[ad_1]

Anthony Bradshaw

Pricey readers/followers,

On this article, I’ll replace my thesis on the one gold “play” I take into account to be related to spend money on – although not essentially at this valuation. You could recall if you happen to observe my work that I’m not a really lively investor within the gold or valuable metals sector in any respect. In reality, as of this specific time, I shouldn’t have any lively investments that match this standards.

Nevertheless, that doesn’t imply I’m inherently disinterested in such corporations. It’s all concerning the valuation that we now have going for these corporations. For those who recall my final article on the enterprise which you could find right here, you then’ll keep in mind that I thought of the valuation extremely excessive as of the final time I reviewed, and gave the corporate a conservative “Maintain” score. I didn’t make investments and didn’t take into account it a superb time to spend money on the corporate on the time both.

Since that point, my thesis has outperformed, that means that the corporate has really gone down almost 20%, along with the 4-5% it went down after my first impartial thesis. My stance that the corporate is just too costly has thus been the “proper” transfer general.

It is a play on gold mining and the possession of gold royalty streams, in addition to another sorts of valuable metals. As such, it has some correlation to gold pricing however as a result of dividends and the truth that you personal a enterprise relatively than a bodily asset which “solely” will increase or decreases in worth with out supplying you with any curiosity I take into account this a superior kind of funding.

Let’s see what we are able to count on out of this firm going ahead. It’s been a very long time since my final article, however you could find that one right here – and you’ll see that it has carried out according to my expectations.

What we are able to count on out of Franco-Nevada going into 2Q24 and for the rest of the 12 months.

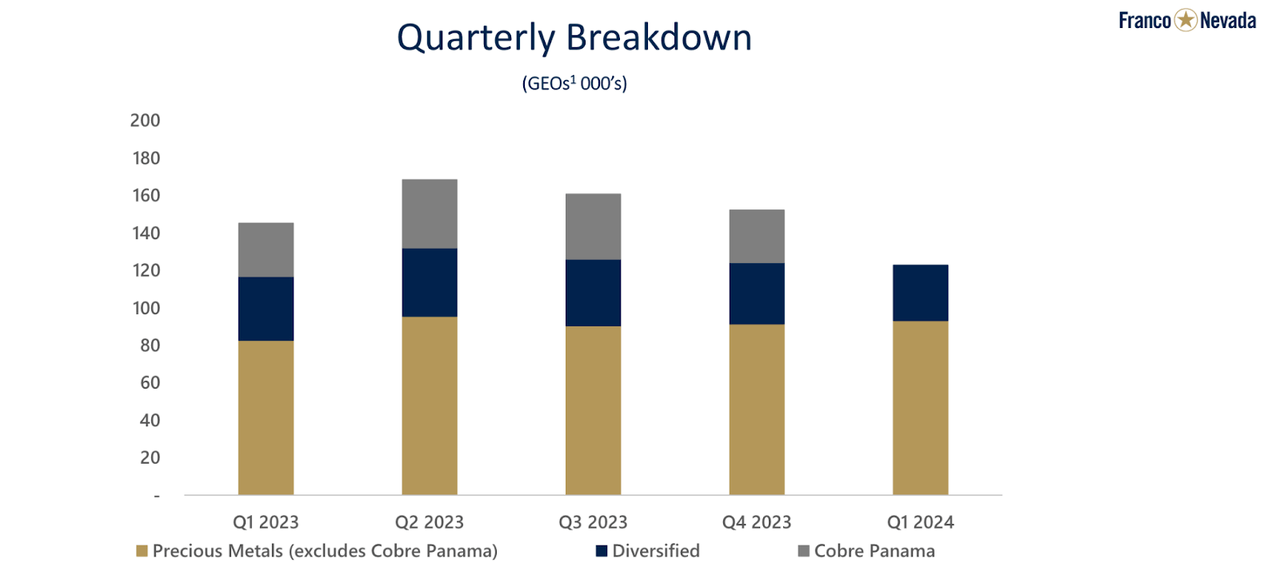

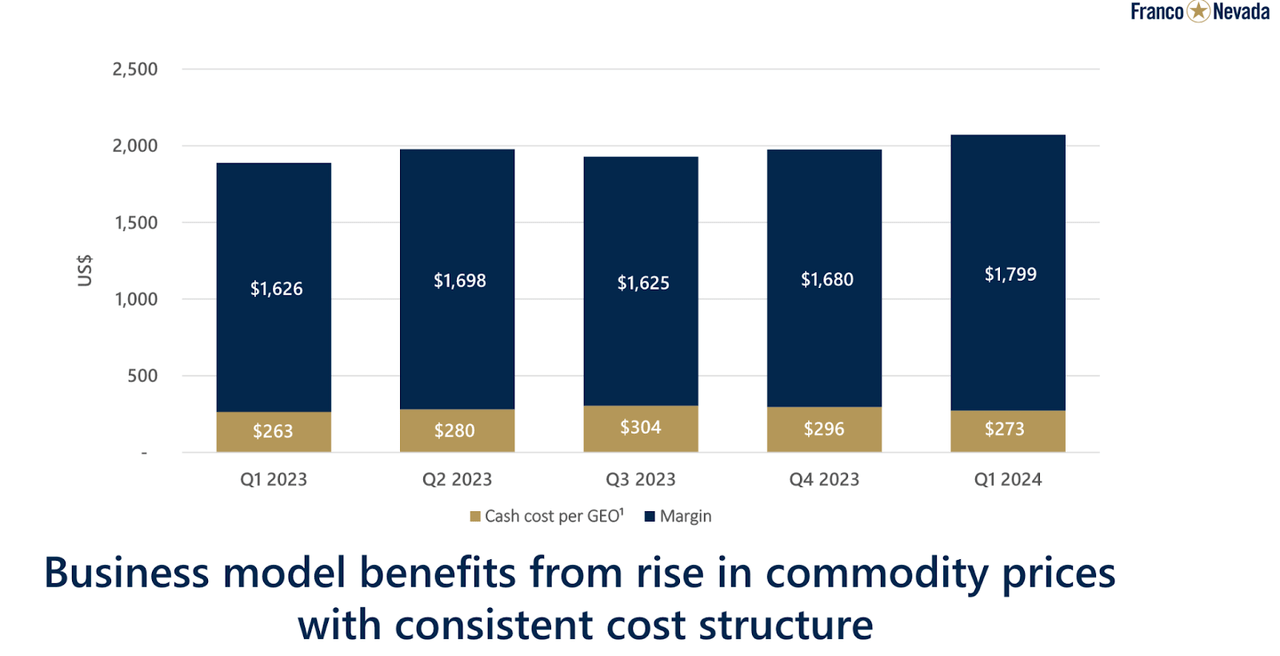

First issues first. The corporate nonetheless is nowhere close to my conservative share worth goal for the enterprise, and which means we ought to be comparatively cautious right here – at the least if we care something about valuation. The actual fact is that ends in 1Q had been relatively poor and continued the pattern of the decline for the corporate. Whereas gold costs proceed to go up, revenues and EBITDA proceed to say no. From highs of $276 in 2Q of 2023, we’re now right down to lower than $217 for the 1Q interval. Good margins, for certain – 84.2% – however outcomes on the entire weren’t that nice.

This has to do with the truth that the corporate isn’t pulling as a lot gold, with gold equal ounces, or GEOs, down 15%, which ends up in a 7.1% income decline and a 5.8% EBITDA decline on an adjusted foundation.

FNV IR (FNV IR)

Regardless of being in different metals, this can be a majority “Gold” kind of participant, with over 62% of complete revenues coming from gold, and 76% in complete from valuable metals, with over 80% of revenues coming from the Americas – round 15 nations. On the constructive half when it comes to diversification, no single asset is greater than 16% right here. The gold worth signifies that the corporate is efficiently rising its GEO margin.

FNV IR (FNV IR)

The corporate’s enterprise mannequin additionally appears scalable in gentle of the latest outcomes and marketplace for valuable metals. We’re speaking a couple of 9x income enhance in lower than 15 years, whereas G&A has solely elevated 2.5x. The corporate deserves props for this – growing clearly its outcomes whereas solely marginally, by comparability, growing a few of its prices. With $2.3B price of accessible capital of which $1.3B is money and equivalents, the corporate can also be within the enviable place of being totally debt-free on a internet foundation.

Different positives embrace the truth that the enterprise mannequin is confirmed with a compounding 15% TSR for the reason that firm IPO, over 15 consecutive dividend will increase, and in some ways, it’s a market-leading kind of firm.

So, loads of positives right here to make sure.

FNV bulls give attention to the expansion potential and perceived restricted threat of the present operations. There’s additional potential for exploration success on 67,400 km2 price of land, and with comparatively restricted publicity to value inflation, its excessive margins, and general portfolio diversification, I can very clearly see why some would “Love” this participant.

FNV additionally has a monitor report. The corporate has not solely financed, however labored with a mess of mines internationally, and completed so efficiently. Its monitor report contains M&A’s, debt discount performs (like with Teck, Glencore, and so on), and the like.

And the truth that the corporate has been rising, that’s not in query right here.

The thesis for this firm and its potential future appears to be cut up into two camps. The bulls are pointing to a rising worth of gold, the corporate’s strong enterprise mannequin, and the like. Each of these information are plain.

What can also be plain is that FNV has underperformed its friends regardless of a rising gold worth. And at any time when one thing like that occurs, we should always have a look at why this occurs and if we perceive what we’re going into.

FNV does wish to current its case as a low-risk funding. And whereas that is largely true, I do on some bases disagree with how risk-free the corporate is being perceived as.

Why?

Effectively, partnerships and operations for one. Normally, the issue with miners versus investing in one thing like a bullion fund/ETF is prices. Mining corporations are, of their operations, inherently completely different from merely proudly owning gold property, bodily or in any other case. They arrive with operational dangers comparable to the invention, working, and execution of mine initiatives. It’s particularly harmful if OpEx and CapEx rise sooner for the corporate (say, as a result of large inflation) than the revenue it could possibly get from gold – that is the state of affairs we’ve really been having for a while. However right here can also be why I like FNV – due to the enterprise mannequin of gold royalties, the place it collects earnings indirectly from mining. The corporate doesn’t really personal any of the property, which implies it’s insulated from these dangers.

Main constructive – and that is additionally why individuals are often so constructive.

Nevertheless, no enterprise mannequin is risk-free and this one actually isn’t. Whereas it does protect the corporate from operational dangers for its property, it as a substitute creates threat with a few of the firm’s companions that truly function the mines.

Right here the corporate has diversification, which offsets these dangers to singular companions in its operations. Once more, this can be a constructive, however there are a number of examples the place the corporate has really seen dangers from its enterprise mannequin. Just a few months in the past, one among its companions was pressured to shut down one among its copper mining operations in Panama as an illustration.

So to be able to get “on board” with the positivity about Franco-Nevada, I might need an affordable worth as a result of I don’t share a few of the bullishness surrounding the corporate. Any constructive thesis additionally must not solely have a look at the corporate’s operational value immunity (which it has) and the rising worth of gold (and it’s rising) but in addition consider the danger of the corporate’s companions and contracts.

Going ahead, I in reality don’t count on the corporate to outperform throughout 2024E. I count on both a flat outcome or perhaps a decline of 2-4% because of additional declining GEO – and I’m not alone on this. The present anticipated EPS on an adjusted foundation involves a declining pattern of about 2% for 2024E (Supply: Paywalled F.A.S.T graphs hyperlink)

That is why I don’t imagine that the corporate will outperform, however why there may be as a substitute loads of extra room to “go south” to my worth goal right here.

Valuation for Franco-Nevada

So, valuation earlier than threat. The chance to this firm is one I alluded to above. Bulls say the corporate is price a excessive P/E due to its perceived immunity to working dangers as a result of its distancing from operations. And whereas this can be a fact, it’s a fact with some moderation to it. Whereas sure, the corporate is insulated from the day-to-day working dangers, it’s under no circumstances insulated from asset and working dangers as a complete. As a substitute, these asset and working dangers come within the type of counterparty volatility.

This isn’t one thing that’s unknown or hasn’t occurred to the corporate earlier than. It’s occurred a number of instances, that the corporate has been pressured to shutter operations. So whereas I might be keen to characterize FNV’s place as impressively insulated within the context of different gold miners, I might level out to anybody who says that this firm doesn’t have operational dangers, that they merely are available different kinds right here.

That is additionally expressed within the forecast accuracy for the enterprise. A greater type of forecast accuracy would imply that the corporate in reality can be simpler to forecast – however as issues stand, there’s a 33% unfavorable miss likelihood for this firm on a 10-year foundation with a ten% margin of error. That is neither stellar nor among the many greatest in investments that I have a look at.

Once you couple this with the truth that the corporate solely has a 0.87% yield for the inventory, issues instantly get a bit extra “somber”. Once you add the truth that FNV at present trades at a 35x+ P/E, whereas averaging round 53x, some questions on valuation seem.

As I’ve stated repeatedly earlier than, I don’t take into account the corporate’s valuation premium to be legitimate. An organization that during the last 3 years has averaged sub-10% annualized progress doesn’t deserve 30x+ P/E.

And the market agrees with this. For the reason that firm peaked throughout COVID-19, those that invested in Franco-Nevada in 2020 have seen TSRs of someplace alongside the road of unfavorable 13.13%, or 3.26% unfavorable per 12 months. That’s by the way in which inclusive of the corporate’s meager dividend.

A case may be made for investing within the firm at a conservative a number of – and that is the place I are available. I say the conservative a number of for the corporate to spend money on is between 25-28x P/E. What do I base this on? I base this on the bottom conservative a number of that this firm has averaged previously 20 years – round 34x P/E. If we make investments at 25-28x P/E or round $130 Canadian, meaning we’re getting a 15-18% annualized RoR for this funding. Whereas if we make investments right now, and forecast at 34-35x P/E, we get an annualized RoR of lower than 10% per 12 months, as issues stand.

For that motive, I don’t take into account the corporate investable right here both. $130/share for the native FNV ticker stays my goal, and this involves $95/share for the NYSE ticker.

Something above that, and I imagine you’re taking a extra “outsized” kind of threat right here. And that threat may very well be pretty substantial.

Dangers for Franco Nevada

I fail to notice any important upside for FNV that ought to be led to by 2Q of 2024. In reality, it’s doable that the sideways efficiency we’ve seen since 2020 might proceed – and if that is so, your draw back to a decrease P/E may very well be within the double digits. Be aware that I stated ‘might’, that is certainly a threat. One other risk is that you’ve got an upside.

FNV is in spite of everything anticipated to develop at round 10% per 12 months for 2025E and 2026E. However since we’re basing this in giant elements on expectations of what precisely the gold costs throughout these years can be, I’m going to say that I don’t imagine this to be as convincingly correct as some wish to make it, backed up by that 25-33% unfavorable miss ratio.

I imagine by investing right here you’re taking an extreme valuation threat, and for that motive, I might say the correct method to “play” this firm is a “HOLD” – at the least at this specific time.

Thesis

My summarized thesis for Franco-Nevada Company is as follows:

This firm stays “my manner” to spend money on Gold – at the least as soon as the value is in any manner appropriate. That is not the case right now. I might need to wait till the corporate is cheaper earlier than shopping for – and I largely stay at this stance regardless of a 20% decline within the share worth.

Franco-Nevada has no debt, ample money, and very good fundamentals. I view this as a superb enterprise to spend money on – however once more, solely on the proper worth.

FNV is a “HOLD” right here. A worth goal that I might take into account engaging for funding primarily based on my objectives can be round $130/share for the native Canadian ticker – although each investor after all wants to have a look at their very own targets, objectives, and methods. I might additionally at all times seek the advice of with a finance skilled earlier than making funding choices comparable to this.

Keep in mind, I am all about:

1. Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly large – corporations discounted, permitting them to normalize over time and harvesting capital beneficial properties and dividends within the meantime.

2. If the corporate goes effectively past normalization and goes into overvaluation, I harvest beneficial properties and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

This firm is general qualitative.

This firm is basically protected/conservative and well-run.

This firm pays a well-covered dividend.

This firm is at present low-cost.

This firm has a practical upside primarily based on earnings progress or a number of growth/reversion.

The corporate doesn’t fulfill each one among my standards, and I might at present take into account it to be a “Maintain” right here.

[ad_2]

Source link