[ad_1]

malerapaso

Persevering with my sequence of articles that pay due consideration to intricately calibrated fairness methods on the intersection of things, as we speak I wish to talk about the JPMorgan Diversified Return U.S. Fairness ETF (NYSEARCA:JPUS). In keeping with its web site, it’s

Designed to supply home fairness publicity with potential for higher risk-adjusted returns than a market cap-weighted index.

That is an formidable proposition. However the very essence of investing is to grasp that expectations and actuality diverge ceaselessly. And alas, that is the case with JPUS.

Regardless of having a number of sturdy durations since its launch in September 2015, JPUS was neither able to outperforming the iShares Russell 1000 ETF (IWB), which is the fund that tracks its benchmark, on an annualized foundation, nor delivering extra comfy risk-adjusted returns (my metrics of alternative are the Sharpe, Sortino, and Treynor ratios). It’s true that there’s one thing to admire about its issue combine (i.e., a price tilt), however I might abstain from establishing a Purchase thesis utilizing this premise solely.

General, whereas I consider JPUS is a automobile able to minimizing losses and taming volatility at instances, it’s powerful to discover a cause why I ought to provoke protection with a Purchase ranking.

What’s the foundation for JPUS’ technique?

Launched in 2015, JPUS is managed passively, with the premise for its technique being the JP Morgan Diversified Issue US Fairness Index. From web page 1 of the abstract prospectus, we all know that its parts “are chosen primarily from the constituents of the Russell 1000 Index.” Relating to the elements thought of within the course of, the next particulars are supplied:

The principles primarily based proprietary multi-factor choice course of makes use of the next traits: worth, momentum, and high quality. The Underlying Index is designed so that every of the person traits is given equal enter in safety choice.

So in essence, it appears it is a principally large-cap echelon-centered technique with an element trifecta at its core.

JPUS efficiency: a number of brilliant spots, however principally unimpressive

There’s something to understand about JPUS’ efficiency, with its maybe most important achievement being the truth that it beat IWB and the iShares Core S&P 500 ETF (IVV) in 2021 and 2022. This means that the ETF was not solely able to benefiting from the capital rotation to cyclicals but in addition supplied some safety amid the gloomiest days of the financial policy-driven bear market.

Yr JPUS IVV IWB 2021 29.08% 28.76% 26.32% 2022 -8.48% -18.16% -19.19% Click on to enlarge

Knowledge from Portfolio Visualizer

That is mirrored within the draw back seize ratio as nicely.

Metric JPUS IVV IWB Draw back Seize 93.44% 100% 101.54% Click on to enlarge

Knowledge from Portfolio Visualizer. IVV was chosen as a benchmark

Nonetheless, neither its compound annual progress charge nor risk-adjusted returns measured utilizing the Sharpe, Sortino, and Treynor ratios delivered over the October 2015-July 2024 interval have been interesting sufficient. That’s to say, JPUS underperformed each IVV and IWB. One other downside is the utmost drawdown (delivered in the course of the March 2020 pandemic-driven sell-off), which, surprisingly, gave the impression to be the deepest within the group.

Metric JPUS IVV IWB Begin Stability $10,000 $10,000 $10,000 Finish Stability $26,712 $33,661 $32,598 CAGR 11.77% 14.73% 14.31% Commonplace Deviation 15.87% 15.75% 15.99% Finest Yr 29.08% 31.25% 31.06% Worst Yr -8.48% -18.16% -19.19% Most Drawdown -25.95% -23.93% -24.57% Benchmark Correlation 0.95 1 1 Sharpe Ratio 0.67 0.84 0.81 Sortino Ratio 1.01 1.32 1.26 Treynor Ratio 11.21% 13.3% 12.8% Click on to enlarge

Knowledge from Portfolio Visualizer. IVV was chosen as a benchmark

How does JPUS’ issue combine stack up towards that of IVV?

Above, I’ve illustrated that JPUS’ historic efficiency was clearly inadequate for a Purchase thesis. However returns are, after all, not the one parameter a thesis can theoretically be primarily based on. A method centered on returns solely is clearly a myopic and dangerous one. A way more vital ingredient is the issue story, or, to be exact, the query of whether or not the issue proportions are ample for the present market narrative. Right here, there’s undoubtedly one thing to understand about JPUS, however these details are nonetheless inadequate to justify a bullish stance.

Delving deeper, as of August 27, there have been 362 frequent shares and REITs within the JPUS portfolio, with the overlap with IVV being at round 72.1%. Although JPUS has publicity to virtually all of the trillion-dollar corporations, apart from Amazon (AMZN), its portfolio is far lighter in them. For instance, Apple (AAPL) is IVV’s largest holding with a 6.9% weight. In the meantime, JPUS has allotted simply 0.37% to it. And its key holding, Kellanova (Ok), has only a 0.52% weight. And right here comes its first relative benefit: a price tilt.

To corroborate, beginning with the market cap, as of August 28, JPUS had a weighted common of $108.7 billion, as per my calculations, whereas the S&P 500 ETF had that determine 9x bigger. And that is hardly a coincidence that its 5.1% adjusted earnings yield gave the impression to be a lot increased than IVV’s adjusted EY of three.7%. In addition to, there’s a huge distinction in allocations to shares with a B- Quant Valuation grade or increased: 26.3% vs. 6.2%.

It’s value clarifying that once I say ‘relative,’ I imply that for many buyers who consider the rally will proceed for the foreseeable future, these traits doubtless imply little. Nonetheless, for these contrarians who consider a great correction is lengthy overdue, JPUS definitely affords one thing.

However a price tilt and strong progress publicity are antithetical in nature. So JPUS is considerably behind IVV in the case of the expansion indicators, like these offered within the desk under.

Metric JPUS IVV EPS Fwd 6.30% 18.27% Income Fwd 3.97% 12.20% EBITDA Fwd 4.84% 20.11% Click on to enlarge

Created by the writer utilizing information from In search of Alpha, IVV, and JPUS

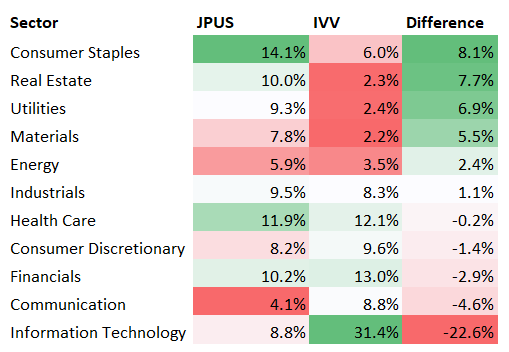

Partially, that is pushed by the sector proportions. As an illustration, in comparison with IVV (which has a sector combine near that of the Russell 1000 ETF), JPUS is considerably underweight in IT and chubby in client staples. The desk under, ready utilizing information from the ETFs and the iShares Core S&P Whole U.S. Inventory Market ETF (ITOT), reveals different vital variations.

Created by the writer; information from ITOT, IWB, IVV, and JPUS

JPUS’ second relative benefit is its publicity to the low volatility issue, which is once more the consequence of the sector combine.

ETF 24M Beta 60M Beta Quant Momentum B- or increased JPUS 0.81 0.99 70% IVV 1.07 1.06 71.3% Click on to enlarge

Calculated by the writer utilizing information from In search of Alpha and the ETFs

It’d look a bit counterintuitive assuming the technique is aware of momentum, not low beta. Nonetheless, on web page 2 of the abstract prospectus, it’s clarified that the index

Targets fairness securities which have increased risk-adjusted returns relative to these of their sector friends over a twelve month interval. The twelve month returns are divided by the twelve month volatility of the returns to get the risk-adjusted returns.

In order volatility can be taken under consideration, low beta is explainable. Once more, this could attraction to buyers who’re awaiting for the expansion premia to turn into slimmer, or, one other means of claiming, the market to surrender a large deal of positive factors. I personally don’t view this as a base-case state of affairs.

Nonetheless, with reference to high quality, I might argue that JPUS is weaker than the S&P 500 ETF, with its weighting schema being the important thing cause. The information under are what I’m basing my opinion on.

Metric JPUS IVV Web Earnings Margin 14.6% 21.5% Return on Belongings 7.3% 14.3% Adjusted Return on Fairness 19.2% 20.1% Quant Profitability B- or increased 87.9% 94.8% Click on to enlarge

Calculated by the writer utilizing information from In search of Alpha and the ETFs

Closing ideas

JPUS is about making use of the issue trifecta in a principally mega- and large-cap universe, with the purpose being to seize the “potential for higher risk-adjusted returns than a market cap-weighted index.” And actually, JPUS does numerous issues proper. It affords a significant depth and breadth of publicity with out over-reliance on only a handful of market darlings which were dashing increased, a price tilt, and principally fantastic high quality. Importantly, its expense ratio of 18 bps appears to be like razor-thin assuming the advanced factor-driven methodology. Nonetheless, neither its efficiency nor issue combine can persuade me {that a} Purchase ranking is justified.

[ad_2]

Source link