[ad_1]

3dfoto/iStock through Getty Photos

MicroStrategy (NASDAQ:MSTR) is a long-lived tech firm that has, in recent times, devoted its focus nearly totally to Bitcoin (BTC-USD). This has earned it a spot in crypto indexes and ETFs. I first got here throughout it whereas analyzing Bitwise Crypto Business Innovators ETF (BITQ), which I lined once more just lately, however I needed to focus extra on MSTR particularly.

One of many few in that fund to report optimistic money flows, it is value taking a look at what it is doing proper and if it is one thing that may be performed reliably for the long run. Total, I discover it to be a C company that capabilities like a managed BTC fund, hoping to generate good returns by means of BTC accumulation and supported by money flows from BTC-related companies.

But, the options of BTC make me marvel if this will reliably produce good, compounding returns to the long-term traders, and so I’ve solely rated MSTR a Maintain.

Bitcoin Growth Firm

Shaped in 1989, MicroStrategy has an extended historical past as a software program developer, even being a kind of infamous Dot Com shares that noticed a meteoric rise and crash through the bubble. Just for the previous couple of years has it leveraged this background right into a concentrate on BTC, and so I am going to reference the working outcomes of that interval.

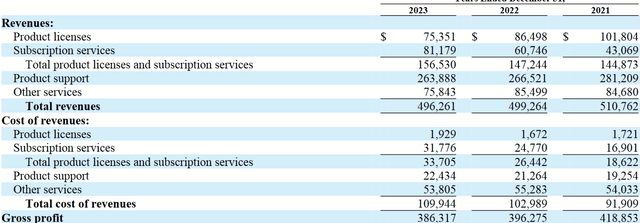

Earnings Assertion (2023 Kind 10K)

Over the past three reporting years, MSTR has had round $500M in income from its numerous strains of software program and associated companies, usually at enticing gross margins.

Earnings Assertion (2023 Kind 10K)

Seen above, their working bills have tended to push them into losses, however this largely owes to the affect of non-cash objects.

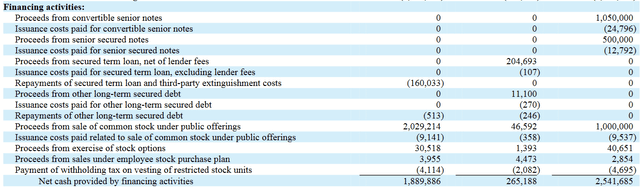

Money Circulation Assertion (2023 Kind 10K)

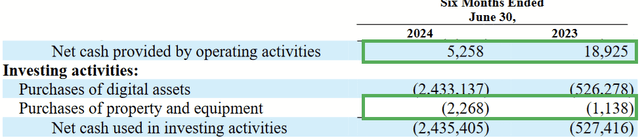

Once we look to the money flows, working money circulate has exceeded capex, producing a optimistic free money circulate within the primary sense. We must always, nevertheless, word the numerous outflow on purchases of BTC (“digital property”).

Money Circulation Assertion (2023 Kind 10K)

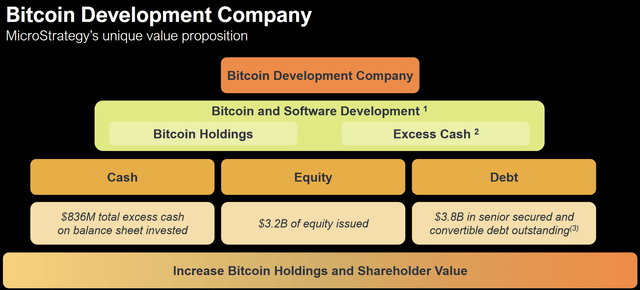

As a “Bitcoin growth firm,” MicroStrategy aspires to be an accumulator of BTC and to be a vendor of software program and companies that can help the event of its mainstream use.

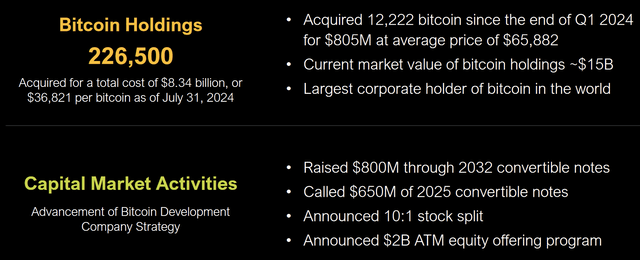

Q2 2024 Firm Presentation

Warren Buffett’s Berkshire Hathaway (BRK.A)/(BRK.B) is a C-corp that makes use of its construction to put money into shares, whereas additionally utilizing the money flows of its wholly owned companies to help this capital allocation. One may say that valuing MSTR requires an analogous strategy to that of BRK: its worth will rely upon one’s appraisal of each the operations and the portfolio. BRK’s portfolio consists of many shares, however MSTR’s is just BTC, a lot of it will rely upon the way forward for the cryptocurrency itself.

BTC Portfolio

The place BTC ETFs enable one to put money into BTC by means of a standard brokerage account, the drawback is within the friction created by their expense ratios that compete towards BTC’s appreciation over time. MSTR believes that it overcomes that drawback with the money from its operations, in addition to a calculated use of financing. Its principal purpose then is to build up BTC at a quicker tempo than it may well dilute frequent shares.

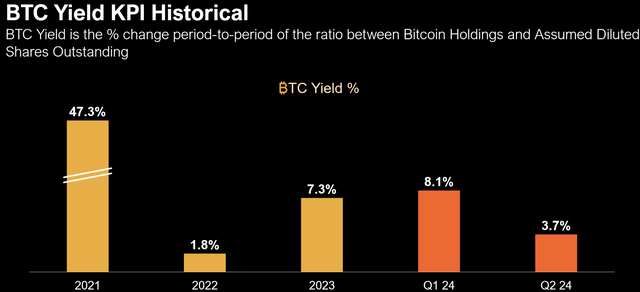

Q2 2024 Firm Presentation

They’ve developed an inner metric known as BTC Yield to precise this, the speed of change between whole BTC holdings and totally diluted shares excellent. A optimistic yield signifies that they need to be creating worth, and the yield has been constantly optimistic up to now.

Q2 2024 Firm Presentation

On the finish of Q2, they reported ₿226.5K, with a mean value foundation of about $36.8K per coin. As the worth of BTC has declined barely since this was reported, they seemingly have one thing round $14 billion in market worth of their portfolio now.

Evaluation of Operations

MSTR’s software program enterprise is not purely BTC-focused, and its offers AI-powered analytics to quite a lot of industries.

Q2 2024 Kind 10Q

Revenues have just lately been in a state of decline, as MicroStatregy is migrating extra clients to its cloud platform, which monetizes on a subscription foundation. The short-term affect subsequently seems to be a discount in income, with potential for larger money circulate in the long run as extra clients convert to the cloud product.

Q2 2024 Kind 10Q

A part of the affect is that working money flows (and thus free money circulate) are a lot decrease for the enterprise, year-over-year. Annualized, that involves about $6M in FCF.

Future Outlook

To be able to worth this enterprise, we have to sift by means of the totally different layers that have an effect on it, such the operations, the portfolio, after which the capital construction.

2022 and 2023 Kinds 10K

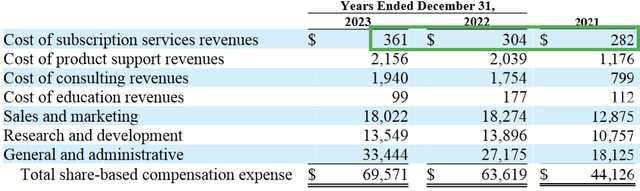

One among my considerations with the software program enterprise is that the price of revenues for the cloud subscriptions are a lot larger than these for product licenses they’re largely changing. Along with the dip in income talked about earlier than, this appears to be the opposite principal cause why working money flows are down from $93.8M in 2021 to an annualized quantity of $6M presently.

Inventory-Based mostly Compensation Historical past (2022 and 2023 Kinds 10K)

Wanting on the final three years, nearly none of this may be attributed to stock-based compensation, and so it seems to be a genuinely costlier product. As AI-powered information analytics have usually proven important demand by enterprises that use them, it is curious why their subscription product is not priced extra aggressively to account for this.

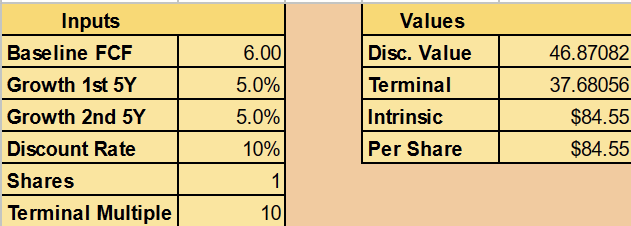

Creator’s calculation

Even when we make optimistic assumptions, that free money circulate will get pleasure from at the least single-digit progress over a decade (regardless of the decreased margins), a Discounted Money Circulation mannequin (priced for a ten% low cost price to match to the market) suggests the intrinsic worth of the software program enterprise is about $84M.

Formidable progress assumptions that enable for FCF to return to 2021 ranges, as if prices may decline/halt because the subscriptions scale out, nonetheless get that into the a whole bunch of tens of millions. Because the BTC portfolio has a market worth of about $14B, whereas MSTR’s market cap exceeds $25B, it is simply clear that the enterprise operations are barely a consideration right here. MSTR’s administration of BTC is what counts.

So why the $11B premium to the BTC holdings? Govt Chairman Michael Saylor defined his ideas to analysts within the Q2 earnings name, stating:

So, when you may have an funding in bitcoin you are not interested by holding it for a brief time period and flipping it. Now, when you consider holding one thing for 30 years, or 40 years, and in case you have a car like a closed-in fund that costs 250 foundation factors as a payment; that appears like a destructive BTC Yield of two.5%. We have now expertise with these form of issues, and we have seen they commerce at a reduction to web asset worth. Closed-in funds with an extended payment on an asset you are going to maintain ceaselessly, they begin to appear like a a number of of the destructive BTC Yield.

Saylor subsequently appears to agree with me that MSTR capabilities like a fund, arguing that the premium is pricing within the worth of the BTC yield.

Referring to Saylor’s comment about treating BTC as an funding asset, it does carry one thing up that offers me pause: the conflicting view on what BTC must be for the long run. Is it an funding asset, or is it a digital foreign money?

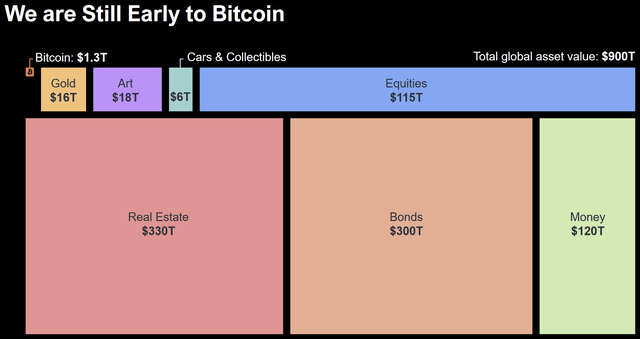

Q2 2024 Firm Presentation

The corporate believes that BTC’s market cap, simply over $1 trillion, has room to understand extra, as international property general are valued at $900T. I am going to word that three of the 4 largest slices (equities, bonds, and actual property) account for property that really produce earnings and money circulate, whereas additionally providing arduous property as extra worth or collateral. BTC lacks both of those qualities.

Gold, artwork, and automobiles/collectibles are additionally arduous property, and to various levels they really have makes use of. Because of this BTC competes most immediately with fiat foreign money, the remaining $120T, as neither present earnings or are something unto themselves, merely currencies. I am going to quote the shareholder letter inside their 2023 Annual Report, which explains their views on the prevalence of BTC:

Now, many have targeted extra on the assumption that Bitcoin is just invaluable as a medium of alternate, and in that case, it’s very simple to say Bitcoin is gradual and never medium of alternate just like the greenback or the euro. Nonetheless, for those who have a look at all of the wealth on the earth as we speak, solely a small proportion of the world’s wealth is saved in instantly accessible mediums of alternate, corresponding to money or checking accounts, and people devices don’t function good shops of worth, significantly in inflationary instances. Subsequently, most wealth is definitely within the type of some higher retailer of worth or helpful capital, corresponding to actual property or shares. In relation to wealth preservation or capital appreciation then, this perception shifts the narrative away from medium of alternate to retailer of worth and from digital foreign money to digital property. Due to its traits, we consider Bitcoin is a superior retailer of worth, akin to digital gold or digital property, and simply as information and CDs gave solution to digital music, we consider gold and different conventional bodily shops of worth will give solution to Bitcoin.

Penned by Saylor, he explicitly disagrees that BTC will perform in the best way that it’s supposed to perform, as a foreign money. He thinks it is higher as a retailer of worth. A part of the issue right here is that so many individuals who maintain BTC accomplish that on the assumption that can displace different fiat currencies. If that does not occur, how does that have an effect on demand and thus the worth? My guess is that it might not be positively.

That is the issue with an asset like BTC. Its recognition is constructed on the simultaneous however typically contradictory views that it may well perform as a foreign money within the short-term and as a retailer of worth within the long-term, though it lacks the traits of both.

Is that this a prediction that BTC will fail and, with it, shares of MSTR? No, nevertheless it does make me query why I would purchase as we speak at nearly an 80% premium to the market worth of the BTC holdings or accept something lower than a GAAP undervaluation.

Q2 2024 Firm Presentation

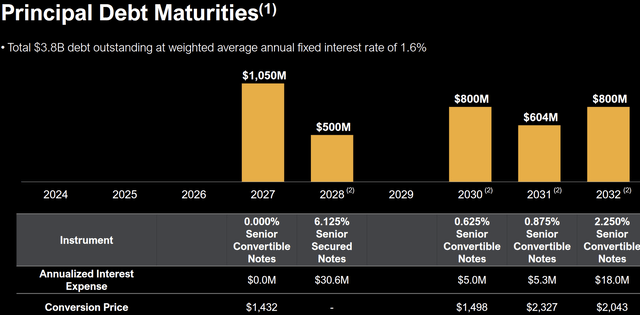

Lastly, let’s take into account the debt available and the way that performs into issues. Practically all of that is convertible debt, with solely the $500M due 2028 of the $3.7B in LT debt on its stability sheet being non-convertible. As the corporate has no downside with issuing fairness, I think that any debt that is not transformed will merely be repaid with extra ATM fairness choices, assuming they can not refinance. Thus, my principal level is that I need to take into account full potential dilution.

Q2 2024 Firm Presentation

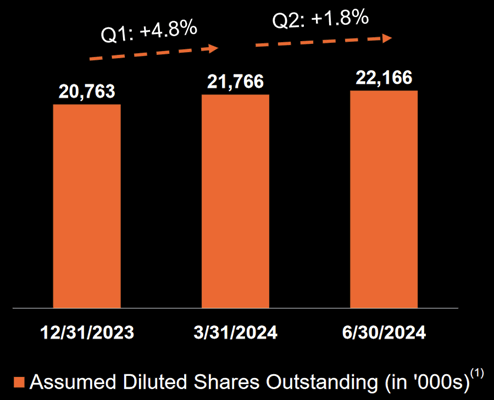

Throughout its Class A shares, Class B shares, and convertible notes, that involves 22,166,000 “assumed diluted shares” as of Q2. After all, if we keep in mind the inventory cut up additionally they introduced, then we have to multiply that by 10.

Whereas MSTR presently trades for about $132 in the marketplace, a good worth for its $14B of BTC could be about $63 per share (if we assume MSTR’s technique can not shut that hole).

Conclusion

MSTR’s market cap over $25B is properly above the worth of the BTC holdings, seemingly across the $14B stage at present costs. Their operations solely generate a number of million in free money circulate annually and are inadequate to plug this worth hole. MSTR’s premium to its BTC holdings subsequently requires confidence that its worth will enhance over the long-term and at a excessive sufficient price to make that premium enticing, together with perception that MSTR can proceed to generate a optimistic BTC yield.

For my part, the corporate fails to ascertain why BTC will reliably carry out as different property do. Shares and bonds have earnings that may compound. Gold and artwork bodily exist and at the least have some utility. Regardless of a increase of AI and the tech to create software program that giant clients can make the most of, that is the trail MicroStrategy has chosen.

Maybe BTC (and MSTR with it) will proceed to understand for a while. But, there’s nothing elementary to the enterprise to require this. In my view, solely a reduction to holdings is smart as an alternative choice to shopping for BTC immediately. With all these uncertainties, I take into account this inventory a Maintain at greatest.

[ad_2]

Source link