[ad_1]

Cash Entice xefstock

Efficiency Evaluation

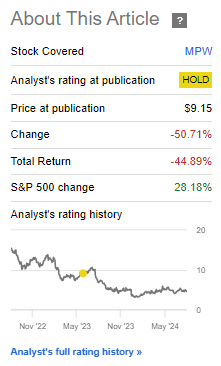

My final article on Medical Properties Belief (NYSE:MPW) was 1 yr in the past. On the time of publication, the sentiment on In search of Alpha was strongly bullish. Nevertheless, I warned of additional asset high quality dangers within the REIT. Sadly, I rated the safety a ‘Impartial/Maintain’ as a substitute of a ‘Promote’, which was clearly the mistaken name:

Efficiency since Creator’s Final Article on Medical Properties Belief (In search of Alpha, Creator’s Final Article on Medical Properties Belief)

Trying again, I feel my evaluation was each appropriate and well timed. Nevertheless, I made a mistake within the ranking evaluation as I believed a low valuation (P/B < 1) and a brief squeeze danger as a consequence of a moderately excessive quick curiosity (20%) have been saving graces. The important thing studying I extracted from this was to position much more weight on the steadiness sheet fundamentals, operational well being of the enterprise and the inventory momentum than valuation and a short lived, perceived quick squeeze danger.

Be aware that these learnings aren’t merely theoretical; I utilized them efficiently in my ‘Robust Promote’ views on B. Riley (RILY), which appeared similar to MPW regardless of being in a unique enterprise altogether; a weak steadiness sheet and cash-bleeding operational efficiency.

1 yr later, not a lot has improved for MPW

I nonetheless have a bearish thesis on Medical Properties Belief:

Impairments have develop into too common The corporate is bleeding money Leverage ranges are excessive and unlikely to profit a lot from price cuts There are indicators of operational weak spot within the broader portfolio as properly Regardless of buying and selling under guide worth, it’s possible a worth lure

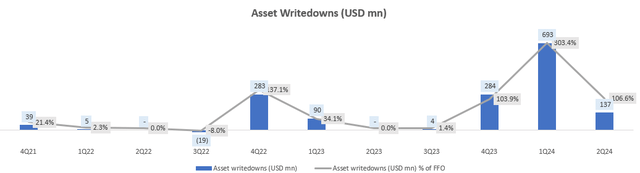

Impairments have develop into too common

Impairments or asset writedowns are presupposed to be one-time results. Nevertheless, for Medical Properties Belief, they’ve develop into an everyday phenomenon:

Asset Writedowns (USD mn) (Firm Filings, Creator’s Evaluation)

This is because of underlying weaknesses in its portfolio of tenants. For instance, its largest tenant Steward making up 30% of total revenues at the beginning of FY23 went underneath chapter. And final yr, one other tenant referred to as Prospect (11% income combine in FY22) additionally went vital impairments of just about $300 million.

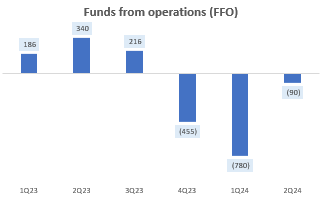

The corporate is bleeding money

MPW’s FFOs are in a gap for the previous 3 quarters, which have seen an outflow of $1.3 billion in complete:

Funds from Operations (FFO) (USD mn) (Firm Filings, Creator’s Evaluation)

This isn’t an excellent signal because the present liquidity (money and equivalents) within the firm is a mere $607 million.

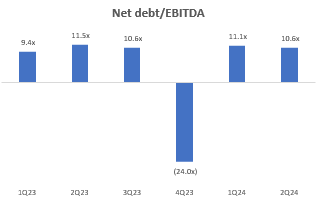

Leverage ranges are excessive and unlikely to profit a lot from price cuts

Leverage ranges are additionally excessive, with Web debt/EBITDA at 10-11x:

Web Debt/EBITDA (Firm Filings, Creator’s Evaluation)

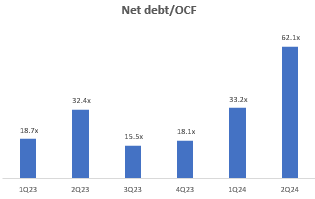

And the image appears even worse if we have a look at a cash-flows measure of the extent of leverage used; internet debt to working money stream (OCF) is greater than 30x on an annualized foundation and 62x as of Q2 FY24:

Web Debt/OCF (Firm Filings, Creator’s Evaluation)

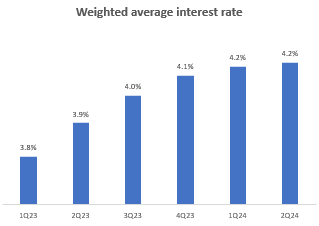

Furthermore, with an elevated weighted common rate of interest of 4.2%:

Weighted Common Curiosity Price (Firm Filings, Creator’s Evaluation)

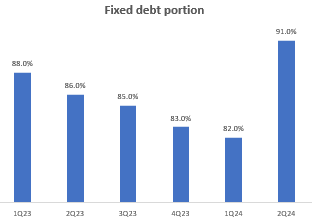

And a excessive mounted debt portion of 91%, leaping 900bps solely within the final quarter:

Fastened Debt Portion of Complete Debt (Firm Filings, Creator’s Evaluation)

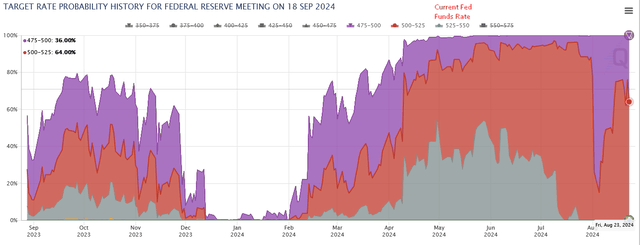

MPW has worsened its positioning to profit from a price lower upcoming in September 2024 (64% probability of a 25bps lower and a 36% probability of a 50bps lower):

Goal Price Possibilities for the September 2024 Fed Assembly (CME FedWatch, Creator’s Annotations)

Federal Reserve Chair Jerome Powell nearly as good as confirmed the market’s expectations for a price lower in subsequent month’s assembly a number of days in the past on the Jackson Gap Symposium:

The course of journey [of rate cuts] is obvious, and the timing and tempo of price cuts will rely upon incoming knowledge, the evolving outlook, and the steadiness of dangers.

– Federal Reserve Chair Jerome Powell on the 2024 Jackson Gap Symposium

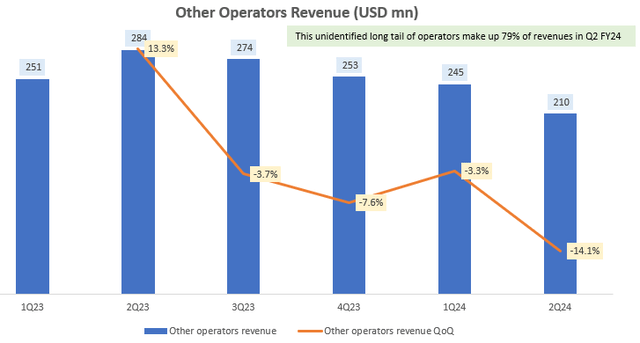

There are indicators of operational weak spot within the broader portfolio as properly

As talked about earlier, Medical Properties Belief’s largest tenants are present process monetary stress. Furthermore, it is also seeing its enterprise relationships flip bitter as MPW is dealing with lawsuits from Steward.

However these points aren’t restricted to the bigger, particular tenants named in MPW’s filings and supplemental disclosures. The enterprise can be seeing YoY revenues decline at an accelerating price, with the remaining lengthy tail of operators making up 79% of complete revenues:

Different Operators Income (USD mn) (Firm Filings, Creator’s Evaluation)

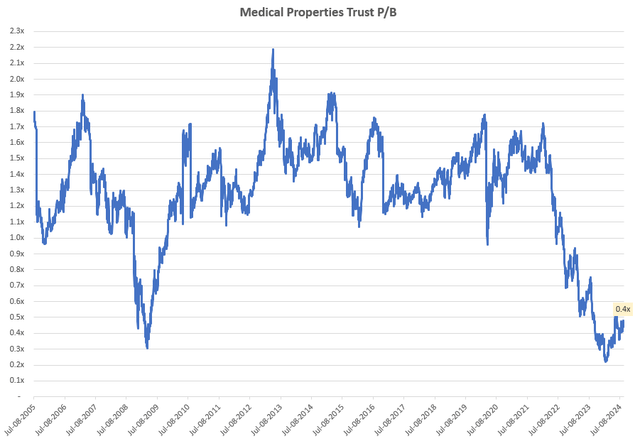

Regardless of buying and selling under guide worth, it’s possible a worth lure

MPW is buying and selling under guide worth at 0.4x P/B. That is even decrease than the 0.7x P/B final yr.

Medical Properties Belief P/B (Capital IQ, Creator’s Evaluation)

Nevertheless, as talked about in my efficiency evaluation reflections at the beginning of this text, with out favorable or at the very least bettering fundamentals, I place much less weight on this decadal low valuation ranges.

Technical Evaluation

If that is your first time studying a Searching Alpha article utilizing Technical Evaluation, you might wish to learn this publish, which explains how and why I learn the charts the way in which I do. All my charts mirror complete shareholder return as they’re adjusted for dividends/distributions.

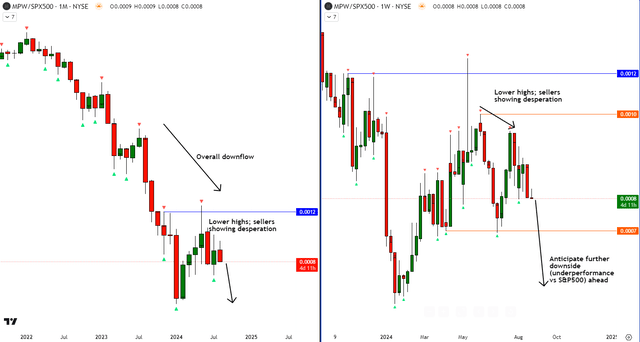

Relative Learn of MPW vs SPX 500

MPW vs SPX500 Technical Evaluation (TradingView, Creator’s Evaluation)

From a relative technical evaluation perspective vs the S&P 500 (SPY) (SPX), MPW inventory stays in an total downward development. On the weekly, we are able to see some indicators of decrease highs, indicating aggression and desperation by the sellers. Therefore, going by the age-old knowledge of ‘do not struggle the development’, I anticipate additional draw back and therefore underperformance vs the S&P 500.

Enhancing tenant fundamentals are a supply of upside danger

A key supply of upside danger, which I imagine could enhance the broader portfolio’s efficiency, is bettering fundamentals in healthcare tenants. There are indicators of this just lately, as healthcare bankruptcies have slowed down, with chapter filings anticipated to be 27% decrease in 2024 vs 2023.

Takeaway & Positioning

My earlier evaluation on Medical Properties belief warned of asset high quality dangers lengthy properly earlier than the blowup within the inventory because of the Steward (largest tenant) chapter. Nevertheless, I erred in ranking the inventory a mere ‘Impartial/Maintain’ as a substitute of a ‘Promote’ for some doubtful causes associated largely to seemingly low valuations, even when the steadiness sheet and operational efficiency of the corporate have been shaky.

Greater than a yr has handed since my final replace on MPW. And my stance right now on the healthcare REIT is a ‘Promote’. I nonetheless see obtrusive operational execution points as a consequence of an FFO money bleed, common impairments, and declining revenues even within the broader portfolio of tenants. On the steadiness sheet facet, I deem the leverage to be excessive and the debt place to be positioned sadly because the excessive and elevated mounted rate of interest debt portion undermines the agency’s potential to profit from upcoming price cuts. Given these weak fundamentals and a bearish learn on the technicals vs the S&P 500, I imagine even a 0.4x P/B valuation is inadequate to stage a real turnaround in MPW.

Tips on how to interpret Searching Alpha’s rankings:

Robust Purchase: Count on the corporate to outperform the S&P 500 on a complete shareholder return foundation, with larger than ordinary confidence. I even have a internet lengthy place within the safety in my private portfolio.

Purchase: Count on the corporate to outperform the S&P 500 on a complete shareholder return foundation

Impartial/maintain: Count on the corporate to carry out in-line with the S&P 500 on a complete shareholder return foundation

Promote: Count on the corporate to underperform the S&P 500 on a complete shareholder return foundation

Robust Promote: Count on the corporate to underperform the S&P 500 on a complete shareholder return foundation, with larger than ordinary confidence

The standard time-horizon for my views is a number of quarters to round a yr. It’s not set in stone. Nevertheless, I’ll share updates on my adjustments in stance in a pinned remark to this text and can also publish a brand new article discussing the explanations for the change in view.

[ad_2]

Source link