[ad_1]

djgunner

Article Thesis

TORM plc (NASDAQ:TRMD) is a delivery firm that gives a big 22% dividend yield proper now, based mostly on its most up-to-date quarterly dividend fee. A yield this excessive is dangerous, in fact, and regardless that TORM could be very worthwhile proper now, the dividend yield is probably going not sustainable in the long term. That being stated, TORM plc is a well-managed delivery firm, and whole returns could possibly be engaging even when there’s a dividend discount within the foreseeable future.

Firm Overview

TORM plc is a UK-based delivery firm that’s centered on product tankers. Its ships transfer merchandise akin to diesel or gasoline from one port to a different, however they do not transfer any crude oil — crude oil tankers have totally different specs. TORM’s historical past dates again to the late nineteenth century when Captain D. E. Torm based the corporate that’s nonetheless named after him. The firm grew in measurement over the many years and has grow to be extra simply investable for US-based buyers in 2017 when TORM plc acquired listed on the NASDAQ. Asset administration firm Oaktree holds a big stake of round 47% in TORM plc, that means the free float is round half as excessive as TORM’s share rely of round 94 million.

On the finish of the primary quarter, TORM plc had 89 vessels, which was up by a few proportion factors in comparison with the earlier yr’s quarter. Thus, the fleet is rising for now. The corporate’s fleet measurement grew additional as a result of acquisition of one other 8 product tankers that was introduced in July. The corporate bought one vessel since its Q1 outcomes had been printed. Thus, the vessel rely was 96 after accounting for the acquisition of 8 extra vessels and the disposition of 1 ship when the corporate introduced its Q2 outcomes a few weeks in the past.

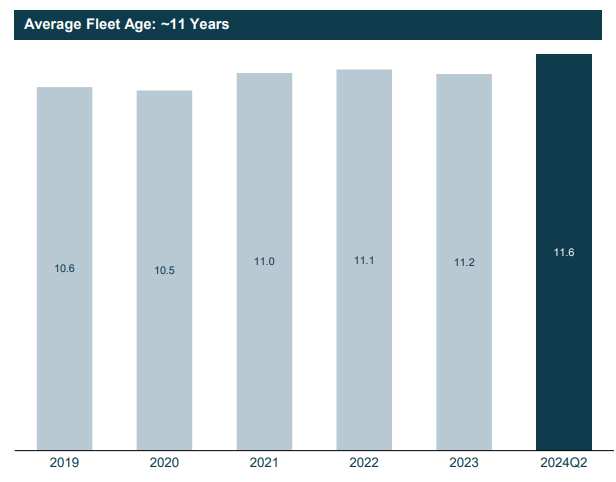

Whereas the dimensions of an organization’s fleet issues, the common age of its fleet is essential as effectively. Newer vessels oftentimes have decrease working bills resulting from extra environment friendly engines, for instance, and so they also can demand greater charges in some circumstances. Importantly, newer vessels even have an extended life span left. Thus, they do not want alternative within the foreseeable future.

The typical age of TORM plc’s automobiles during the last couple of years appears to be like like this:

TORM plc common fleet age over time (TORM plc Q2 outcomes presentation)

The typical fleet age has moved up barely during the last couple of years, and likewise during the last yr, and is now at a stable stage of between 11 and 12 years. TORM’s fleet thus isn’t ultra-new in any respect, however its ships have nonetheless a few years left till they won’t be helpful any longer. Many product tankers are used for 20 years or extra, thus TORM’s fleet age isn’t particularly excessive.

The pattern is pointing to a considerably getting old fleet, nevertheless. Regardless of TORM’s resolution to promote older ships occasionally whereas buying newer vessels, these efforts haven’t stored the common age at a relentless stage. This isn’t a difficulty within the close to time period, however TORM plc will probably must step up its fleet renewal efforts within the coming years with the intention to stop its fleet from getting old additional.

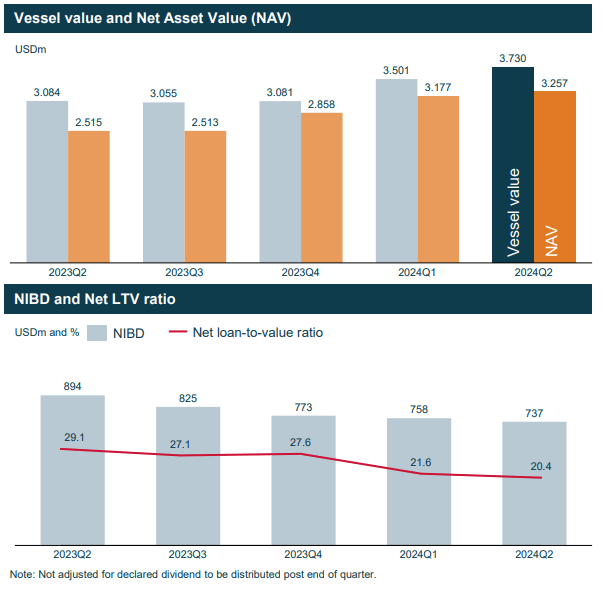

TORM plc must be simply in a position to take action, as its robust steadiness sheet offers it appreciable monetary firepower:

TORM plc’s web asset worth and common mortgage to worth (TORM plc Q2 earnings presentation)

We see that TORM plc’s web asset worth is comparatively near its gross asset worth, resulting from the truth that TORM’s web debt place is reasonably small. On the finish of the second quarter, TORM had $560 million of money on its steadiness sheet, whereas its long-term debt totaled $1,080 million on the identical time. TORM’s web debt thus stood at round $500 million.

On a relative foundation, in comparison with the worth of TORM’s ships, debt ranges are fairly low as effectively, as the web loan-to-value ratio stood at simply 20% on the finish of the latest quarter. That was down on by 120 base factors in comparison with the earlier quarter, and down by a pleasant 870 base factors in comparison with one yr earlier. TORM thus has been deleveraging very efficiently within the current previous, which was made attainable by robust profitability. The steadiness sheet is now fairly clear, which is why TORM should have no issues in buying additional (younger) vessels to cut back the common age of its fleet.

TORM Advantages From A Sturdy Market

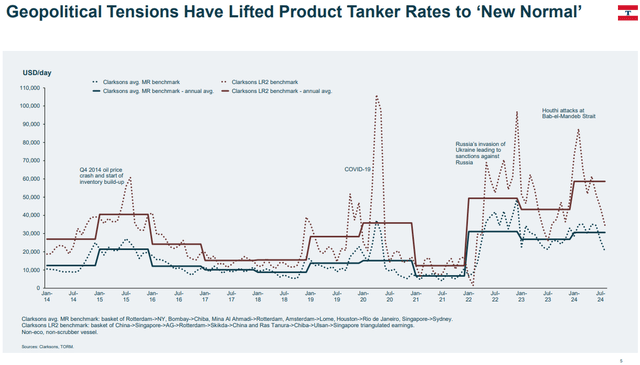

Transport firms can have famously unstable outcomes, as delivery charges can see substantial ups and downs, relying on what the availability of ships and demand for delivery capability appear like. It’s not uncommon to seek out delivery firms that report losses throughout phases when the market is reasonably weak for the kind of ship they personal.

TORM plc, as a product tanker firm, naturally relies upon so much on what charges for product tankers appear like. Within the current previous, charges have been robust, with geopolitics and unrest being a key issue. The Suez Canal is likely one of the most essential delivery strains on the earth, and for the reason that battle within the Center East escalated final October when Hamas attacked Israel, Houthis have been attacking ships that traveled by way of the Suez Canal. On prime of that, there’s additionally the continuing warfare in Ukraine, which provides to international tensions. Within the following chart, we see that these elements have resulted in steep will increase in product tanker charges:

Product tanker charges (TORM plc Q2 earnings presentation)

Since early 2022, when the warfare in Ukraine started, charges have been elevated, and so they rose additional when the battle within the Center East escalated. This has resulted in substantial development in TORM’s time constitution equal charges, which rose from round $36,000 in Q2 of 2023 to round $42,000 in Q2 of 2024.

This enhance in charges, mixed with development in TORM’s fleet, has boosted the corporate’s earnings properly. TORM earned $251 million of EBITDA in Q2 2024, up somewhat greater than 25% in comparison with the earlier yr’s quarter. TORM’s share rely grew during the last yr, resulting from some shares being issued to finance acquisitions, however earnings per share have been nonetheless up by a pleasant 17% year-over-year regardless of the headwind from share rely dilution. With $2.08 per share in earnings in Q2, TORM’s annualized earnings tempo is round $8.30 — for an organization that trades at $33 per share proper now, that is wonderful, because it pencils out to an earnings a number of of round 4.

It’s thus not stunning that TORM plc can supply very good dividend funds proper now. The corporate’s most up-to-date quarterly dividend fee stood at $1.80 per share, which pencils out to $7.20 on an annual foundation. Relative to a share value of $33, that makes for a dividend yield of twenty-two%, or greater than 5% per quarter.

Dangers And Sustainability Of Dividends

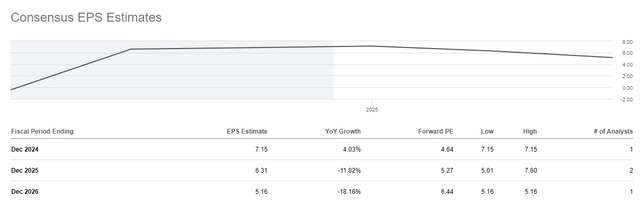

When an organization’s dividend yield is as excessive as that of TORM plc, the market clearly believes that dividends will decline in the long term. And in TORM’s case, that is sensible. Earnings are forecasted to peak in 2024, with decrease earnings per share being forecasted for 2025 and 2026, wanting on the Wall Avenue analyst consensus estimates for these years:

TORM plc earnings per share estimates (In search of Alpha)

Earnings are forecasted to say no by round 30% by the tip of 2026, relative to what’s forecasted for this yr. And even after we have a look at this yr’s estimate, we see that the analyst neighborhood expects a slowdown throughout H2 — TORM earned $4.40 per share in H1, however the full-year estimate is just a bit north of $7, implying that earnings in Q3 and This fall will likely be effectively beneath $2 per share, respectively.

If earnings drop to round $5 per share by 2026, then the present dividend of $7.20 per yr isn’t sustainable. There’s, in fact, no assure that the analyst neighborhood is true about decrease earnings in 2025 and 2026, however it could, I consider, not be a serious shock. In spite of everything, the present geopolitical issues will hopefully come to an finish, and if tensions within the Center East ease, then product tanker charges will probably decline.

In relation to TORM’s earnings, geopolitical tensions are “constructive”, whereas waning tensions are “damaging” as they may lead to decrease TCE charges and decrease earnings, all else equal. Peace within the Center East and an finish to the Suez Canal assaults is thus a “threat” for TORM. There’s additionally the chance that additional fleet getting old will finally harm TORM’s earnings, though I consider that the corporate’s clear steadiness sheet will give the corporate the flexibility to resume its fleet in time.

Is TORM A Purchase?

TORM is well-managed, has a sizeable and rising fleet, and a really clear steadiness sheet. Earnings proper now are wonderful, however they may probably not stay this excessive eternally. The dividend could be very excessive proper now, however will probably decline within the coming years.

That being stated, even when the dividend have been to be minimize in half, the yield would nonetheless be very robust, at 11%. And contemplating that TORM trades beneath web asset worth (NAV of $3.3 billion, versus a market capitalization of $3.1 billion), TORM could possibly be a superb funding nonetheless — buyers should not suppose that the dividend will at all times stay this excessive, nevertheless.

[ad_2]

Source link