[ad_1]

Sundry Pictures

Amid more difficult macro straits this yr, many corporations have adopted a tried and true playbook to drive income progress: rising pricing by a wide range of means. For Eventbrite (NYSE:EB), the web ticketing firm that competes with the likes of StubHub and Ticketmaster, this meant introducing new creator charges, whereby occasion organizers now need to pay Eventbrite a payment for internet hosting an occasion and accessing its viewers attain.

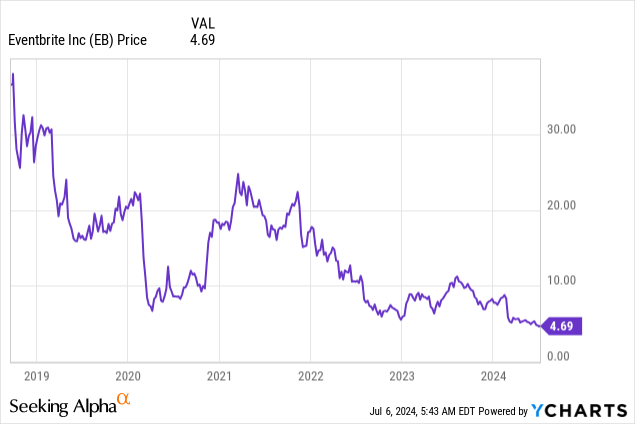

The change has produced a really predictable impact: internet income per ticket has soared as a result of new charges, however extra creators have dropped out and paid ticket volumes have continued to say no. Thus far, Wall Avenue has little or no confidence in Eventbrite’s trajectory wanting forward, because the inventory is down greater than 40% yr to this point.

Compelling valuation, however dangers from pricing strikes nonetheless stay

I final wrote a impartial opinion on Eventbrite in April, when the inventory was nonetheless buying and selling within the low $5 vary. Since then, we have been capable of see the preliminary impacts of the corporate’s payment construction change on Q1 outcomes.

Eventbrite is plowing forward with the change, noting as properly that it continues on increasing its variety of occasions that it covers. It just lately commissioned a examine, “Area of interest to Meet You,” on youthful generations’ fatigue over on-line relationship and the rise of offline relationship occasions, like speed-dating rounds. The corporate is making an attempt to usher in extra of these kind of occasions and creators to offset potential churn from its current pricing choices.

I stay impartial on this inventory. We have now seen constructive advantages from these value will increase in Eventbrite’s Q1 outcomes: income progress exceeded expectations, and its adjusted EBITDA margins soared to new heights. We word now that one of many largest attracts to Eventbrite is that we are able to correctly worth the inventory from an EBITDA foundation.

At present share costs underneath $5, Eventbrite trades at a market cap of $455.5 million. After we internet off the $693.6 million of money and $358.2 million of debt on the corporate’s most up-to-date steadiness sheet, the corporate’s ensuing enterprise worth is simply $120.1 million. That is one other large draw for Eventbrite: the vast majority of its market money is just sitting in its internet money place.

In the meantime, for the present fiscal yr FY24, the corporate is anticipating to generate income of $360-$371 million, which represents 10-14% y/y progress, and a “low to mid teenagers” adjusted EBITDA margin on that income profile.

Eventbrite outlook (Eventbrite Q1 shareholder letter)

If we conservatively assume a 12% adjusted EBITDA margin (in keeping with Q1 margins) on the midpoint of the corporate’s income vary, adjusted EBITDA for the yr could be $43.9 million (+53% y/y). This places Eventbrite’s valuation at simply 2.7x EV/FY24 adjusted EBITDA.

The inventory is affordable: however that is as a result of its path ahead is laden with dangers, together with:

Churn impacts from payment choices. Eventbrite’s determination to begin charging occasion organizer charges, arguing that creators ought to pay for entry to Eventbrite’s viewers attain, is at the moment driving double-digit income progress. However we have already seen paid creator counts decline, and over the long term, it might steer extra creators away from Eventbrite and towards competing platforms. Quantity decline. To that extent, paid ticket volumes are additionally declining – a mirrored image of fewer occasions, fewer creators, and finally fewer consumers on the Eventbrite platform. Quite a few rivals. We are able to’t neglect as properly that Eventbrite is certainly one of numerous on-line ticketing platforms, together with evite, Ticketmaster, Meetup, and different names.

All in all, although I am trying to rotate extra of my portfolio towards deep-value names amid a really costly inventory market, I proceed to want sitting on the sidelines for Eventbrite. In my opinion, there are too many unknowns surrounding paid ticket declines to make a long-term guess right here.

Q1 obtain

Let’s now undergo Eventbrite’s newest quarterly leads to better element. The Q1 earnings abstract is proven beneath:

Eventbrite Q1 outcomes (Eventbrite Q1 shareholder letter)

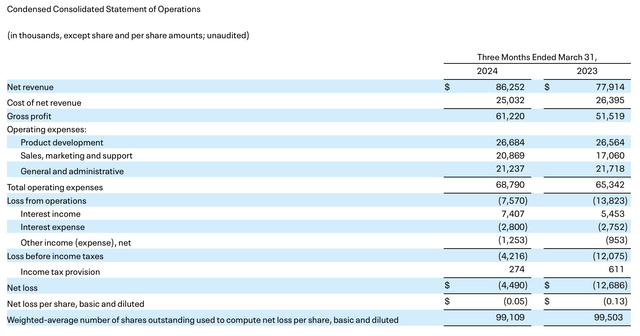

Eventbrite’s income grew 11% y/y to $86.3 million, barely beating Wall Avenue’s expectations of $85.3 million (+9% y/y). We do word, nevertheless, that income progress decelerated sharply from 22% y/y progress in This autumn. We additionally word that Eventbrite’s full-year steering, which requires a 10-14% y/y progress vary, implies that to hit the midpoint, Eventbrite’s efficiency must sequentially speed up and enhance as we transfer all year long.

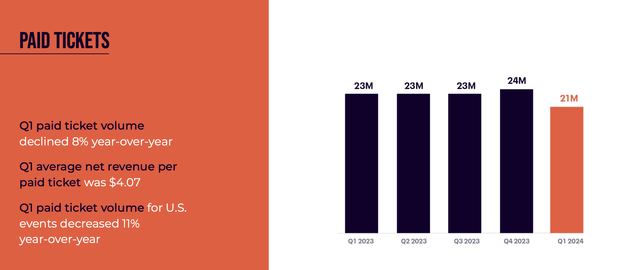

As anticipated, paid ticket volumes declined -8% y/y to 21 million tickets: a deeper decline than -4% in This autumn. The corporate offset this with a internet income per ticket of $4.07, which was up 21% y/y.

Eventbrite paid ticket traits (Eventbrite Q1 shareholder letter)

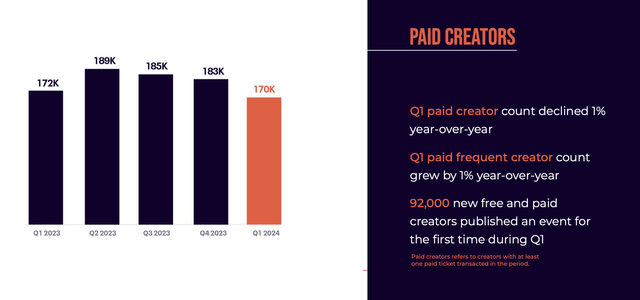

Maybe extra worrisome than the decline in paid tickets, nevertheless, was the sharp drop-off in paid creators: which has already been a pattern over the previous few quarters. Eventbrite’s depend of paid creators declined 13k sequentially to 170k, the third straight quarter of decline.

Eventbrite paid creator traits (Eventbrite Q1 shareholder letter)

The corporate nonetheless argues that it is constructing a long-term basis for creator funding and success. Administration says that extra creators are opting to enroll in month-to-month subscriptions relatively than pay per occasion, which means that these creators could also be higher-volume, higher-frequency clients for Eventbrite. Per CEO Julie Hartz’s remarks on the Q1 earnings name:

Second, on pricing and packaging. Creators have adopted the month-to-month subscription plan at a sooner price than pay per occasion pricing, which mixed with their direct suggestions has given us a robust sign on how we are able to simplify the selection set and lean extra into the subscription pathway by providing free trialing, annual reductions and promotional advantages for issues like Eventbrite Advertisements. In response to those adjustments and clear communication across the plans, subscribing creators elevated by 40% throughout the primary quarter […]

Along with these transitions, we’re specializing in creator satisfaction and listening fastidiously to their suggestions. As an illustration, we launched prompt payouts and faucet to pay in Q1 to offer creators sooner entry to their cash and better comfort to assist on the door ticket gross sales. We additionally delivered a brand new creator dashboard that gives the reporting readability they need. Creators have additionally requested for better assist and skilled steering and we responded by increasing buyer assist and account administration.

These motion plans are the first levers that place us to reaccelerate paid ticket quantity, as we transfer via 2024. However we’ve not taken our eye off the longer-term technique of how we construct our market at scale. Our creators inform us their prime want is to attach with their group and convert that group right into a rising variety of occasion goers.”

As we transfer into Eventbrite’s Q2 earnings launch (anticipated in early August) and past, it’s going to be key to see that paid ticket volumes and creator counts do not meaningfully deteriorate farther from right here.

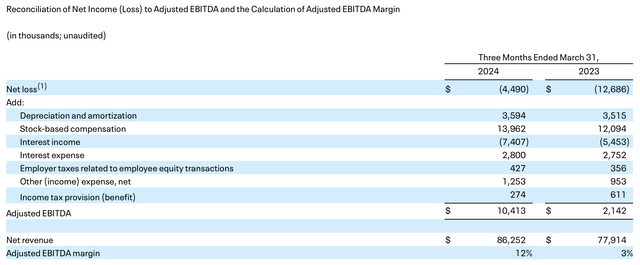

From a profitability perspective, it is no shock that Eventbrite’s pricing strikes have produced a considerable enhance to adjusted EBITDA, which grew almost 5x y/y within the quarter to $10.4 million, representing a 12% adjusted EBITDA margin: 9 factors greater than 3% within the year-ago quarter.

Eventbrite adjusted EBITDA margins (Eventbrite Q1 shareholder letter)

Key takeaways

I want Eventbrite was a slam-dunk worth play that I used to be assured on, as a result of a ~3x adjusted EBITDA a number of is nearly unattainable to seek out in at this time’s market: however sadly that low-cost valuation comes with a plethora of dangers as Eventbrite undergoes a serious enterprise mannequin change and has continued to shed creator counts and paid ticket volumes. I proceed to want watching this inventory from the sidelines and ready on additional readability earlier than diving in.

[ad_2]

Source link