[ad_1]

Monty Rakusen

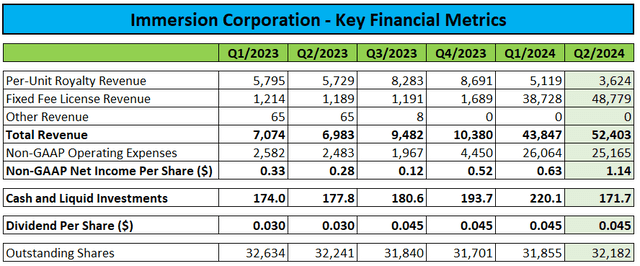

After the shut of Tuesday’s common session, Immersion Company or “Immersion” (NASDAQ:IMMR) reported robust second quarter outcomes. Nevertheless, the corporate’s current acquisition of a controlling stake in Barnes & Noble Schooling (BNED) has resulted within the unlucky requirement to consolidate the brand new subsidiary’s monetary outcomes.

The consolidation of Barnes & Noble Schooling’s extremely seasonal operations will lead to Immersion reporting large losses within the first half of every calendar yr, adopted by robust earnings within the second half.

Whereas Immersion hasn’t stopped breaking out revenues and belongings for its core licensing operations, the Q2/2024 numbers for non-GAAP working bills and non-GAAP web earnings per share embrace the contributions from Barnes & Noble Schooling:

Regulatory Filings / Firm Press Releases

Reported will increase in mounted price license income and profitability in H1/2024 have been principally the results of a litigation settlement and associated licensing settlement with Meta Platforms (META) in addition to the current renewal of present agreements with key licensees Nintendo (OTCPK:NTDOY, OTCPK:NTDOF) and Samsung Electronics (SSLNF).

As these funds will not repeat within the close to future, licensing revenues are more likely to come down fairly meaningfully within the second half of the yr. Nevertheless, with Barnes & Noble Schooling’s busiest quarter straight forward, Immersion is more likely to report a really robust Q3 in November.

The sequential discount within the firm’s money and liquid investments displays Immersion’s current $50.1 million funding (web of reimbursements) in Barnes & Noble Schooling, as additionally outlined within the firm’s quarterly report on kind 10-Q:

As a part of the Transactions, the Firm acquired 42% of all excellent frequent shares of Barnes & Noble Schooling, in addition to management over Barnes & Noble Schooling by means of the 5 Immersion-appointed board seats.

The full consideration transferred was roughly $50.1 million, consisting of $52.2 million in money consideration paid to Barnes & Noble Schooling much less $2.1 million in transaction prices incurred by Immersion however reimbursed by Barnes & Noble Schooling.

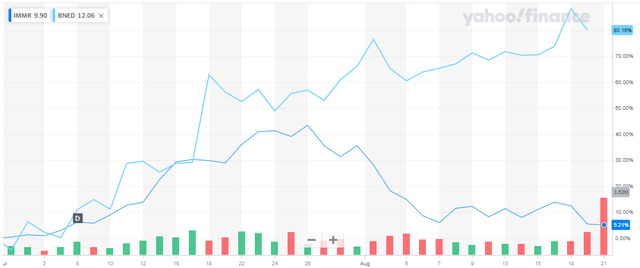

In trade, Immersion obtained roughly 11 million shares of Barnes & Noble Schooling with a present market worth of near $135 million, which interprets into an nearly 170% acquire inside simply two months.

Because the starting of July, Barnes & Noble Schooling’s inventory worth has doubled on favorable regulatory developments and hopes for robust development within the firm’s all-important First Day Full (“FDC”) choices, as outlined in nice element by fellow contributor The Minotaur in a current article.

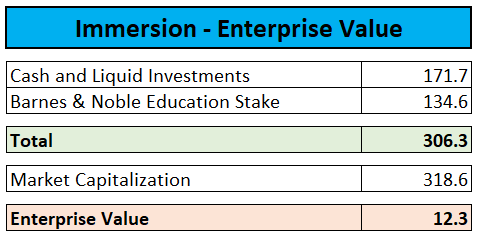

Including Immersion’s money and liquid investments to its stake in Barnes & Noble Schooling leaves nearly no worth for the corporate’s core licensing enterprise:

Yahoo Finance / Writer’s Calculations

Given the corporate’s current success in its licensing efforts, Mr. Market’s judgement seems a bit harsh right here, however the inherent unpredictability and low popularity of the enterprise seems to maintain most buyers sidelined.

Fellow contributor Gary Bourgeault truly referred to as Immersion “The Haptic Ambulance Chaser” in an article printed early final yr, whereas some tech information outfits are outright labeling the corporate a “patent troll”.

Administration’s method to shareholder communication and capital returns would not precisely assist issues both, as the corporate declines to carry quarterly convention calls and solely pays out a measly quarterly money dividend of $0.045 per share with an annualized yield of under 2%.

Whereas Immersion has an energetic $50 million inventory repurchase program, the corporate hasn’t purchased again any shares thus far this yr.

With stock-based compensation now not offset by repurchases, the variety of excellent shares has moved again up in current quarters.

As a way to appeal to new consumers to the inventory, administration would probably should resume share repurchases and enhance the quarterly money dividend fairly meaningfully.

Immersion might additionally attempt to monetize its lately acquired stake in Barnes & Noble Schooling and distribute the proceeds in type of a particular dividend. Nevertheless, any share gross sales into the open market would probably trigger Barnes & Noble Schooling’s inventory worth to break down.

That mentioned, additional appreciation within the worth of the corporate’s stake in Barnes & Noble Schooling may also lead to a elevate to Immersion’s share worth, albeit this isn’t a given by any means as evidenced by the chart comparability:

Yahoo Finance

No less than in my view, Immersion is reasonable for a cause, as market members are scrutinizing the shortage of predictability and unsure long-term worth of the corporate’s core licensing operations.

As well as, the efficiency of Barnes & Noble Schooling will rely on a positive regulatory setting. Ought to the Division of Schooling make modifications to the present opt-out mannequin for inclusive entry applications, the corporate’s enterprise would probably take a serious hit.

Furthermore, the consolidation of Barnes & Noble Schooling’s extremely seasonal operations is more likely to confuse buyers going ahead.

In my opinion, I’m not keen to turn into uncovered to those uncertainties, even with the core licensing enterprise valued at discount ranges.

Consequently, I’m initiating protection of Immersion Company with “Maintain”.

Nevertheless, buyers feeling snug with the enterprise mannequin and Barnes & Noble Schooling’s prospects may take into account betting on a near-term enhance in shareholder capital returns, which I take into account the method greatest suited to elevate Immersion’s inventory worth.

Backside Line

Immersion Company’s core licensing operations delivered robust second quarter outcomes, with profitability boosted by the popularity of recent licensing offers with tech giants from the likes of Meta Platforms, Samsung, and Nintendo. Nevertheless, these funds will not repeat within the second half, so outcomes are more likely to be decrease going ahead.

Whereas the acquisition of a controlling stake in Barnes & Noble Schooling has turned out to be a serious winner for the corporate, the requirement to consolidate Barnes & Noble Schooling’s extremely seasonal operations will make it harder for buyers to evaluate Immersion Companies monetary efficiency.

The current recapitalization has put Barnes & Noble Schooling on stronger monetary footing, however the firm stays depending on a positive regulatory setting.

In my opinion, I’m not keen to turn into uncovered to the inherent uncertainties of Immersion Company’s enterprise, even with the core licensing operations valued at discount ranges.

Consequently, I’m initiating protection of Immersion Company with “Maintain”.

[ad_2]

Source link