[ad_1]

JHVEPhoto

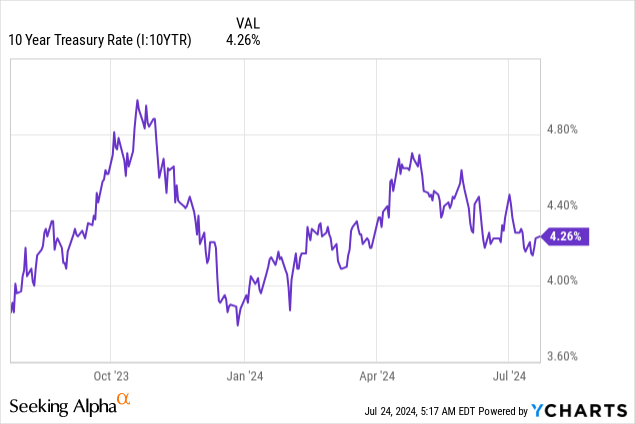

Intuit Inc.’s (NASDAQ:INTU) inventory has been among the many largest beneficiaries of the latest drop within the time period premium in early November of final 12 months, which marked a peak in U.S. Treasury yields.

To place it briefly, through the U.S. Treasury Quarterly Refunding Announcement in November, the Treasury introduced a considerably decrease share of long-dated bonds to be issued within the coming months, which was a powerful sign of decrease provide forward. This resulted in larger costs and decrease yields for these bonds, which in flip stopped the yield curve steepening course of and, as talked about above, marked a peak in yields.

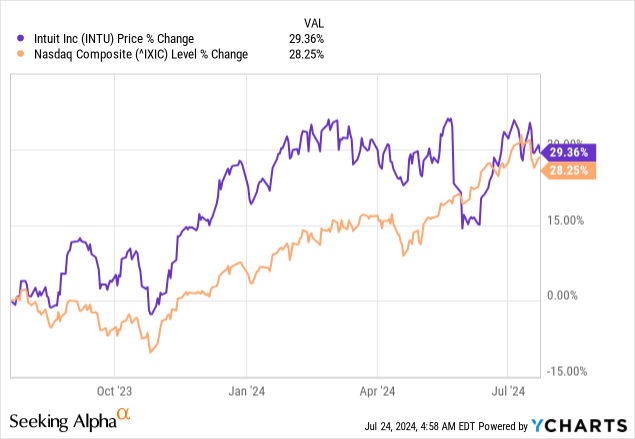

That’s the reason, since 1st of November final 12 months, we have now been observing sturdy demand for longer period equities and specifically high-growth know-how shares, equivalent to Intuit. Consequently, INTU is up almost 30% over the previous 12-month interval, and so is the Nasdaq Composite Index.

Nevertheless, there are two main issues forward for Intuit’s buyers, which make the present ranges extremely unsustainable for my part.

Firstly, the aforementioned tailwind is slowly being exhausted as yields are creeping up. And secondly, as we see on the graph above, the efficiency hole between INTU and the Nasdaq has disappeared.

The explanation why that is regarding is that INTU is a excessive beta inventory and, as such, is predicted to outperform the index throughout market upturns. However in latest months, INTU has been going sideways despite the fact that the market continued to make new all-time highs. This implies that there are issues beneath the floor which might be more likely to proceed to weigh on the share value.

Priced For Perfection

Earlier than we go into the underlying cause as to why Intuit’s inventory is underperforming the market in latest months, we must always present some context on why the inventory is buying and selling at such a big premium.

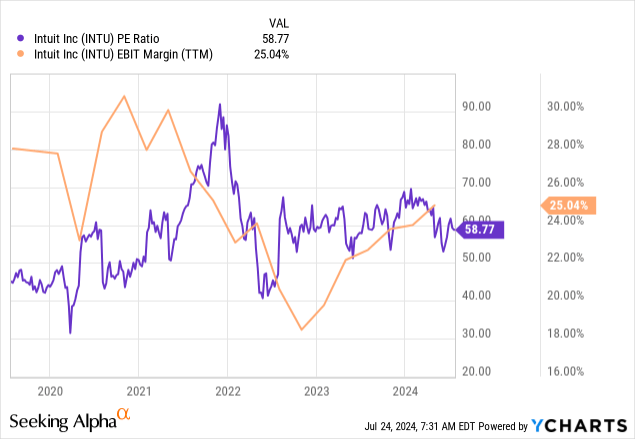

Lately, the inventory has been buying and selling roughly throughout the vary of 60 to 70 occasions earnings – a spread that’s simple to justify for a inventory that’s anticipated to develop at double-digit charges for a few years forward, however a lot more durable to justify for a inventory the dimensions of INTU. Furthermore, Intuit’s working margin has fallen well-below its earlier highs of round 30%. In the intervening time, the trailing 12-month EBIT margin is simply 25%, which continues to be a long-way to go earlier than returning to the earlier highs.

However even when that is not convincing sufficient that Intuit’s inventory is presently buying and selling at a premium that’s laborious to justify, then we might take a more in-depth have a look at how the inventory is priced in opposition to a broader peer group within the software program area.

On the graph under, we have now internet revenue margins plotted on the x-axis and value/gross sales multiples on the Y-axis, which supplies us a superb indication of how every inventory trades relative to its present profitability profile. Variations between implied multiples (those who could be on the pattern line) and the precise ones might usually be defined by both expectations of modifications in profitability, irregular income progress or different aggressive benefits that will permit a given firm to attain a better return on capital than its friends.

It’s fascinating to notice that the INTU is a inventory that has a big distinction between its precise and implied value/gross sales a number of. Furthermore, its present P/S a number of of 11.3 additionally lies above the trend-line, which implies that both the inventory is considerably overpriced or it’s assuming a major enchancment within the internet revenue margin to round 30% (from 19% at current).

ready by the writer, utilizing knowledge from Searching for Alpha

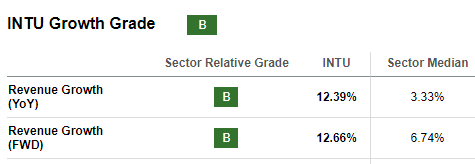

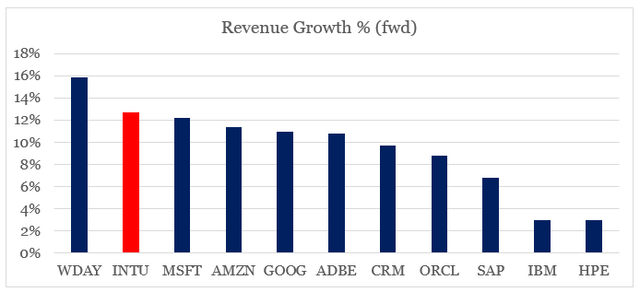

Whereas this may very well be partially defined by Intuit’s excessive anticipated income progress fee of round 12%, it’s not sufficient to justify such a big hole. For instance, the typical ahead income progress fee of the entire peer group is 9.5%, which does not make Intuit a noticeable exception in terms of progress.

Searching for Alpha ready by the writer, utilizing knowledge from Searching for Alpha

Not solely that, however it seems that Intuit is likely to be having a troublesome time sustaining this progress fee, which in itself might imply a downward a number of repricing over the approaching 12 months.

Progress Headwinds

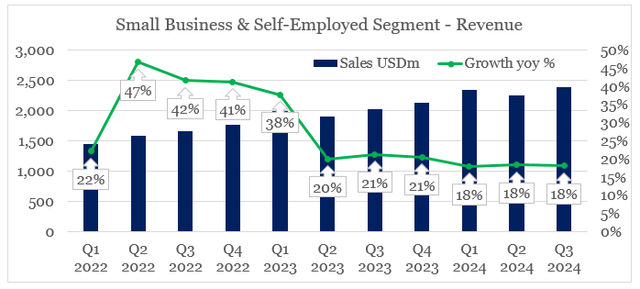

In relation to income progress, the Small Enterprise & Self-Employed phase, which includes the QuickBooks and Mailchimp manufacturers, is by far crucial for Intuit. As of the tip of fiscal 12 months 2023, round 56% of Intuit complete revenues have been derived from this phase.

Intuit 10-Ok SEC Submitting

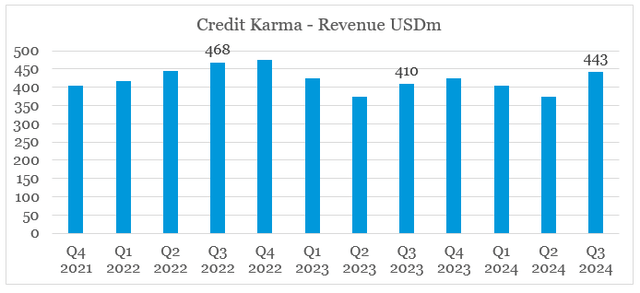

That’s the reason, despite the fact that the just lately acquired Credit score Karma enterprise is usually getting a lot of consideration, it’s nonetheless a comparatively small a part of Intuit.

The Small Enterprise & Self-Employed phase was an enormous beneficiary of the digitalization developments following the pandemic lockdowns. That’s the reason, we noticed quarterly year-on-year progress charges within the neighborhood of fifty% in fiscal 12 months 2022. Since then, nevertheless, these progress charges have been progressively normalizing – from round 20% in FY 2023 to 18% in FY 2024.

ready by the writer, utilizing knowledge from SEC Filings

As progress within the phase naturally slows down, Intuit’s administration is betting on AI assistants to distinguish its providing and reinvigorate progress.

As a part of our monetary planning course of, we have now recognized key areas inside our Large Bets the place we plan to speed up investments to ship better affect. These embody: Large Guess 1 GenAI to ship done-for-you experiences with Intuit Help, Large Guess 2 go-to-market investments for TurboTax Dwell and QuickBooks Dwell, embedding AI powered consultants throughout our small enterprise choices (…)

Supply: Intuit Q3 2024 Earnings Transcript

AI investments have been additionally used as an excuse for the just lately introduced lay-offs, as supposedly the corporate is specializing in improvements on this space to additionally enhance effectivity and cut back fastened prices.

Searching for Alpha

The latter goal seems extra more likely to be achieved, however the differentiating issue of AI within the sphere of accounting and different value-added providers for small enterprise, and people is more likely to be much less pronounced. Versus extra artistic areas, such because the areas of operation of Adobe (ADBE) for instance, the place getting access to monumental quantities of information to coach AI is a key aggressive benefit, in accounting software program, AI is much less more likely to be a differentiating issue. Having stated that, within the short-term AI value-added providers might present a profit for many of Intuit’s providers, however past that, AI is extra more likely to create a degree taking part in discipline.

I additionally discover it regarding that Intuit seems to be as soon as once more specializing in acquisitions as a imply to reinvigorate progress. I’ve criticized this strategy again in 2022, after I argued that the technique holds monumental dangers for shareholders and is unlikely to generate worth for shareholders.

Only a month in the past, Intuit’s administration introduced that it’s going to purchase know-how from a mobility threat intelligence supplier, Zendrive.

Searching for Alpha

The intention is more likely to merge these providers with the prevailing choices of the just lately acquired Credit score Karma, in an effort to compete extra efficiently. Up to now, the acquisition of Credit score Karma has didn’t live-up to the expectations, with the enterprise staying flat to barely declining lately.

ready by the writer, utilizing knowledge from SEC Filings

Due to this fact, evidently the know-how acquisition from Zendrive, is probably going geared toward enhancing Credit score Karma’s present standing, as these service choices are more likely to be bundled collectively. For my part, that is an try to enhance Credit score Karma’s competitiveness and put it on a path to future progress. Assumption that, if true, would imply that Intuit’s administration has most definitely overpaid for the enterprise and will face extra difficulties sooner or later.

With that in thoughts, buyers ought to anticipate extra info to be supplied through the upcoming quarterly outcomes, however thus far, evidently Intuit is likely to be going through yet one more wave of acquisitions in an effort to retain its excessive income progress and compete in its new service segments.

Investor Takeaway

Intuit’s share value is as soon as once more buying and selling close to all-time highs, and buyers needs to be cautious when extrapolating returns from the previous 12-month interval into the long run. Sure macro tailwinds are fading, and the inventory is already pricing-in a notable enchancment in margins. On the similar time, I stay skeptical that the present income progress may very well be sustained, which holds further dangers for shareholders.

Having stated all that, nevertheless, I’d additionally not be inclined to take a brief place in Intuit for one easy cause – the potential of the macroeconomic surroundings to stay supportive. As I mentioned at first, the latest fall within the time period premium has been extremely supportive for the inventory, and though we have now seen a gradual enhance in yields in latest months, the financial coverage might as soon as once more shift to being extremely supportive as soon as once more. Though such a state of affairs could be unsustainable, it might present a powerful short-term tailwind for Intuit’s share value.

[ad_2]

Source link