[ad_1]

It’s not fairly Halloween simply but, however dwelling patrons could have already gotten scare.

The 30-year mounted mortgage, for which most patrons depend on, jumped from round 6% to just about 6.75% within the span of about three weeks.

And this passed off proper after the Fed lastly pivoted and minimize its personal fed funds fee. Good timing I do know.

Previous to this fee reversal, mortgage charges had steadily fallen all the way in which from 8%, their current cycle excessive that sarcastically passed off simply earlier than final Halloween.

Discuss yr for charges, transferring down two full share factors. However the pattern is now not our pal, a minimum of within the interim.

Now I’d wish to make a case for why this truly is likely to be good for the housing market.

Greater Mortgage Charges May Encourage Extra Than Decrease Charges

I do know what you’re considering, increased mortgage charges can’t presumably be good for the struggling housing market.

Particularly this housing market, which is presently probably the most unaffordable in latest historical past.

However bear with me right here. I acquired to considering not too long ago how the low mortgage charges didn’t appear to get potential dwelling patrons off the fence.

As famous, charges got here down fairly a bit from their cycle highs, falling about two share factors.

In Mid-September, you might get a 30-year mounted for round 6% for the common mortgage state of affairs. And in actuality, a lot decrease in the event you had a vanilla mortgage (excessive FICO, 20% down, and many others.) and/or went with a reduction lender.

The identical was true in the event you paid low cost factors at closing. I used to be even stumbling upon charges within the excessive 4% vary at the moment.

Absolutely that might be adequate to get potential patrons to chew. However the mortgage utility knowledge simply didn’t reply.

You’ll be able to blame seasonality, given it being a suboptimal time for charges to hit their lowest ranges since early 2023.

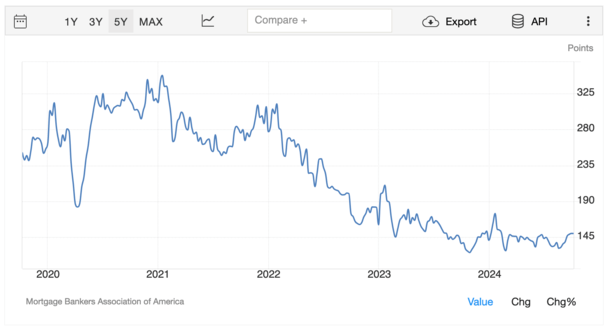

However in the event you take a look at the seasonally adjusted dwelling buy utility index from the Mortgage Bankers Affiliation (MBA), you’ll see it barely budged. See the chart above from Buying and selling Economics.

In the meantime, refinance purposes surged, granted they’re much extra rate-sensitive. Nonetheless, given the very best charges in years, dwelling patrons simply didn’t present up.

And this was stunning as a result of there had been a story that they’d flock to the housing market the second charges dropped.

The truth is, there have been some who argued to purchase a house early to beat the push. That too gave the impression to be little greater than a misguided dream. And it’d all need to do with motivation.

Perhaps Residence Consumers Needed Even Decrease Mortgage Charges

With the ability of hindsight, maybe the offender was the concept that falling mortgage charges merely make dwelling patrons thirsty for higher.

It’s a bizarre psychological factor. When you get slightly of one thing good, you need much more. And when you get extra, it doesn’t appear pretty much as good because it as soon as was. You want much more.

Merely put, falling mortgage charges appeared to show much less motivational than rising charges, as unusual as that sounds.

When charges are going up, there’s an intense urgency to lock in a fee earlier than they get even worse.

When charges are falling, you may bide your time and await even higher. That seems to be precisely what potential patrons did.

Regardless of beforehand being instructed to beat the push, they have been now being instructed to attend. So not solely did decrease charges not get patrons off the fence, they virtually entrenched them additional.

After all, I’ve argued not too long ago that it’s now not in regards to the mortgage charges, and will in truth be different issues.

It is likely to be uncertainty concerning the economic system, it might be dwelling purchaser burnout, it may merely be that dwelling costs are too excessive. Sure, that’s a risk too!

Nevertheless, and right here’s the even stranger factor, now that patrons have been spooked with increased charges, that might truly get them to leap off the fence!

(picture: Marcin Wichary)

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) dwelling patrons higher navigate the house mortgage course of. Observe me on Twitter for decent takes.

[ad_2]

Source link

{kind=link}