[ad_1]

How To Profitably Commerce Bitcoin’s In a single day Classes?

As curiosity in cryptocurrencies continues to surge, pushed by every new worth rally, crypto property have solidified their place as one of many essential asset courses in international markets. Not like conventional property, which primarily commerce throughout normal working hours, cryptocurrencies commerce 24/7, presenting a novel panorama of liquidity and volatility. This steady buying and selling surroundings has prompted us to research how Bitcoin, the flagship cryptocurrency, behaves throughout intraday and in a single day intervals. With Bitcoin’s rising availability to each retail and institutional traders by means of ETFs and different funding autos, we hypothesized that buying and selling exercise in these distinct timeframes may reveal patterns just like these seen in conventional markets, the place returns are sometimes impacted by liquidity shifts throughout off-peak hours.

Now we have been protecting the ideas and matters referring to crypto extensively. For extra related articles, examine our cryptocurrency buying and selling analysis subpage or search for the articles with the “cryptocurrencies” tag on our weblog. Alternatively, you may go to our intensive library of cryptocurrency buying and selling methods.

This research’s major function is

to investigate the day by day versus the in a single day (nightly) buying and selling classes within the crypto(currencies) house

examine whether or not the general in a single day impact exists within the major uncrowned flagship assetl Bitcoin (BTC), and in that case, to what extent

analyze, whether or not the “day of the week” or “weekend” impact exists in cryptocurrencies (Bitcoin)

use the entire above to construct a seasonal technique that may exploit the seasonal impact within the BTC market

Background

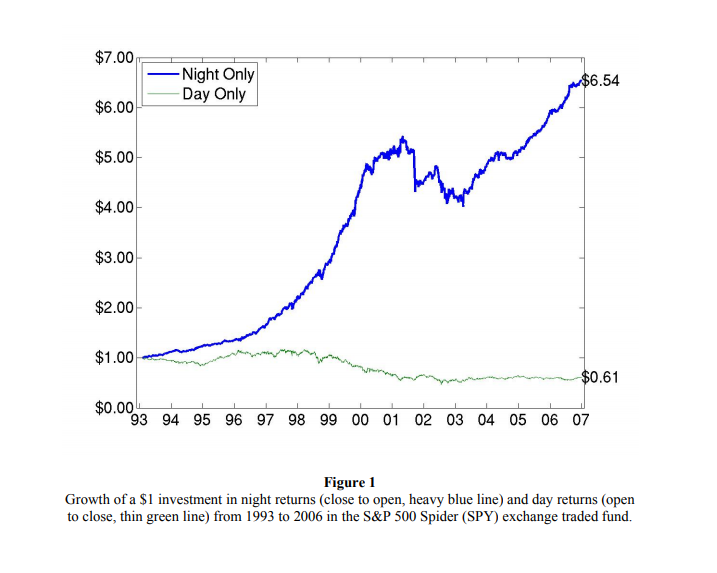

Referencing the graph from our prior analysis on the Lunch Impact within the S&P 500 and different main U.S. inventory indices, we noticed that the majority SPY and inventory index efficiency accrues largely throughout the nightly classes:

And for placing issues into perspective, here’s a shorter pattern from the analysis paper revealed in 2008 (as we will see, not loads has modified during the last 16 years):

In a single day Anomaly as introduced by Cliff, Cooper, Gulen: Return Variations between Buying and selling and Non-Buying and selling Hours: Like Night time and Day.

Our goal and aim, subsequently, is to know the influence of day by day and nightly classes on Bitcoin efficiency, notably in gentle of the introduction of Bitcoin ETFs. This means there is perhaps a shift from 24/7 buying and selling to a extra structured buying and selling surroundings akin to these on conventional exchanges (such because the NYSE, NASDAQ, AMEX, ARCA, and so forth).

Motivation

We suspect that since inflows and outflows from ETFs buying and selling on these TradFi domains are extremely tied to exchanges’ open hours, it can grow to be extra prevalent that Bitcoin buying and selling modifications are increasingly more tied to these of conventional property similar to equities and bonds.

Institutional merchants often unload or provoke (take) positions primarily on the open(ing) and shut of the principle session, the place they’ve sufficient liquidity to fulfill their orders (not accounting for block trades in darkish swimming pools or TWAP orders throughout the day); therefore, the primary and final buying and selling moments when it comes to time-span of minutes in day by day buying and selling classes are erratic and unstable (which day-traders try for; atypical traders not a lot so). Add market makers’ pursuits in thoughts, which can be some over-standing stock on their books they should liquidate, in addition to choices sellers hedging their flows. You get the right time for conflicting pursuits that ceaselessly help the worth discovery and transfer the worth towards the market’s consensus view, often forming the pattern in traded property for the remainder of the day.

This stuff had been unknown primarily to Bitcoin, because it was traded in lots of decentralized venues (spot or futures), which allowed solely instantaneous worth arbitrage amongst them if liquidity constraints had been in favorable situations.

Bitcoin is traded nonstop and infrequently might be the primary, riskiest asset readily liquidated in anticipation of upcoming volatility, similar to (geo)political tensions or different unspecified excessive and non-predictable occasions when conventional finance exchanges are closed. Now that Bitcoin has acquired Wall Avenue’s blessing and approval and is accepted as a reliable asset class by ETFs, the SEC can be changing into a bit of bit much less strict in regulation by taking small steps similar to approving choices buying and selling on mentioned ETFs, BeInCrypto knowledgeable in late October. So, have Bitcoin’s distinctive traits relating to classes’ distribution of returns grow to be distorted, shifted, reversed, and are actually extra resembling time-tested property like ETFs and shares?

Information

Our evaluation is predicated on the hourly BTC information from the Gemini Information web page in intervals starting from 2015-10-08 to 2024-10-15. We outline the day by day session as efficiency between 10 am EST and 4 pm EST throughout buying and selling days when the NYSE change is opened. The entire hours out of this interval are outlined as in a single day classes. It’s the identical information supply we utilized in our earlier article wherein we revisited trend-following and mean-reversion methods in Bitcoin.

We assume that the underlying futures of ETF BITO can precisely monitor and predict the affect of cryptocurrencies’ “institutionalization” precisely from its Inception Date on 2021-10-18. Due to this fact, for simplicity, we cut up our pattern into an in-sample interval (till October 2021, throughout which the straightforward ETF buying and selling car was not obtainable for BTC buying and selling) and an out-of-sample interval (after October 2021).

We perceive that our definition of in-sample and out-of-sample intervals could be very arbitrary. It’s not potential to outline the precise time when Bitcoin (and different cryptocurrencies) turned a conventional asset and was now not thought-about an unique funding. The road between conventional property and different property is a blurry one. What we need to present is that there’s/was a shift in Bitcoin’s habits in in a single day and intraday classes over time.

Preliminary Investigations

After gathering all of the wanted information, we began processing it and growing our preliminary investigation.

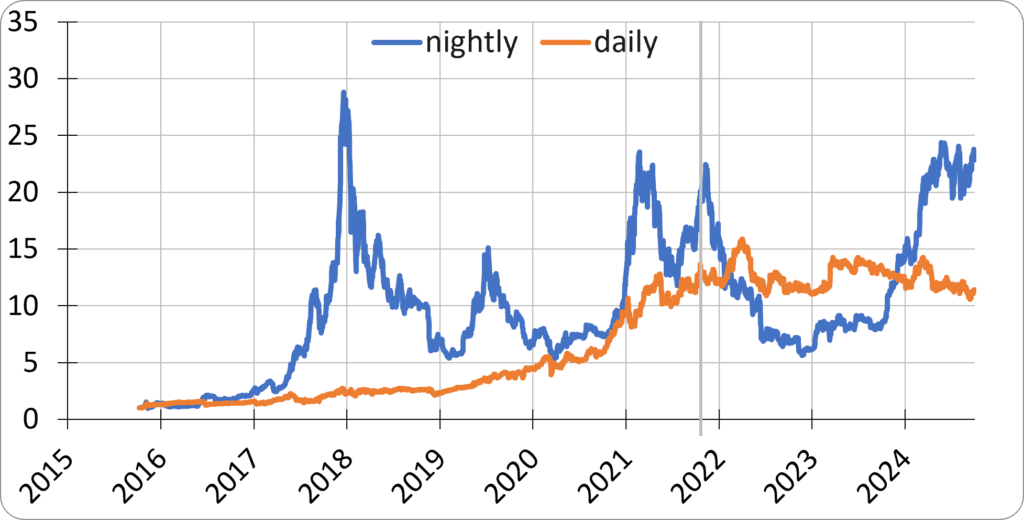

The next graph evaluation illustrates returns throughout day by day vs. nightly buying and selling classes over time:

We highlighted milestones of our curiosity and marked the launch of the primary BTC ETF (2021-10-18) inside the graph with a thick gray line.

As an summary, we put two factors of essential observations:

A good portion of robust BTC actions (each up-trends and downtrends) are inclined to happen within the nightly classes.

The day by day classes carried out properly till 2021 however have plateaued during the last three years.

The idea concerning the “In a single day Impact” posits that the majority efficiency in dangerous property similar to equities is realized throughout nightly (so from near open; “nocturnal”) buying and selling classes as compensation for the related dangers. That could be a time whenever you can’t often commerce loads, so whenever you maintain an asset in a single day, you might be compensated for its illiquidity (or decrease liquidity) with greater efficiency. As Bitcoin more and more integrates into conventional monetary programs, this precept can be anticipated to use to BTC.

Our constructed close-to-open versus open-to-close efficiency graph above confirms the beforehand outlined theoretical assumptions. Initially (till round 2021), the efficiency of the BTC throughout day by day classes was considerably optimistic, and BTC holders may multiply their property with a low threat (volatility and drawdowns). The nightly classes provided greater efficiency but in addition greater threat (volatility and drawdowns). As Bitcoin regularly turned an asset class just like different essential asset courses, returns over the day by day classes diminished, and a lot of the BTC returns since 2021 had been realized throughout the nightly classes. That is exactly the identical sample as in shares or fairness indexes!

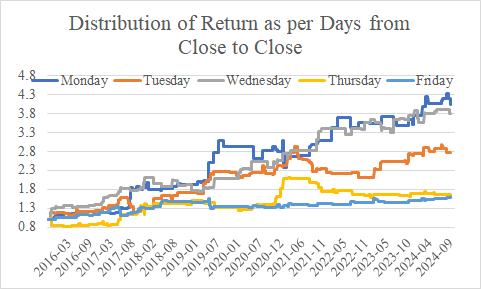

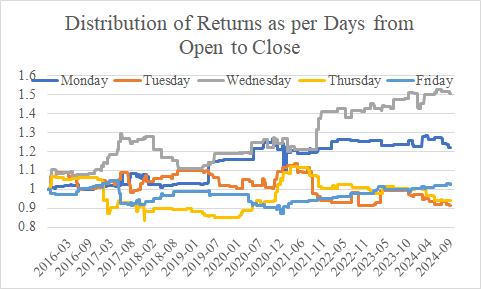

Deconstructing the Composition of Bitcoin Returns for Every Day

Let’s transfer on and decompose Bitcoin’s efficiency by particular person buying and selling days (Monday, Tuesday, and so on.), analyzing close-to-open, open-to-close, and close-to-close classes. In keeping with our definition, Monday evening’s efficiency contains the interval from Friday near Monday morning (the entire weekend with conventional finance, whether or not securities or foreign exchange, exchanges are closed). Tuesday evening’s efficiency contains the interval from Monday’s shut (4 pm EST) till Tuesday’s open (10 am EST), and so on.

The outcomes are displayed in tabular and graphical codecs, with a conclusion indicating that the first (most contributing) efficiency happens on Monday, Tuesday, and Wednesday close-to-close classes. Nevertheless, this efficiency is pushed primarily by the nightly classes. So Bitcoin strikes to the optimistic territory primarily between Friday’s shut and Monday’s open (so over the weekend), between Monday’s shut and Tuesday’s open, and between Tuesday’s shut and Wednesday’s open. As we transfer nearer to Friday, Bitcoin’s efficiency diminishes (in intraday and in a single day classes, too). Plainly, finally, there actually exists a “Weekend Impact” in Bitcoin returns—a major influence of Saturdays and Sundays when conventional monetary exchanges (like NYSE) are closed.

OK, we all know that BTC is delicate to the in a single day/intraday cut up and it’s delicate to the Weekend Impact. Now, the query is, what can we do about it? Our subsequent sections purpose to discover a approach to revenue from this discovering.

Replication of the Earlier Analysis Methodology

Firstly, we took our older trend-following research and replicated the MAX technique with 5-day, 10-day, and 50-day excessive parameters.

Our trend-following and mean-reversion research was backtested on day by day bars with 0.00 GMT time stamps and utilizing a 24/7 buying and selling calendar (trades might be executed on Saturdays, Sundays, and in addition throughout public holidays). Due to this fact, our first step was to examine how the trend-following technique that buys new native highs (5, 10, 20, 30, 40, or 50-days) performs if we restrict our buying and selling choices and might commerce solely on the ETF market shut at 4 pm on days when the NYSE is open. We used Gemini information and the NYSE calendar to create such information sequence and examined our MAX technique on it. This easy technique (purchase a Bitcoin within the type of cryptocurrency, futures contract, CFD, or ETF at NYSE shut, when Bitcoin is on the native X-day excessive, maintain for one buying and selling day) might be simply executed with ETFs from 2021 onwards. Nevertheless, we aren’t utilizing the precise ETF closing costs however Gemini BTC information. This enables us to check the technique’s efficiency even earlier than any Bitcoin ETFs had been launched.

And right here we’ve a complete graph showcasing all variations in mixture for the buying and selling interval from close-to-close, together with detailed tables:

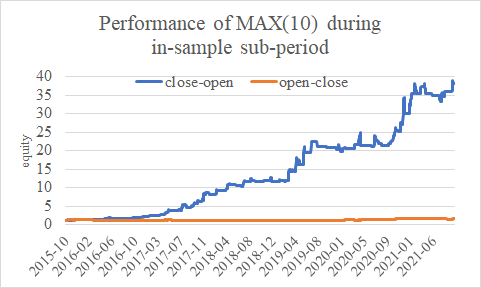

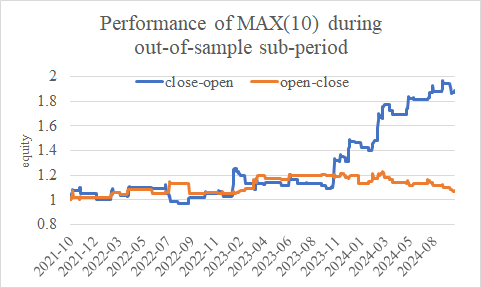

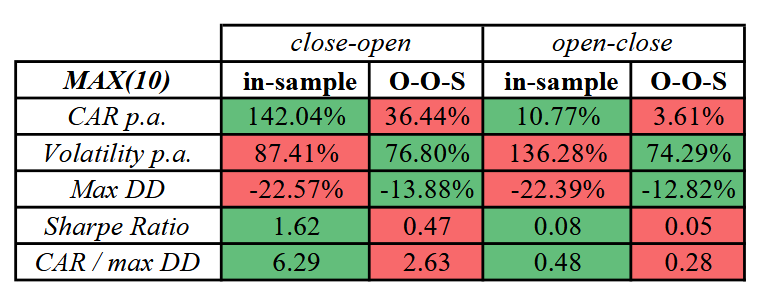

For consistency with our prior publications, we finally moved ahead and used a 10-day model regardless of it not being optimum with the best returns. This model, for functions of this analysis publication, requires the presentation of close-to-open and open-to-close efficiency graphs, tables, and an acceptable abstract as beforehand described:

As we will see, Bitcoin MAX technique carried out higher throughout the first sub-period earlier than the primary ETF introduction. Within the out-of-sample interval, the technique nonetheless has over 35% efficiency with a minimal -12% maximal drawdown (and considerably outperforms the underlying Bitcoin market on a risk-adjusted foundation), however as Bitcoin has grow to be a typically accepted, mainstream asset class, the straightforward trend-following technique that buys new native highs doesn’t supply the identical juice as earlier than. What can we do about it? Let’s focus our consideration on the in a single day anomaly and filter our trades a bit of. It’s the identical trick we used once we had been investigating the in a single day reversal within the high-yield market.

MAX(10) Technique Efficiency Throughout Sub-Intervals

Firstly, we will attempt to examine the 10-day MAX technique in close-to-open and open-to-close sub-periods (only a quick reminder that in-sample is till October 2021, and out-of-sample [OOS] is from October 2021 onwards):

This part demonstrates that the majority returns of the MAX(10) technique all through historical past, each in-sample and out-of-sample, are generated throughout the in a single day buying and selling session (from near open).

Closing Buying and selling Technique Proposal

OK, we’re close to the top of our evaluation. We discovered that Bitcoin is delicate to intraday vs. in a single day cut up, to the day-of-the-week (or Weekend) impact, plus it traits loads (as soon as, when it’s on the native excessive, then it often continues in optimistic pattern and finally to the upper worth). Due to this fact, we suggest a consolidated MAX(10) technique, which operates completely throughout evening classes spanning Friday to Monday evening, Monday to Tuesday evening, or Tuesday to Wednesday evening. This last technique is illustrated with a single fairness curve, efficiency desk, and an evaluation of the technique’s efficiency each in-sample (as much as 2021) and out-of-sample:

Now we have a superb instance of the mixture of weekend and in a single day results, as you may go lengthy on Friday’s shut in case you are on an area 10-day MAX, maintain the BTC till Monday morning (open), and go lengthy once more on Monday’s and/or Tuesday’s shut if the Bitcoin remains to be on the native 10-day MAX. The technique provides a pretty Sharpe ratio and low threat and exhibits that Bitcoin remains to be a younger asset, burdened by inefficiencies rather more than conventional, mature basic asset courses and their constituents.

In gentle of our evaluation, the straightforward technique targeted on nightly buying and selling classes has yielded substantial insights into Bitcoin’s efficiency dynamics. The technique, working completely throughout evening classes from Friday to Monday, Monday to Tuesday, and Tuesday to Wednesday, has demonstrated that a good portion of Bitcoin’s returns is realized in a single day. This sample is in keeping with conventional asset courses, the place the In a single day threat premium is acknowledged, suggesting that as Bitcoin integrates extra into standard monetary markets, its return distribution mirrors that of established property.

The findings from this technique point out that Bitcoin, regardless of its distinctive traits and the 24/7 buying and selling surroundings, behaves equally to different monetary devices when topic to institutional buying and selling patterns. This implies a gradual alignment with conventional market behaviors, probably pushed by the rising participation of institutional traders and the introduction of Bitcoin ETFs. These outcomes spotlight the significance of contemplating buying and selling session dynamics when growing buying and selling methods and threat administration frameworks for Bitcoin and different cryptocurrencies.

In conclusion, our research reinforces that the in a single day impact considerably drives Bitcoin’s efficiency. The technique’s success underscores the worth of specializing in particular buying and selling classes to optimize returns and handle dangers successfully. As Bitcoin continues to achieve legitimacy and combine into conventional monetary programs, ongoing analysis will likely be important to adapt buying and selling methods and capitalize on rising traits, making certain that traders stay forward of the curve on this evolving market.

Writer: Cyril Dujava, Quant Analyst, Quantpedia

Are you searching for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you need to study extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you need to study extra about Quantpedia Professional service? Test its description, watch movies, assessment reporting capabilities and go to our pricing supply.

Are you searching for historic information or backtesting platforms? Test our checklist of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookDiscuss with a pal

[ad_2]

Source link

, Boeing (NYSE:BA)")

{kind=link}