[ad_1]

Moussa81

There are a lot of “Buffetisms” on the market, and whereas most are acquainted with his saying to “be grasping when others are fearful, and be fearful when others are grasping”, I imagine a extra considerate and insightful assertion of his is that “the market is designed to switch wealth from the impatient to the affected person.”

That is as a result of when many development shares are buying and selling at what I’d contemplate to be nosebleed valuations, I am fortunately shopping for into worth shares at what I’d contemplate to be a fraction of what they’re value.

In actual fact, I do not thoughts worth shares remaining underpriced for an prolonged time frame, as that merely offers me the chance to greenback value common into them to develop my earnings stream.

This brings me to the next 2 picks, each of which have lengthy observe information of elevating their dividend for over 25 consecutive years. Each commerce at interesting valuations for affected person buyers prepared to go in opposition to the grain and be paid to attend with above-average yields, so let’s get began!

#1: Medtronic

Medtronic (MDT) is a healthcare expertise whose merchandise serve the areas of Cardiovascular, Medical Surgical, Neuroscience, and Diabetes. This consists of proprietary units akin to pacemakers, insulin pumps, spinal implants, ventilators, surgical navigation methods, amongst others.

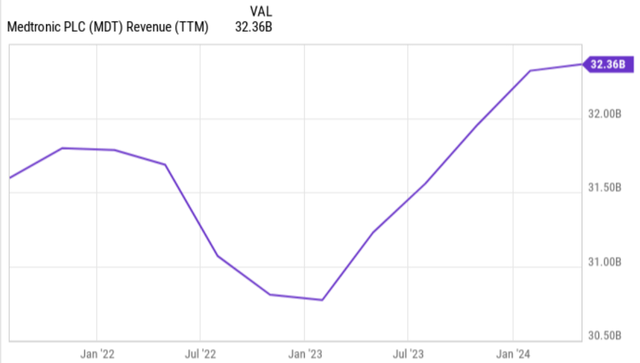

MDT inventory continues to commerce weakly in comparison with the place it was within the Fall of 2021, throughout which it hit a excessive of $135. On the present value of $81.37, the inventory is down 40% over this timeframe. MDT’s weak inventory value efficiency belies total strengths within the enterprise. As proven beneath, MDT’s income has greater than recovered from hitting a trough in late 2022, with TTM income sitting at $32.4 billion.

YCharts

MDT continued this development development in fiscal This autumn 2024 (ended on April twenty sixth), throughout which natural income grew by 5.4% to $8.6 billion, exceeding Wall Avenue analyst expectations by $150 million. Additionally encouraging, MDT’s adjusted EPS of $1.46 landed on the higher finish of steerage and free money move grew by 14% YoY to $5.2 billion. MDT’s top-line development was supported by mid-single digit development in U.S. and Europe, and by a robust 13% development in rising markets, together with China, the place it is since emerged from COVID-related lockdowns.

Administration is guiding for natural income development within the 4% to five% vary for the present 2025 fiscal yr in progress. That is primarily based on the expectation that MDT will lengthen its management in key classes, together with the introduction of Aurora EV-ICD, an implantable extravascular defibrillator to deal with sudden cardiac arrest, surgical improvements such because the Hugo robotic-assisted surgical procedure system, and the upcoming Simplera Sync sensor integration with MDT’s MiniMed 780G system for the therapy of Diabetes.

In the meantime, MDT maintains a robust stability sheet with an ‘A’ credit standing from S&P. This consists of having a secure internet debt to TTM EBITDA ratio of 1.87x, sitting nicely beneath the three.0x market typically thought-about secure for non-REIT/Utility firms.

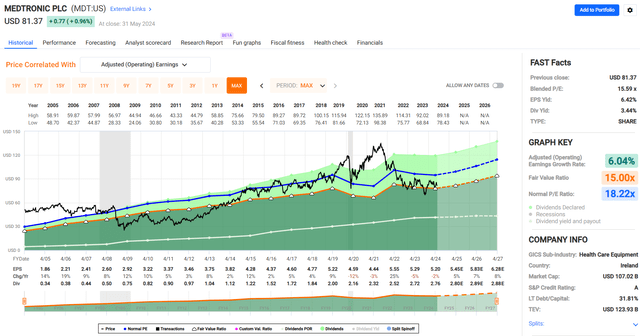

This helps MDT’s 3.4% dividend yield, which comes with a secure 53% payout ratio and a 5-year dividend CAGR of 6.7%. Whereas MDT is not essentially low cost the present value of $81.37 with a ahead PE of 14.9, it does sit nicely beneath its historic PE of 18.2, as proven beneath.

FAST Graphs

I imagine MDT deserves to commerce at its historic PE contemplating its Dividend Aristocrat standing with 46 years of consecutive annual raises below its belt, giving credence to its sturdiness. Furthermore, with the aforementioned latest encouraging development and analysts anticipating 7% annual EPS development over the subsequent 2 years, MDT may moderately ship market-level efficiency even with no reversion to its imply valuation.

#2: Altria

Altria (MO) is formally a Dividend Aristocrat regardless of having decreased its dividend in 2008, and that is as a result of its spin-off, Philip Morris Worldwide (PM) made shareholders entire from a cashflow standpoint with its personal dividend, and has elevated it yearly since then.

Those that observe the tobacco trade would most likely know that it is at the moment present process its greatest transition in a long time, with people who smoke having expanded choices that embody vaping, heat-not-burn, and nicotine pouches.

Altria has been considerably late within the recreation following its missteps from its failed Juul stake and with peer British American Tobacco (BTI) taking the lead in vaping and Philip Morris Worldwide taking the lead in heat-not-burn merchandise via IQOS and nicotine pouches via Zyn.

MO has seen a difficult top-line surroundings because of people who smoke switching to alternate options and unlawful vapes within the U.S. with revenues internet of excise taxes declining by 1% YoY throughout Q1 2024. This was pushed largely by a ten% YoY decline in cigarette volumes, resulting from pure declines in smoking, increased gasoline costs, and switching to each authorized and unlawful merchandise within the vaping class.

Regardless of challenges within the present working surroundings, I imagine it might be a mistake to put in writing off Altria this early within the recreation because it pertains to nicotine transition. That is contemplating the encouraging quantity development in MO’s NJOY, which continued to see elevated market share development of 0.6% on a sequential QoQ foundation to 4.3% on the finish of Q1. Additionally encouraging MO’s nicotine pouch, On!, noticed 0.7% sequential market share development to 7.1%.

As well as, MO not too long ago filed a PMTA with the FDA for NJOY’s blueberry and watermelon flavors with the NJOY ACE 2.0 platform, which has Bluetooth-enabled age restrictions to stop utilization amongst youths. This, together with crackdowns on unlawful vaping, might be tailwinds for the corporate that the market has not totally priced in.

Within the meantime, it is also value noting that MO nonetheless retained an 8.1% stake in Anheuser-Busch InBev (BUD) as of the top of Q1, which it may proceed to monetize to purchase again shares. MO additionally maintains a robust stability sheet with a BBB credit standing from S&P and a secure internet debt to EBITDA ratio of two.1x. This consists of MO having retired $1.1 billion value of debt in Q1 alone.

This lends help to MO’s 8.5% dividend yield, which comes with a secure 79% payout ratio that is consistent with MO’s historic ~80% payout ratio. MO’s dividend can be positioned to develop this yr, contemplating that administration is guiding for two% to 4.5% EPS development this yr.

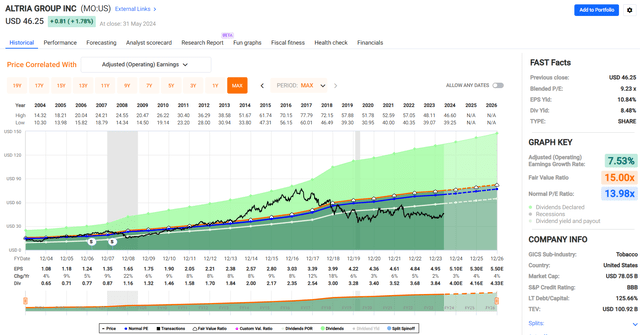

I see worth in MO on the present value of $46.25 with a ahead PE of 9.1, sitting nicely beneath its regular PE of 14.0, as proven beneath.

FAST Graphs

Promote aspect analysts who observe the corporate estimate 4-5% annual EPS development over the subsequent two years, which might be pushed by value elasticity in conventional smokables together with development in newer classes like On! nicotine pouches and NJOY and share buybacks. As such, MO may ship above-market complete returns after we mix the dividend yield with even the decrease finish of administration’s EPS steerage, and this doesn’t embody the potential for share value appreciation to MO’s long-term historic valuation.

Investor Takeaway

Medtronic and Altria current compelling alternatives for affected person buyers targeted on worth shares with robust dividend histories. Medtronic, a healthcare expertise chief, presents a 3.4% yield backed by 46 years of consecutive annual raises and strong development prospects in its cardiovascular and diabetes sectors.

Altria, regardless of latest challenges within the tobacco trade, maintains an 8.5% yield and potential upside from its NJOY e-vapor enterprise and strategic investments. Each firms, with their stable stability sheets and dedication to shareholder returns, are well-positioned to ship long-term worth via dividends and potential capital appreciation.

[ad_2]

Source link