[ad_1]

Evgeny Gromov

Whereas most valuable metals names reported margin growth in Q1 2024 on the again of stronger metals costs, Endeavour Silver Corp. (NYSE:EXK) was an exception, battling a stronger Peso and lapping tough comps at its Guanacevi Mine from a grade standpoint. The outcome was that AISC margins sunk to beneath 10% in Q1 2024 and the corporate generated restricted money move regardless of the stronger gold worth. On a constructive word, Q2 is shaping as much as be a significantly better quarter, benefiting from an additional enhance from gold by-product credit and a a lot stronger silver worth. As well as, its Terronera Venture is nearing the end line, a transformative asset that can assist to enhance EXK’s company-wide margin profile.

On this replace we’ll dig into the latest outcomes, the Q2 outlook, and whether or not EXK nonetheless affords worth at present ranges.

Endeavour Silver Q1 Manufacturing & Gross sales

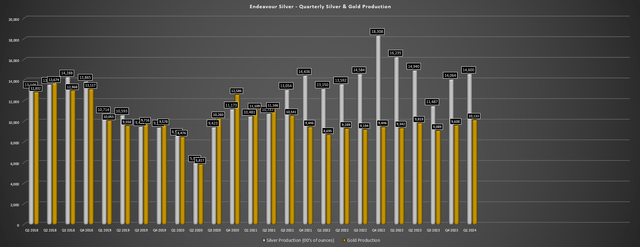

Endeavour Silver launched its Q1 manufacturing outcomes, reporting quarterly manufacturing of ~1.46 million ounces of silver and ~10,100 ounces of gold. This represented a ten% decline in silver manufacturing year-over-year, offset by a 9% improve in gold manufacturing. The decrease silver manufacturing was attributed to considerably decrease grades at Guanacevi (402 G/T of silver vs. 511 G/T of silver), in addition to decrease grades at Bolanitos (42 G/T silver vs. 61 G/T of silver). Fortuitously, greater gold grades at Bolanitos greater than offset the decrease silver grades, which, mixed with greater gold costs, resulted in a significantly better quarter from this smaller asset.

Endeavour Silver Quarterly Gold/Silver Manufacturing – Firm Filings, Writer’s Chart

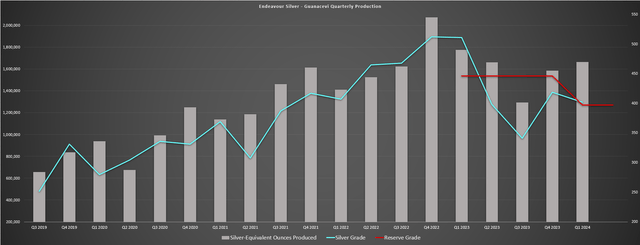

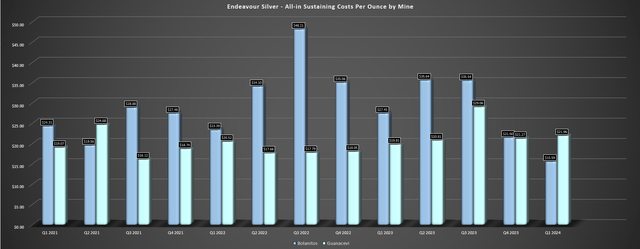

Digging into the outcomes somewhat nearer, Guanacevi produced ~1.34 million ounces of silver and ~4,100 ounces of gold, down from ~1.42 million ounces and ~4,200 ounces, respectively. Larger mill throughput of ~115,000 tonnes and better recoveries had been greater than offset by the 21% decrease silver grades. Endeavour famous that the decrease grades had been per the mine plan and the sharp dip and manufacturing declines at Guanacevi should not be shocking provided that the corporate was mining properly above reserve grades in 2022 by means of early 2023 (proven beneath). Based mostly on decrease manufacturing, a stronger Peso, and continued inflationary pressures, AISC spiked to $21.96/oz, a 14% improve year-over-year.

Guanacevi Mine Quarterly Manufacturing – Firm Filings, Writer’s Chart

Fortuitously, whereas Guanacevi had a softer Q1 with greater manufacturing at decrease margins, Bolanitos had a greater quarter from a margin standpoint. This was regardless of decrease year-over-year manufacturing of ~124,300 ounces of silver (Q1 2023: ~183,600 ounces), offset by 17% greater gold manufacturing. The results of the upper gold by-product credit (elevated gold ounces offered at greater costs) led to mine web site AISC declining to $15.59/ozvs. $27.45/ozwithin the year-ago interval, a 43% decline. The excellent news is that this tailwind for prices ought to proceed into Q2 with the gold worth anticipated to be up 12% sequentially (Q2 vs. Q1) to ~$2,330/ozor higher.

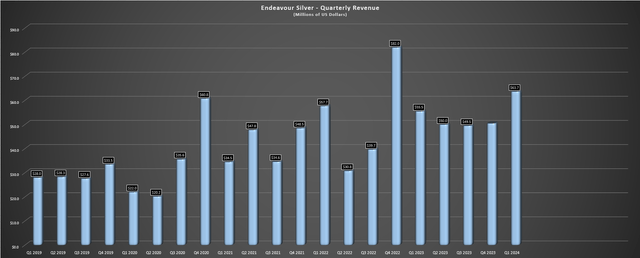

Endeavour Silver Quarterly Income – Firm Filings, Writer’s Chart

As for the corporate’s monetary outcomes, Endeavour reported income of $63.7 million (+15% year-over-year), $4.6 million in working money move (Q1 2023: [-] $0.4 million), and a free money outflow of $40.3 million (Q1 2023: free money outflow of $21.1 million). This was associated to greater spending at Terronera which noticed capex almost double year-over-year to $40.3 million. As for Endeavour’s stability sheet, the corporate ended the quarter with money & money equivalents of $34.9 million and ~$28 million in internet money. Nevertheless, this was largely associated to vital share gross sales, evidenced by ~23.1 million shares being offered underneath its ATM in Q1 alone at US$1.72, leading to ~11% share dilution at multi-year lows, a painful stage of dilution for a longtime and producing firm.

Prices & Margins

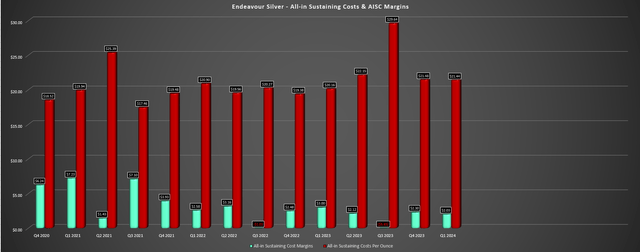

Taking a look at prices and margins, Endeavour’s Q1 AISC of $21.44/oz, up 6% year-over-year, however beneath funds due to the good thing about greater gold by-product credit and decrease sustaining capital spend ($7.0 million vs. $8.0 million). Endeavour referred to as out greater energy, labor, and consumables prices being headwinds from a value standpoint, and the stronger Mexican Peso definitely did not assist. Given the restricted improve within the silver worth year-over-year ($23.47/ozvs. $23.16/oz), AISC margins sunk to $2.03/ozvs. $3.00/ozwithin the year-ago interval. And whereas its higher-cost present operations shall be diluted by lower-cost Terronera ounces, the sticky inflationary pressures counsel Terronera working value estimates are too low, with a extra sensible AISC of ~$12.00/ozon silver-equivalent ounces vs. the $9.84/ozreported within the 2023 FS replace.

Endeavour Silver – Quarterly Prices by Mine – Firm FIlings, Writer’s Chart Endeavour Silver AISC & AISC Margins – Firm Filings, Writer’s Chart

Whereas these are nonetheless very strong margins at Terronera and can assist to drag down Endeavour Silver’s prices materially beginning in H2 2025, it’s a downgrade from my earlier outlook. So, whereas Terronera is undoubtedly an improve for the funding thesis, it is not as vital as I initially anticipated given the associated fee creep throughout all operations. Endeavour Silver had the next to say on its Q1 2024 Convention Name:

“We have not offered steering from an operational standpoint for Terronera since April 2023 after we introduced the development resolution. And at the moment, we put out an optimized plan and highlighted an ~$81 value/tonne. And that value per tonne had come down from the FS of ~$87 to ~$81 due to the economies of scale. That estimate was performed successfully in December of 2022, and January of 2023.

Because the begin of 2023, throughout the trade and particularly in Mexico, you’ve got had the appreciation of the Mexican Peso by 15%. You’ve got had inflationary pressures, particularly on metal, reagent, and energy prices, all in Mexico. So it could be particularly reasonable to imagine that you’ve got had escalations from an working standpoint at Terronera going from $81 possibly you get into the $95 or $100 vary. As we go into manufacturing, hopefully later this 12 months, like I say, commissioning for This autumn, administration will replace these prices.”

– Endeavour Silver Q1 2024 Convention Name

So, what’s the excellent news?

Whereas Endeavour Silver reported razor-thin margins in Q1 2024, the corporate ought to see vital margin growth within the upcoming quarter with the silver worth averaging over $28.50/ozquarter-to-date and the gold worth averaging above $23.00/oz. Not solely will this give it a lift from a by-product credit score standpoint at Bolanitos to drag AISC down farther from Q1 2024 ranges, however the firm will take pleasure in a better promoting worth within the upcoming quarter as properly. Therefore, it would not shock me to see Endeavour Silver report AISC margins of $6.00/ozor higher in Q2 2024 (Q2 2023: $2.12/oz), and we must always see a really robust Q3 as properly with the Mexican Peso trying to have lastly topped out vs. the US Greenback (UUP).

Latest Developments

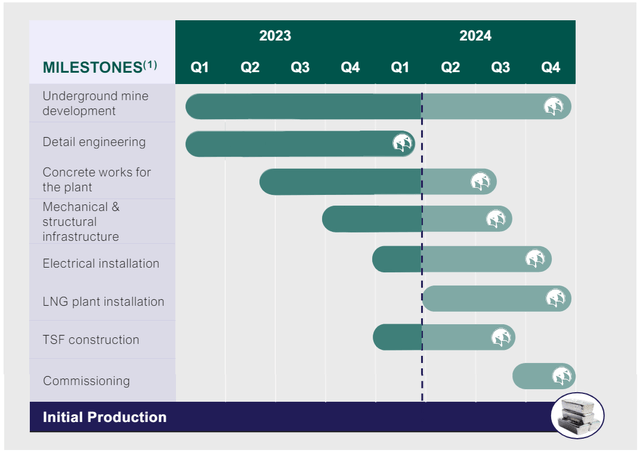

Transferring to latest developments, Terronera has handed the midway mark for development and stays on observe for its first manufacturing by year-end 2024. Because the begin of development, the corporate has spent ~$158 million or ~58% of its up to date capital estimate of ~$271 million, with a extra conservative determine being $280 million to bake in any minor value overruns vs. the earlier estimate. This leaves ~$120 million left to spend on development with this accessible to Endeavour from ongoing money move from operations, its undrawn $120 million debt facility ($60 million drawn in April after the tip of Q1), and its present money place. Therefore, whereas we’ve got seen huge will increase to the Terronera capex invoice from ~$175 million beforehand in 2021, the mission does look absolutely funded.

Terronera Venture Building – Endeavour Silver

As for the latest progress replace, Endeavour famous that 83% or ~$225 million had been dedicated, and over 3,200 meters of underground improvement had been accomplished. As for floor actions, floor mill and infrastructure development was 56% full whereas concrete work and structural metal erection stood at 83% and 80% full, respectively. Throughout Q2, Endeavour will mine the primary improvement ore primarily based on the present schedule, with long-hole mining anticipated in Q3 adopted by reduce and fill mining to arrange an ore stockpile for ramp-up. Total, issues seem like progressing fairly easily which is constructive to see, and the present timeline suggests we might see roughly three full quarters at full manufacturing ranges in 2025 for Terronera, assuming industrial manufacturing is reached by late March/early April.

Terronera Building Timeline – Firm Web site

So, what are the advantages of Terronera?

As outlined in previous updates, this mission is able to producing ~7.0 million silver-equivalent ounces every year at a lot decrease prices (~$12.00/ozAISC?) which can assist to enhance Endeavour’s margins. That is necessary as a result of the corporate at present has razor-thin margins however Terronera will morph it into an average-cost producer vs. one of many highest-cost producers sector-wide. Total, this is able to have helped with a big re-rating within the inventory, however with EXK already up over ~160% off its lows in the identical interval that we noticed over 20% share dilution (successfully a 200% improve in its market cap), I am undecided how a lot room is left for a re-rating right here near-term.

Valuation

Based mostly on ~248 million absolutely diluted shares and a share worth of US$3.60, Endeavour Silver trades at a market cap of ~$890 million and an enterprise worth of ~$920 million when factoring in debt just lately drawn on its debt facility. This leaves Endeavour Silver buying and selling at over P/NAV (6.5% low cost price), properly above the 0.80x P/NAV a number of that the inventory traded at close to its lows the place it turned very moderately priced earlier this 12 months. In the meantime, Endeavour Silver now trades at ~10x FY2025 EV/FCF estimates which isn’t an unreasonable valuation for a reputation with silver publicity, however I see it as almost absolutely valued for a corporation with all of its operations in a Tier-2 ranked jurisdiction, Mexico and a reputation with a poor observe file of per share development (*).

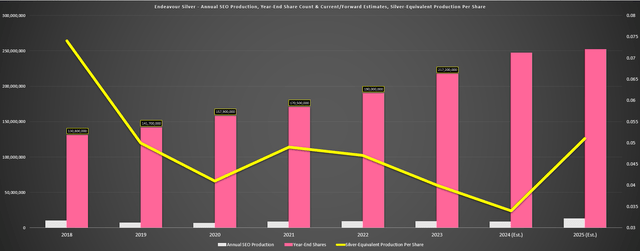

(*) Because the chart beneath highlights, whereas Terronera is a transformational asset that pushes up annual search engine optimisation manufacturing, the advantages to shareholders are largely muted provided that complete shares have elevated almost 80% since 2019 (~142 million shares —> ~250 million shares). So, whereas Endeavour’s prime and backside line profit from Terronera, there may be restricted enchancment from a per share foundation, with annual search engine optimisation manufacturing per share anticipated to be roughly flat in 2025 vs. 2019 ranges (*)

Endeavour Silver Annual search engine optimisation Manufacturing, 12 months-Finish Share Rely + Ahead Estimates & search engine optimisation Manufacturing Per Share – Firm Filings, Writer’s Chart & Estimates

To place this valuation in perspective, B2Gold Corp. (BTG) is at present paying a 6.3% dividend yield, has an exceptional observe file of per share development, and trades at simply ~7x FY2025 EV/FCF with a extra diversified portfolio and far greater margins. In the meantime, Lundin Gold Inc. (OTCQX:LUGDF) additionally operates in a Tier-2 jurisdiction however with a far stronger asset (Fruta del Norte) and a really spectacular observe file of per share development as properly. It trades at ~6x FY2025 EV/FCF estimates or almost half the a number of of Endeavour Silver. So, adjusted for general high quality (observe file, common asset high quality, margins), I proceed to see way more enticing bets elsewhere within the sector.

So, what’s a good worth for the inventory at the moment?

Utilizing what I consider to be honest multiples of 8x working money move estimates and 1.2x P/NAV and a 65/35 weighting to P/NAV vs. P/CF, I see a good worth for Endeavour Silver of US$3.40. This factors to the inventory being absolutely valued at present ranges which is unlucky as a result of the inventory’s honest worth would have been nearer to US$4.00 if not for the ~20% share dilution incurred in the latest quarter alone (and certain extra ATM gross sales in Q2 2024). To summarize, I see no margin of security at present ranges and consider that any upside in Endeavour would require greater silver costs which isn’t a sexy funding thesis. As an alternative, I favor to mannequin conservative metals worth assumptions, and discover what names are undervalued even utilizing base case assumptions, and take the upside in commodities as a bonus.

In Endeavour’s Silver case, I consider one must mannequin a minimal of $30.00/ozsilver to justify the present valuation.

Abstract

Endeavour Silver had an honest Q1 operationally and noticed a significant profit from the gold worth power at Bolanitos which helped to cut back its mine-site AISC. Sadly, AISC margins nonetheless fell year-over-year, however we are going to see vital margin enchancment in Q2 2024 with AISC margins more likely to climb upwards of $6.00/oz. That mentioned, the improved margin outlook is overshadowed by what seems to be as much as 25% share dilution this 12 months (over 21% year-to-date) to convey its new lower-cost asset in manufacturing. So, whereas a rising silver worth will carry all boats, and Endeavour is undoubtedly a greater firm with Terronera, I proceed to see way more enticing bets elsewhere within the sector at the moment.

If I had been trying to put new capital to work at the moment in what I consider to be essentially the most undervalued names, Vox Royalty Corp. (VOXR) stands out as essentially the most enticing. Not solely does the enterprise commerce at lower than 0.70x P/NAV regardless of a superior enterprise mannequin and 85% margins, nevertheless it has the next enticing attributes:

1. The 2nd largest hard-rock royalty portfolio in Western Australia and a portfolio centered round Tier-1 ranked jurisdiction property (Australia, Nevada, Ontario, Quebec).

2. A robust stability sheet with over $10 million in internet money and no debt, and a rising 2.1% dividend yield.

3. A aggressive benefit vs. its royalty friends with an unimaginable observe file of persistently shopping for a greenback in worth for $0.30 or much less with a sub 3-year payback on royalty offers to this point.

Therefore, whereas EXK would possibly develop into attention-grabbing if it dipped again beneath US$2.50, I believe VOXR is the way more enticing alternative and buying and selling at an enormous low cost to honest worth with as much as 100% upside potential if it had been to re-rate consistent with its friends, with far larger upside longer-term because it broadens out its portfolio.

[ad_2]

Source link