[ad_1]

I got here throughout a report from CoreLogic the opposite day that stated residence fairness mortgage lending elevated to its highest stage since 2008.

At any time when anybody hears the date “2008,” they instantly consider the housing bubble within the early 2000s.

In spite of everything, that’s when the housing market went completely sideways after the mortgage market imploded.

It’s the yr all of us use now as a barometer to find out if we’re again to these unsustainable instances, which might solely imply one factor: incoming disaster.

Nonetheless, nuance is vital right here and I’m going to let you know why the numbers from 2008 and the numbers from 2024 aren’t fairly the identical.

First Let’s Add Some Context

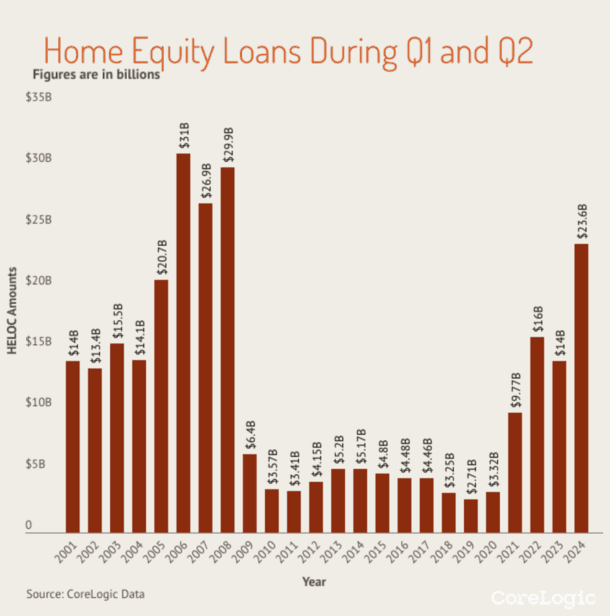

CoreLogic economist Archana Pradhan famous that residence fairness mortgage lending (not HELOCs) grew to the very best level for the reason that first half of 2008 through the first two quarters of 2024.

In the course of the first half of this yr, mortgage lenders originated greater than 333,000 residence fairness loans totaling roughly $23.6 billion.

For comparability sake, lenders originated $29.9 billion in residence fairness loans through the first half of 2008, simply earlier than the housing market started to crash.

It was the final massive yr for mortgage lending earlier than the underside fell out. For reference, residence fairness lending totaled simply $6.4 billion in 2009 and barely surpassed $5 billion yearly up till 2021.

A part of the explanation it fell off a cliff was attributable to credit score circumstances changing into frozen just about in a single day.

Banks and lenders went out of enterprise, property values plummeted, unemployment elevated, and there was merely no residence fairness to faucet.

As soon as the housing market did get well, residence fairness lending remained subdued as a result of lenders didn’t take part as they as soon as had.

As well as, quantity was low as a result of first mortgage charges have been additionally so low.

Due to the Fed’s mortgage-backed securities (MBS) shopping for spree, generally known as Quantitative Easing (QE), mortgage charges hit all-time lows.

The favored 30-year fastened went as little as 2.65% in early 2021, per Freddie Mac. This meant there wasn’t actually a lot motive to open a second mortgage.

You would go along with a money out refinance as a substitute and safe a number of actually low cost cash with a 30-year mortgage time period.

That’s precisely what householders did, although as soon as first mortgage charges jumped in early 2022, we noticed the alternative impact.

So-called mortgage price lock-in grew to become a factor, whereby householders with mortgage charges starting from sub-2% to 4% have been dissuaded from refinancing. Or promoting for that matter.

This led to a rise in residence fairness lending as householders might borrow with out interrupting their low first mortgage.

What About Inflation Since 2008?

Now let’s examine the 2 totals and think about inflation. First off, $29.9 billion remains to be properly above $23.6 billion. It’s about 27% larger.

And that’s simply evaluating nominal numbers that aren’t inflation-adjusted. If we actually need to examine apples-to-apples, we have to take into account the worth of cash over the previous 16 years.

In actuality, $24 billion immediately would solely be value about $16.7 billion in 2008, per the CPI Inflation Calculator.

That might make the 2024 first half complete extra on par with the 2001-2004 years, earlier than the mortgage business went completely haywire and threw frequent sense underwriting out the door.

Merely put, whereas it could be the very best complete since 2008, it’s not as excessive because it appears to be like.

On prime of that, residence fairness ranges at the moment are the very best on file. So the quantity that’s being tapped is a drop within the bucket compared.

In 2008, it was frequent to take out a second mortgage as much as 100% mixed mortgage to worth (CLTV).

That meant if residence costs dipped even just a little, the house owner would fall right into a detrimental fairness place.

Immediately, the everyday house owner has an excellent low loan-to-value ratio (LTV) due to way more prudent underwriting requirements.

Usually, most lenders gained’t transcend 80% CLTV, leaving in place a large fairness cushion for the debtors who do elect to faucet their fairness immediately.

There’s Additionally Been Very Little Money Out Refinancing

Lastly, we have to take into account the mortgage market general. As famous, many householders are grappling with mortgage price lock-in.

They aren’t touching their first mortgages. The one sport on the town if you wish to faucet your fairness immediately is a second mortgage, corresponding to a house fairness mortgage or HELOC.

So it’s pure that quantity has elevated as first-mortgage lending has plummeted. Consider it like a seesaw.

With only a few (to virtually no) debtors electing to disturb their first mortgage, it’s solely pure to see a rise in second mortgage lending.

Again in 2008, money out refinancing was big AND residence fairness lending was rampant. Think about if no one was doing refis again then.

How excessive do you assume residence fairness lending would have gotten then? It’s scary to consider.

Now I’m not going to sit down right here and say there isn’t extra threat within the housing market on account of elevated residence fairness lending.

After all there may be extra threat when householders owe extra and have larger month-to-month debt funds.

However to match it to 2008 could be an injustice for the numerous causes listed above.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and current) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for warm takes.

[ad_2]

Source link

")

{kind=link}