations

So from each the dividend protection perspective and the asset protection ratio perspective, I’m not nervous about ECC’s fee commitments.

Including length to my portfolio utilizing the perpetual most well-liked shares

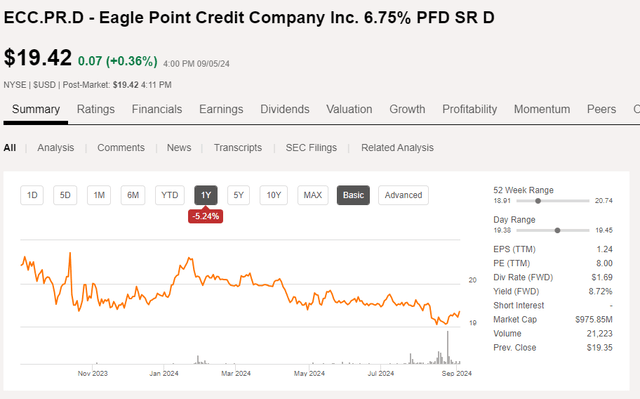

Whereas Eagle Level Credit score has a number of problems with time period most well-liked shares and child bonds excellent, I turned more and more intrigued by the perpetual most well-liked shares, buying and selling with (NYSE:ECC.PR.D) as ticker image. The Sequence D most well-liked shares are presently buying and selling at $19.42 (proven under) which suggests the present yield is roughly 8.7%. As these are perpetual most well-liked shares and not using a agency maturity date, it’s fairly ineffective to calculate a yield to name (which might be the higher metric to make use of for the time period most well-liked shares). As 6.75% is a fairly low price of capital for Eagle Level Credit score, I’m not relying on these most well-liked shares being retired anytime quickly.

In search of Alpha

These most well-liked shares pay an annual distribution of $1.6875 per share, payable in month-to-month tranches of simply over $0.14 per 30 days.

Funding thesis

I presently have a small lengthy place in ECC’s most well-liked shares Sequence D as I like the danger/reward ratio and because the perpetual nature of those most well-liked securities provides length to my portfolio. I’ll add a number of the different most well-liked or debt securities to my portfolio. In the meantime, the widespread shares seem fairly fascinating in addition to the present quarterly distribution of $0.48/share (paid month-to-month) is decently coated whereas the yield on the widespread shares is roughly 19%. However whereas the distribution charge on the widespread models is interesting, let’s not overlook the inventory is buying and selling at a premium of just about 15% to its NAV however Eagle Level continues to promote widespread inventory on the open market on the similar premium.

[ad_2]

Source link