[ad_1]

Pornpimone Audkamkong/iStock through Getty Photographs

Inflation could also be crusing towards development, however uncertainties stay on the horizon. Our specialists focus on the components which will influence the economic system and monetary markets within the second half of the yr.

Macroeconomic Outlook

Crusing by means of Uncharted Waters

The macroeconomic backdrop is turning into more and more favorable for G10 bond markets after a tough begin to the yr. Scorching U.S. inflation prints within the first quarter raised doubts in regards to the Federal Reserve’s (Fed’s) potential to chop charges in 2024. Nonetheless, more moderen knowledge exhibits a resumption of the disinflationary development. In the meantime, U.S. development has slowed to a trend-like price, and additional weak spot could also be in retailer because the economic system adjusts to excessive rates of interest and diminished fiscal assist. Total, we count on slower nominal gross home product (‘GDP’) development throughout G10 economies. In flip, this slowdown will allow central banks to decrease coverage charges from restrictive ranges, supporting bond market returns. Nonetheless, whereas it feels as if the macroeconomic ship is now crusing easily towards one thing resembling regular, it is very important do not forget that that is all nonetheless uncharted waters. And farther out, the economic system is headed towards maybe even higher uncertainties. One uncertainty is the shortage of any historic precedent for the present financial cycle and ongoing post-pandemic rebalancing. However one other complicating issue for buyers is the upcoming U.S. election, which has the potential to generate important volatility throughout a variety of asset markets.

One thing Nearer to Regular

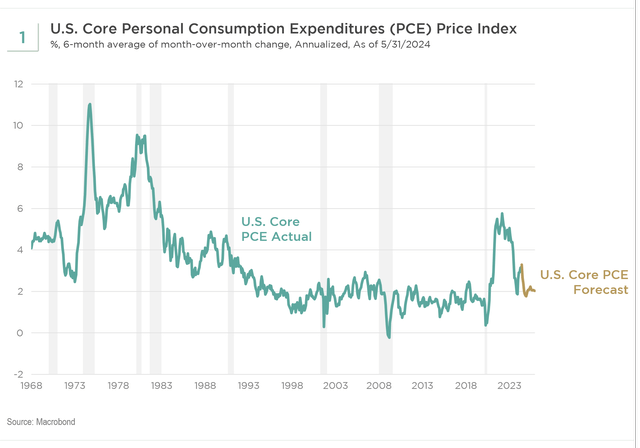

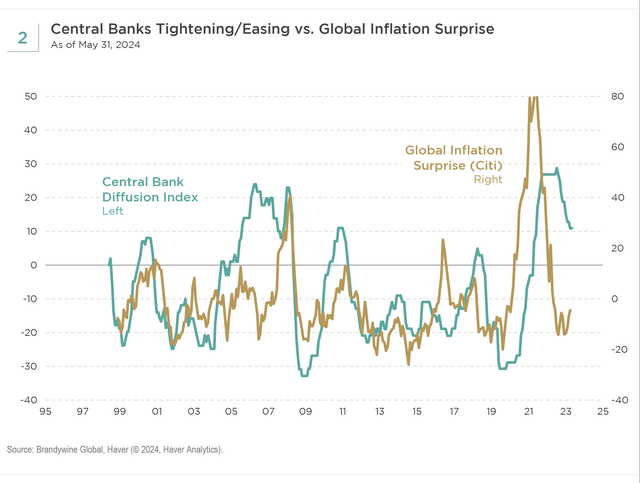

In the course of the previous two years, we have now already made important progress in decreasing inflation (see Exhibit 1). The upside surprises in U.S. inflation throughout the first quarter have been concentrated in service sectors, through which the lags with financial exercise are significantly lengthy. In essence, excessive inflation in these sectors is the results of shocks from two to a few years in the past, fairly than present financial circumstances. Items worth inflation, which responds sooner to present demand/provide imbalances, is already again to its pre-pandemic run price. The unit labor price development price is slowing, reflecting labor market rebalancing and sooner productiveness development. In the meantime, shelter inflation ought to proceed to decelerate within the months forward as a consequence of extra benign market lease traits.

Progress Drivers Rebalancing

We count on some extra moderation in U.S. financial development going ahead in addition to a rebalancing of its relative drivers. Authorities spending and repair consumption have contributed disproportionately to GDP lately. We should always see decrease development contributions from these sectors sooner or later. Financial coverage is restrictive and a headwind to financial development. This tightness is mirrored in very delicate personal sector credit score development, stress throughout industrial actual property markets, rising bank card delinquencies, and weak small enterprise confidence surveys.

It seems that recession dangers are comparatively low at this level, significantly if the Fed cuts charges this yr. Nonetheless, we acknowledge that the present financial cycle is exclusive and with out apparent historic comparisons. In mild of this lack of previous parallels, we stay open-minded about recession dangers and are carefully monitoring financial knowledge. It’s attainable that a big slowdown in service spending along with much less fiscal assist might doubtlessly result in a deeper retrenchment in labor demand and the next unemployment price. The labor market has proven very blended indicators lately, with robust headline employment development contrasted by a rising unemployment price, delicate survey indicators of employment, and falling momentary assist employment. It’s noteworthy that the Fed expects the unemployment price to complete the yr at 4%. Since we’re already at this degree, any additional softening in labor markets might set off a extra aggressive easing cycle.

Eurozone financial development has improved in latest months as falling inflation boosted actual shopper incomes and allowed the European Central Financial institution (‘ECB’) to chop charges. Nonetheless, the upcoming French elections have launched a big ingredient of political uncertainty going into the second half of 2024. Within the occasion of a divided authorities, the broader financial influence on the eurozone is more likely to be comparatively short-lived. Nonetheless, if the Nationwide Rally (‘RN’) occasion wins an outright majority, that might result in a sustained enhance in sovereign danger premiums throughout the eurozone, undermining latest financial development enhancements.

With inflation moderating throughout developed market economies, central banks within the eurozone, Canada, Sweden, and Switzerland have already minimize coverage charges. The Fed is priced for 160 foundation factors (‘bps’) of price cuts over the subsequent 3 years. If our inflation view is correct—that’s, inflation ought to proceed to reasonable as lagging service parts catch as much as items worth disinflation—the Fed ought to have the ability to ship what’s priced into the cash market curve, beginning with two 25bps cuts later this yr. It is vitally unlikely that the Fed might want to hike charges once more on this financial cycle. However we might see plenty of situations through which coverage charges are minimize extra aggressively than what’s priced in. Within the occasion of a deeper slowdown in development or a big sell-off in dangerous belongings, bonds provide a beautiful asymmetry and portfolio safety.

Electing a Cautious Strategy

Latest elections in Mexico, South Africa, India, and the European Union brought on giant bouts of market volatility. And November might carry even larger disruptions. The U.S. elections in November might have main implications for fiscal coverage, commerce coverage, and worldwide relations. For instance, wanting on the large scope of potential commerce implications, if all of Donald Trump’s commerce coverage proposals are carried out, U.S. tariffs would attain their highest ranges because the Nineteen Thirties. Granted, it’s onerous to know the way a lot is marketing campaign rhetoric or what the timing of any proposed commerce restrictions may be. Nonetheless, even when half of the present proposals are carried out, 70 years of U.S. commerce liberalization shall be reversed. It is vitally tough to estimate the influence of such a big coverage shift on monetary markets. So, whereas moderating inflation and development could really feel constructive now, within the second half of the yr markets will shift their focus from the timing of the Fed’s first minimize to election polling. In some unspecified time in the future, a extra conservative strategy to place sizing shall be warranted due to the potential for giant market shocks within the fourth quarter.

Developed Markets Mounted Revenue Outlook

Yr of the Coupon Continues

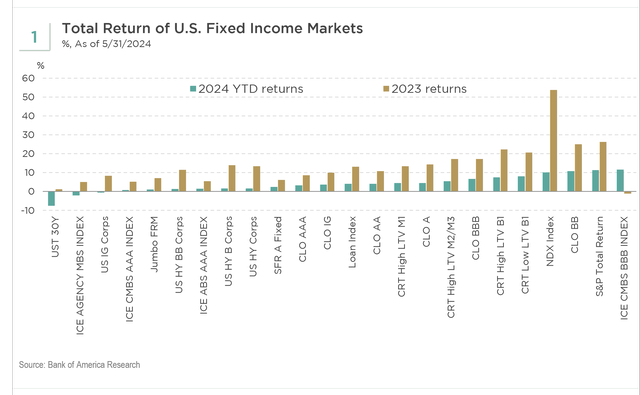

World bonds have mean-reverted to a extra traditionally regular atmosphere (see Exhibit 1). The short take is that earnings in mounted earnings is again to being a driver of efficiency.

Preserving the story easy in an more and more difficult world, developed market bonds provide each earnings and worth. Nonetheless, it’s U.S. Treasuries which have our consideration as we imagine they’ll present management going ahead.

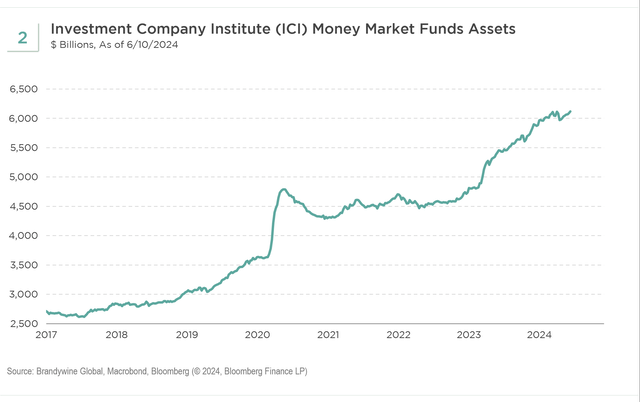

In the course of the second half of 2024, the time shall be proper to maneuver out of money and to place farther out on the Treasury curve, in our view. For the reason that subsequent transfer by the Federal Reserve (‘Fed’) shall be to chop charges, a few of that over $6 trillion in cash market funds will grow to be a supply of funding for U.S. Treasuries (see Exhibit 2). These funds probably should not going into equities given stretched valuations. The “unknowns” are the timing of Fed price cuts and their magnitude. For now, the Fed thinks it’ll take a nuanced strategy and nudge charges decrease, extra so in 2025 than 2024. Historical past exhibits this isn’t the norm. Sometimes, there’s a “disaster” through which one thing is breaking, and that turns into the explanation for the Fed to chop extra aggressively.

We just like the return potential of longer-dated U.S. Treasuries. In step with our name that 2024 shall be one other yr of the coupon in mounted earnings, Treasuries pay a beautiful coupon, and in contrast to money, time is in your facet. Moreover, longer-dated Treasuries have a “kicker” of potential worth appreciation when the Fed is pressured to chop extra aggressively.

So, what’s going to drive the Fed to behave extra forcefully? If it comes right down to just one financial knowledge level, preliminary/persevering with jobless claims within the U.S. could be the sequence that warrants watching. Latest claims knowledge level to an acceleration in labor market deterioration, which confirms the rise within the unemployment price that has been unfolding for months. The Fed has emphasised the labor market’s significance, much more than inflation, and stays delicate to shifts within the jobs knowledge.

A method to consider longer maturity bonds, i.e., 10- to 30-year, is as a low-cost insurance coverage coverage on one thing going fallacious with the economic system. In two out of three situations—the Consumed maintain or the Fed reducing charges—U.S. Treasuries will provide optimistic returns. The one situation through which they won’t work is the fat-tail occasion, which means an occasion that isn’t anticipated and seen as extremely unlikely, of a robust rebound in financial development and a restoration in inflation. That’s the situation the place the subsequent transfer by the Fed is to hike charges, however it isn’t our base case. It additionally could be painful for bonds. One other danger that might be painful for the bond market could be a sweep by both occasion within the upcoming U.S. election. Relying on the occasion, a sweep probably means both extra spending or extra tax cuts, which might not be good for developed market bonds and U.S. Treasuries specifically.

Within the U.S., there are two high-level components we should monitor in analyzing our bullish Treasury bond thesis.

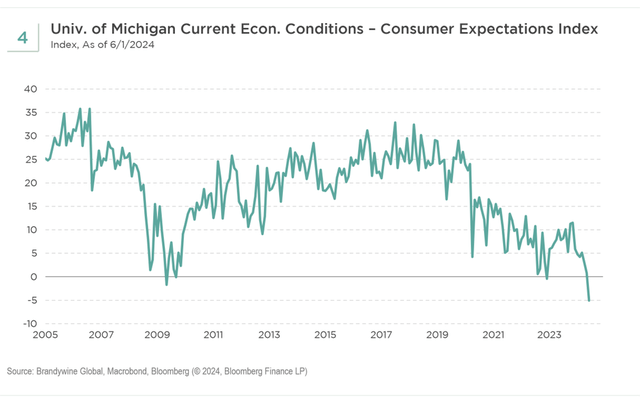

The primary issue is the extra easy one. We shall be monitoring the general financial backdrop for developments in development and inflation dynamics in addition to market atmosphere components. These are a few of the extra vital ones: Demand for U.S. Treasuries: This dynamic has clearly shifted. Latest auctions of longer-maturity Treasuries have been met with stellar demand, marking a significant shift in sentiment across the Treasury complicated. It isn’t that provide is shrinking, however demand influenced by weaker financial fundamentals has a stronger affect than endless Treasury provide. Moreover, there needs to be much less competitors from company bonds as provide is anticipated to sluggish within the second half of the yr. Peak immigration within the U.S.: Immigration declines underneath each a Biden or Trump administration may have a labor influence and should detract from development in a significant means. Falling inflation: Inflation continues to grind decrease, evidenced by Might CPI and PPI, and the sources of decrease inflation are growing (see Exhibit 3). The final main supply of decrease inflation will come from housing, which is a lagging indicator, however we are going to most likely want weak spot within the labor market because the catalyst. Decrease oil and commodity costs additionally assist, together with by unwinding the frothy lengthy positions from the speculative hedge fund group. Bear in mind, inflation has come down sharply with no important financial slowdown—but. What occurs if we get a slowdown? Inflation will soften decrease. For now, the course of inflation is extra vital than the extent of inflation. Inflation expectations are nonetheless nicely anchored. Bifurcated economic system: Decrease earnings, non-asset proudly owning customers are feeling extra stress relative to greater earnings, asset house owners. The identical is true within the company sector. Massive firms versus small companies exhibit the identical bifurcation in efficiency on this economic system. This divergence shouldn’t be sustainable. Fairness market warning indicators: Underlying dynamics within the fairness market are cautionary—a possible detrimental wealth influence. The underperformance of cyclical shares might be a barometer for international financial development. Be looking out for a divergence in shares and bonds, which can sign a shift within the anticipated delicate touchdown turning right into a more durable touchdown. Bear in mind, on plenty of ranges bonds are undervalued relative to equities. Fiscal coverage: Relative to 2023, the U.S. has probably reached the height of fiscal lodging. The U.S. federal authorities can’t keep on its present fiscal path with out risking political instability. Curiosity prices will proceed to crowd out needed spending, e.g., protection. The second issue is more durable to amount. It pertains to election volatility and the “shades of grey influences” we might see in financial knowledge and markets within the second half of 2024. Financial knowledge may not give its regular sign to markets as it might be influenced by the election cycle. This definitely might be the case within the U.S., and it might have already began. The chart beneath highlights the uncommon occasion when present circumstances within the College of Michigan survey are beneath the anticipated shopper confidence studying (see Exhibit 4). Our tackle this improvement is that this yr’s election cycle, whether or not warranted or not, is already having an influence on the U.S. shopper and, by default, the company sector. There have been sufficient election surprises globally thus far that 2024 might be dubbed “The yr of the election.” Market volatility has elevated consequently, however elections like these in France and Mexico could also be only a precursor of the potential election-induced volatility that’s but to unfold. As we head into the second half of the yr, the “Granddaddy” of 2024 elections—the U.S. election—will seize the markets’ consideration. Within the case of France, if political developments don’t result in a “Frexit,” a hypothetical withdrawal of France from the EU, we count on a reconvergence of normality within the OAT market. In Mexico, President-elect Claudia Sheinbaum has despatched optimistic messages round persevering with outgoing President Andrés Manuel López Obrador’s path of fiscal accountability. Within the U.S., we count on election-induced market volatility to start out earlier this yr than typical. Our base case is that we get a divided authorities irrespective of who wins the White Home. That might be the best-case situation for markets. A divided authorities curtails new main spending applications and tax cuts. There’s not a clear-cut hedge towards election volatility apart from taking smaller positions than regular to raised stand up to the value strikes. Polls haven’t been correct up to now elections, and there’s no purpose to count on this one shall be completely different. There are a number of different developments to observe within the developed markets bond area in second half of 2024. Nonetheless, one theme that can persist is that knowledge will proceed to be extra vital than central financial institution rhetoric.

Japan: The Financial institution of Japan (BOJ) wants a definitive plan to deal with inflation issues, fairly than a “plan to have a plan.” Markets hate the uncertainty. We’d keep away from Japanese authorities bonds as their pure purchaser, the BOJ, is in retrench mode.

Eurozone: The eurozone can’t get out of its personal means. Latest developments in France remind the markets it isn’t actually a unified foreign money bloc however 20 particular person international locations, which in flip are a subset of the 27 that make up the EU. European bonds usually commerce costly to U.S. Treasuries. The larger change in info within the second half shall be relative to the slowdown within the U.S. economic system and whether or not the Fed follows after which leads the European Central Financial institution (ECB) in price cuts. In that case, Treasuries ought to outperform their European counterparts.

UK: The UK may need moved into the lead of secure international locations, on a relative foundation. Gilts ought to outperform core eurozone bonds within the second half. Spreads versus German debt look enticing.

China: We nonetheless view China as a supply of worldwide deflation that’s attempting to export its means out of financial malaise. A structural situation of an excessive amount of leverage and never sufficient development to assist it factors towards additional deflation.

I nonetheless imagine the remainder of 2024 will proceed to be the yr of the coupon. Developed market bonds have worth as a result of the coupon is now significant. One caveat, buyers ought to count on to endure an uptick in volatility within the second half, as markets focus extra on the political panorama than on the financial one.

World Currencies Outlook

Decrease Greenback Probably however Election a Threat

The primary half of 2024 was marked by U.S. inflation persistence, driving U.S. rates of interest greater in absolute and relative phrases, which, in flip, supported broad greenback efficiency. Stepping again, within the huge image, most developed market currencies have been vary sure for the previous 18 months, because the starting of 2023. Whereas U.S. financial development outperformed all through 2023, the U.S. greenback has been unable to maneuver greater, restricted by foreign money overvaluation and the dollar’s explicit danger traits.

We stay of the view that U.S. ‘exceptionalism’ over the previous few years was largely a operate of fiscal ‘exceptionalism,’ i.e., the U.S. authorities spent more cash to assist its economic system than some other main economic system. From 2021 by means of 2023, the U.S. greenback benefited from a ‘tight cash/simple fiscal’ mixture. Though the general U.S. fiscal deficit stays important, it’s the change on this deficit—the ‘fiscal impulse’—that issues most for financial development. We anticipate the fiscal impulse will transfer from a big supply of assist in 2023 to a gentle drag on financial development in 2024. With out fiscal assist, the restrictiveness of U.S. financial coverage is more likely to grow to be extra obvious because the yr progresses. Notably, U.S. actual gross home product (GDP) slowed to 2% within the first half of this yr, practically half the tempo recorded within the second half of 2023. The dearth of fiscal stimulus seems to be having a significant influence on the expansion price of total output. Actual GDP development of two% shouldn’t be weak, however together with an extra moderation of employment development and inflation, we count on the slowing of nominal output in 2024 to immediate the Federal Reserve to ease financial coverage over the approaching yr. In flip, we count on this shift in coverage will weaken the greenback.

Rising market currencies usually carried out nicely in 2023 and the primary quarter of 2024, as their greater coverage charges and stronger financial fundamentals attracted capital into their markets. Nonetheless, within the second quarter, plenty of these currencies skilled corrections, partly as a result of valuations modified, rate of interest spreads narrowed, and/or political dangers rose. We diminished publicity to rising market currencies within the first half of 2024. Going ahead, we count on additional upside in rising market foreign money efficiency is probably going restricted to extra choose alternatives.

Lastly, the end result of the U.S. election could influence foreign money efficiency. Present polling is simply too near combine a base situation end result, however usually, the important thing danger is a Republican sweep that permits Trump to pursue additional anti-trade insurance policies and/or pro-growth fiscal insurance policies. Whereas a real mercantilist framework in the end requires a weaker greenback, the president has extra direct management of tariffs than financial coverage. Therefore, the chance is that protectionist insurance policies initially serve to drive the greenback greater.

Rising Markets Outlook

Ahead Actual Yields Level to Choose Alternatives

U.S. inflation persistence early within the yr resulted in greater U.S. charges, a stronger greenback, and volatility in Federal Reserve (Fed) pricing, which has weighed on native rising market (‘EM’) charges and currencies thus far this yr.

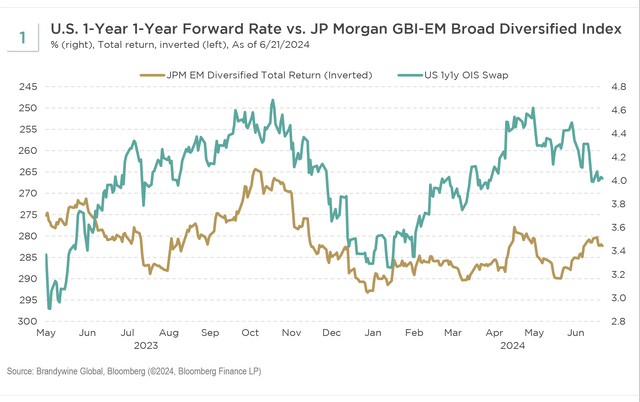

The JP Morgan GBI-EM Diversified Index has been pretty correlated with markets’ pricing of Fed coverage over the previous yr (see Exhibit 1). We noticed a pointy rally beginning on the finish of October 2023 by means of the top of December 2023, with markets accelerating expectations of Fed price cuts. Nonetheless, following a number of higher-than-expected U.S. inflation prints, these anticipated cuts have been shortly eliminated, weighing on the native EM asset class. Regardless of the latest enchancment in Fed pricing, we have now not seen an enchancment in native EM efficiency, which might be associated to apprehensions over U.S. development, native fiscal issues, and election outcomes.

Along with Fed uncertainty, we have now lately seen a deterioration in efficiency, significantly throughout Latin America. This fast deterioration within the efficiency of native markets in Latin America got here on the again of questions round fiscal coverage. For instance, Colombia lately offered its medium-term fiscal framework, displaying a worse-than-expected fiscal deficit for 2024 and 2025. There are issues with fiscal coverage in Brazil along with the longer term composition of the central financial institution towards the top of the yr when President Luiz Inácio Lula da Silva, or Lula, appoints three new board members. With the latest election in Mexico, we are going to see how the federal government will modify fiscal coverage in 2025 from elevated ranges in 2024. Along with potential adjustments in fiscal coverage, markets additionally needed to digest the overwhelming victory by the ruling occasion, Morena. President-elect Claudia Sheinbaum received by over 30%, and her occasion achieved a certified majority within the Chamber of Deputies and an in depth certified majority within the Senate. This end result offers outgoing President Andrés Manuel López Obrador, or AMLO, the prospect to push by means of constitutional adjustments with the brand new Congress in September earlier than Sheinbaum assumes workplace in October. Latin America continues to supply excessive nominal and actual yields relative to historical past, however we should proceed to pay shut consideration to fiscal coverage and home politics.

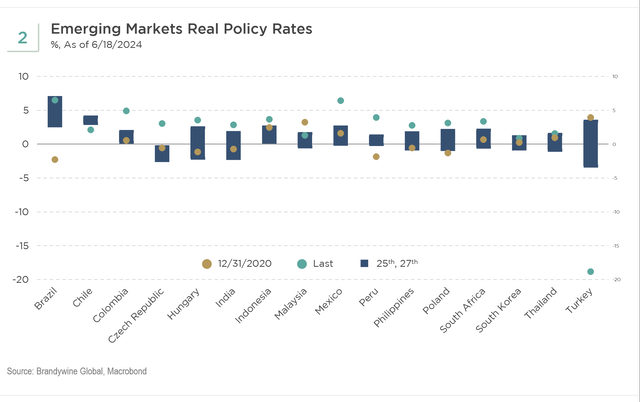

Central and Jap European international locations (‘CEE’) comprise one area with optimistic actual coverage charges above 2% (see Exhibit 2). Disinflation has been a significant theme since final yr, giving central banks the area to chop charges up by means of the primary half of this yr. Given the macroeconomic circumstances for the remainder of the yr, CEE central banks, nonetheless, are more likely to be extra cautious of their rate-cutting cycle, preferring to cut back the tempo of cuts. First, home demand has been choosing up over the previous quarters following nonetheless resilient wage development and financial spending. Second, CEE as a area may gain advantage from a producing rebound as core Europe recovers. Final, international locations corresponding to Hungary and Czech Republic, which have seen weaker currencies within the first half of the yr, at the moment are extra cautious about imported inflation. This concern could result in a slower central financial institution price minimize path for the remainder to the yr.

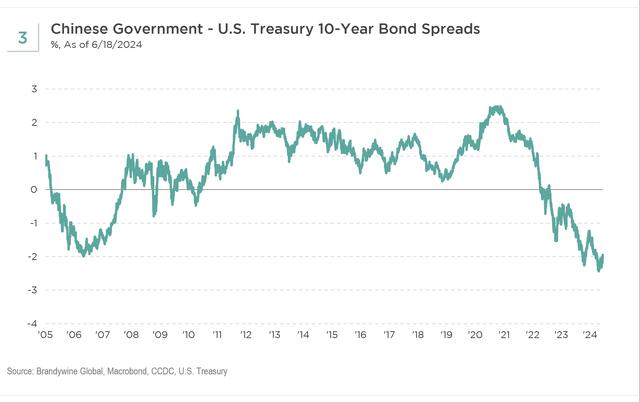

In distinction, Asian bond yields provide low carry and are much less enticing in comparison with Latin America and CEE. This unattractiveness is pushed partly by Chinese language authorities bonds, which have been rallying within the wake of disinflation (see Exhibit 3). Whereas Chinese language policymakers have been supporting the beleaguered property market, and the most recent coverage rescue package deal involving the acquisition of unsold inventories has been encouraging, shopper confidence stays weak. This weak spot has been accompanied by continued deleveraging and downward worth pressures. We imagine China must do extra to carry confidence again to the property market.

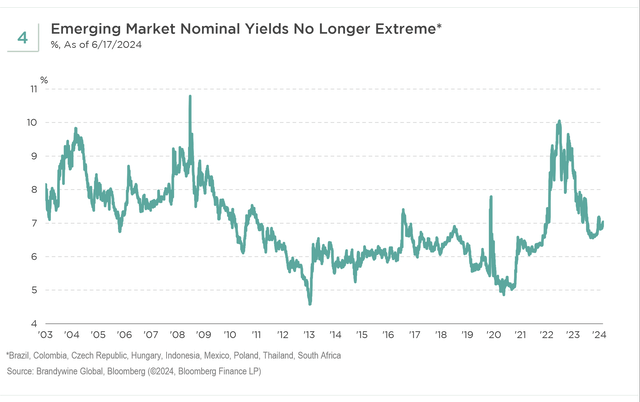

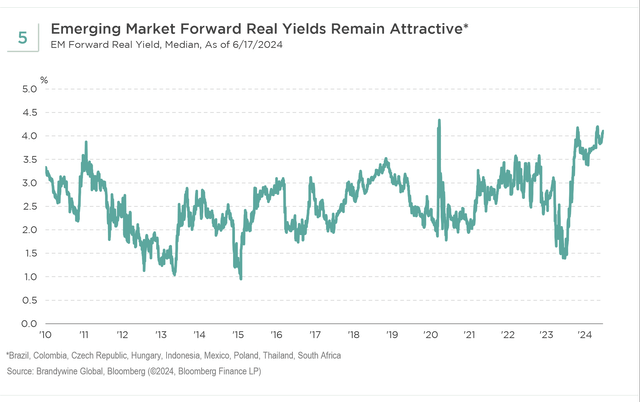

Nominal yields are now not as excessive throughout EM native markets, in comparison with the highs of 2023 (see Exhibit 4). Moreover, spreads relative to U.S. Treasuries are on the tighter finish of their historic vary. Nonetheless, ahead actual yields stay fairly elevated (see Exhibit 5), and we predict there are enticing alternatives that also exist in choose native EM.

Over the approaching months, we shall be watching the Shopper Worth Index (CPI) and labor market knowledge within the U.S.

Can the Fed obtain a delicate touchdown or not? We’re seeing some deterioration in U.S. labor market knowledge that can assist additional declines in wage strain however might weigh on the expansion outlook ought to unemployment speed up greater. A recession within the U.S. would probably be a nasty end result for rising markets. We now have already seen plenty of stunning election outcomes thus far this yr, with the U.S. election nonetheless forward within the coming months. Polls presently present a tie between the 2 candidates; nonetheless, polls haven’t been a great barometer for precise election outcomes. We additionally shall be monitoring developments in China, given the numerous influence on the commodities complicated and development in different EM. In July, the Chinese language authorities will maintain its third plenum. This assembly sometimes coincides with some coverage bulletins, so we’re ready to see if any new coverage updates observe.

Funding Grade Credit score Outlook

Sturdy Fundamentals and Enticing Yields

As buyers, we are likely to look again—after which ahead—at efficiency at sure instances on the calendar. Mid-year occurs to be a kind of instances to evaluate the place markets have been and to ponder what path lies forward for buyers. A lot of the return for funding grade credit score might be defined by the influence of worldwide treasury markets. Persistent energy of assorted international economies pushed the anticipated rate-cutting cycle additional into the longer term, sending yields for a lot of benchmark sovereign bonds greater whereas compressing credit score spreads.

However a slight deterioration in worth throughout the first half of the yr, the macroeconomic atmosphere stays supportive of danger belongings, like company credit score. Moreover, we imagine the person fundamentals stay enticing for funding grade buyers to bear sure dangers of their portfolios. The place to begin of in the present day’s yield is at enticing ranges. With price cuts on the horizon, some buyers could discover shorter-duration funding grade credit a compelling various to money and money equivalents. Many issuers have cheap leverage profiles, and their curiosity burdens usually stay manageable. These robust fundamentals ought to permit for any buyers to take publicity. We’d caveat this view with sure parameters given the world remains to be an unsure place with geopolitical dangers, many doubtlessly disruptive international elections, and financial insurance policies in some international locations, just like the U.S., that seem to stay unchecked.

Our focus could be on publicity within the entrance finish of a capital construction of these credit which have what we might deem to be robust stability sheets. This positioning relies on a view that spreads will proceed to compress, and the credit score curve ought to steepen, supported by continued demand from buyers wanting previous spreads to seize all-in yields which might be at multi-year highs. We’d additionally favor these which might be decrease within the score spectrum, corresponding to BBBs, as opposed to people who are greater rated given the latter are usually buying and selling at unfold ranges that might look like tight at this time limit. Our bias continues to be targeted on vitality, commodities, and financials.

Excessive Yield Credit score Outlook

Optimistic Components Outweigh Tight Spreads

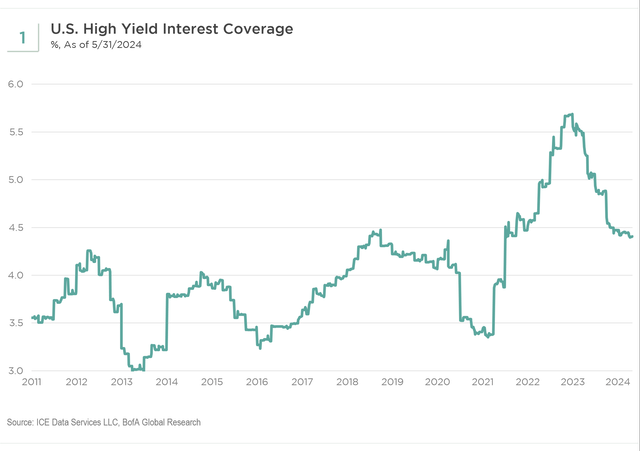

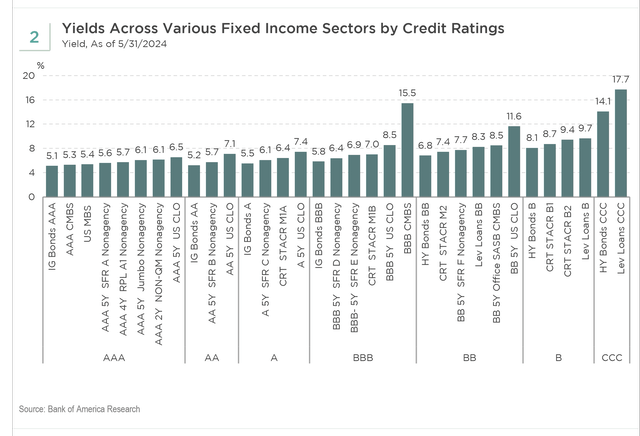

Each the U.S. and international excessive yield markets proceed to profit from a beautiful yield round 8%, low common greenback costs, robust fundamentals, and favorable supply-demand dynamics. The one metric that warrants warning, a diffusion over Treasuries that’s close to the tight finish of the historic vary, should be managed however shouldn’t be, in our view, sufficient to offset the various optimistic components. Within the U.S. market, defaults have stabilized at nicely beneath common ranges since late final yr. Curiosity protection has stabilized at nicely above common ranges whereas leverage ratios stay modest (see Exhibit 1).

The administration groups of excessive yield issuers have had over two years to arrange for greater rates of interest and a attainable recession. And, aside from the 10-15% lowest credit score high quality issuers, they’ve had ample entry to capital, not simply within the excessive yield market however in loans, personal credit score, asset-backed securities, and private and non-private fairness. Excessive yield issuers with publicly traded equities doubtlessly can entry the convertible bond market at practically the identical low rates of interest as in 2020 and 2021 if they’re prepared to surrender a few of the upside on their inventory, which might be at a excessive valuation given the present elevated state of fairness markets.

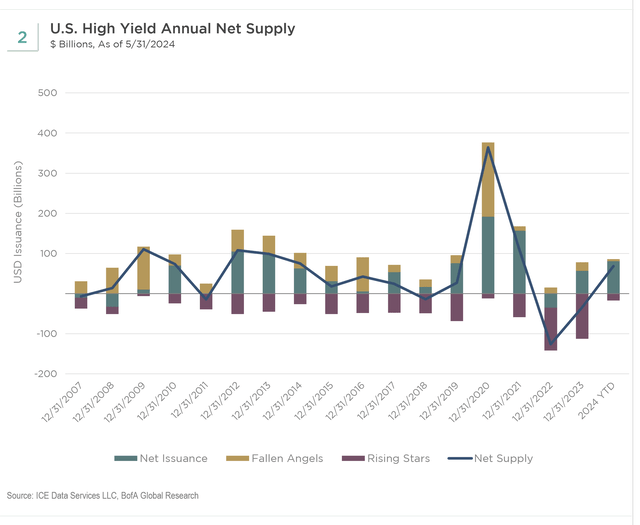

Since 2022, a lot of the new issuance in excessive yield has been used for refinancing. We now have not seen a lot of the dangerous bond buildings or financing of dangerous companies that precipitated main sell-offs in prior excessive yield cycles. Within the U.S. market, a restricted internet new provide (see Exhibit 2) is usually being met with robust international demand for top yield bonds from allocators who perceive these optimistic components and the lengthy historical past of compelling risk-adjusted returns that the asset class has delivered.

For the second half of the yr, we count on the enticing yield and greenback worth, robust fundamentals, and favorable supply-demand dynamics to proceed to result in cheap returns within the U.S. and international excessive yield markets. Any unfold widening could also be the results of decrease authorities bond yields fairly than decrease costs for top yield bonds.

Structured Credit score Outlook

Three Musketeers of Carry, Convexity, and Volatility

Supported by the “excessive for longer” rate of interest atmosphere, strong housing fundamentals, wholesome family stability sheets, and benign credit score fundamentals, high-yielding floating-rate sectors like credit score danger transfers (‘CRT’) and collateralized mortgage obligations (CLO) have outperformed most credit score sectors yr thus far in 2024. Business mortgage-backed securities (‘CMBS’) BBB tranches shone as nicely as a consequence of distressed valuations and extra certainty within the Federal Reserve’s rate of interest path (see Exhibit 1).

Trying ahead to the second half of the yr, we imagine the underlying components described above proceed to carry. We see recession unlikely this yr with peak rates of interest looming. Credit score spreads throughout the structured credit score market usually nonetheless have room to tighten regardless of the rally thus far. We see enticing alternatives within the following sectors, which we imagine provide good relative worth with excessive all-in yields (see Exhibit 2), backed by strong credit score fundamentals and a good market technical. They’re additional supported by the tailwinds of fine carry, optimistic convexity, and decrease price volatility.

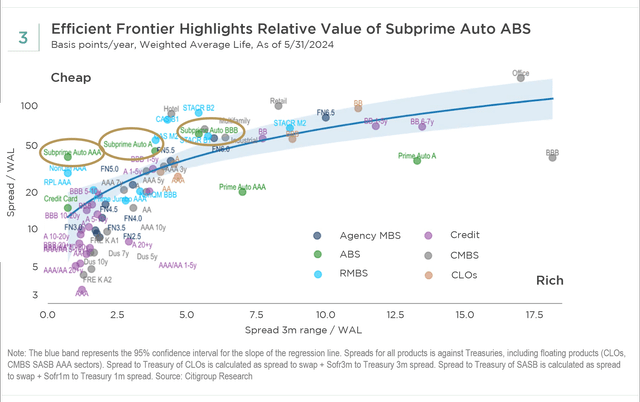

Excessive-yielding floaters, like CRT and CLO, present good carry with excessive all-in yields. Additionally they are an amazing hedge towards price volatility, in our view: Authorities-sponsored enterprises (GSE), like Fannie Mae and Freddie Mac, have been and can proceed tendering excellent CRT bonds with premiums above market costs. When buyers must reinvest these proceeds, it ought to create a good market technical. The dearth of issuance of non-investment grade (‘IG’) tranches and steady score upgrades additionally creates shortage worth for non-IG mezzanine tranches within the secondary market. Underlying efficiency ought to keep strong given the tight job market, important residence fairness accumulation, and first rate housing worth appreciation. CLO BBB and BB mezzanine tranches present good worth with excessive all-in yield and nonetheless benign credit score efficiency. The growing creation of CLO exchange-traded funds (ETFs) boosts demand and liquidity for CLOs. The credit score assist of bonds with BBB or BB high quality scores ought to stand up to reasonable credit score stresses. Unfold ranges on CLO stay elevated in comparison with company credit score counterparts, offering room for convergence. Company mortgage-backed securities (‘MBS’) provide enticing valuations, an amazing convexity profile, and potential financial institution and insurance coverage shopping for sooner or later. Because of the lock-in impact, convexity on company MBS ought to keep in optimistic territory, unprecedented in historical past. The unfold of present coupon company MBS relative to 7- to 10-year Treasuries is hovering above 140 foundation factors, representing one commonplace deviations of cheapness in its 10-year historical past. The unfold between IG company and MBS option-adjusted unfold (‘OAS’) is at historic tights, indicating the latter is affordable. We imagine the MBS unfold to Treasuries ought to tighten as a consequence of declining rate of interest volatility and enhancing demand from cash managers, banks, and insurance coverage firms. We want manufacturing coupon company MBS as they provide the most cost effective unfold with reasonable period. CMBS new situation versus the secondary market represents a story of two worlds. The underwriting requirements for the brand new situation market have tightened considerably, providing much less publicity to the troubled workplace sector, decrease leverage, and shorter period. Spreads on BBB tranches have tightened considerably because the starting of the yr. Alternatively, a whole lot of dangerous information within the workplace sector is being step by step priced into secondary market offers, offering upside alternatives with the correct credit score choice. There are many different property varieties which might be doing nicely and supply worth, too. GSE multi-family CRT is an instance of a sector that we like. Asset-backed securities (ABS) on the buyer facet, corresponding to subprime auto ABS with adequate credit score safety, are nonetheless enticing given the quick period and quick delevering construction (see Exhibit 3). On the company ABS facet, we see attention-grabbing alternatives in entire enterprise securitization, knowledge middle, and fiber ABS from established issuers. A number of provide cheaper valuations, rising enterprise prospects, nice scalability of dimension, and strong period alternative with IG scores.

Trying into the second half of the yr, we see the next traits impacting fundamentals throughout the structured credit score market.

Housing fundamentals nonetheless strong

Mortgage charges within the U.S. elevated to the low-to-mid-7% vary within the first half of 2024. Listings for each new residence gross sales and present residence gross sales elevated. Nonetheless, provide stays comparatively low with housing shortages supporting housing costs. We imagine residence worth appreciation will keep within the low-to-mid single digits in 2024.

Wholesome family stability sheets

Credit score fundamentals are returning to pre-COVID ranges as customers spend their elevated financial savings, constructed up from the beneficiant stimulus packages and huge wealth results as a consequence of rising asset costs. Shopper wellbeing is a bifurcated story of internet asset house owners versus internet debt debtors. The previous are principally child boomers who benefited from asset worth inflation, greater curiosity earnings, and fewer debt. The latter, who’re principally youthful or lower-income cohorts, are feeling the squeeze of upper shopper debt with greater charges. Nonetheless, the job market remains to be first rate and child boomers nonetheless dominate the macro shopper story for now.

Business actual property market woes

The reckoning of the workplace sector shall be an extended, drawn-out course of which will final a number of years. Market sentiment ought to step by step backside with rates of interest peaking. The extensive CMBS unfold pickup relative to company bonds supplies unfold compression potential. We imagine the latest incident of a AAA-rated CMBS deal taking losses shouldn’t be an remoted occasion. Consequently, we count on to see extra capitulation and worth discovery, which is part of the bottoming course of.

Increased CLO tail dangers

The latest high-profile Altice credit standing downgrade highlighted the growing tail dangers within the leveraged mortgage area. Nonetheless, the CLO market has been resilient as a consequence of sturdy deal buildings and different components. As well as, the floating price nature of CLO belongings ought to proceed to supply hedges towards period dangers.

Favorable market technical

Lowered internet new issuance and still-high demand throughout many sectors are buoying the market technical.

Abstract

Beneficiant carry, optimistic convexity, and decrease price volatility together with good worth relative to company credit score sectors are tailwinds for structured credit score markets. We imagine excessive yield floaters, like CRT and CLO BBB/BBs, manufacturing coupon company MBS, and sure pockets of CMBS and ABS, provide nice worth in within the second half of 2024.

World Equities Outlook

Alternatives and Catalysts throughout the World Funding Panorama

In our relentless pursuit of funding alternatives throughout the worldwide canvas, a number of compelling themes have captured our consideration.

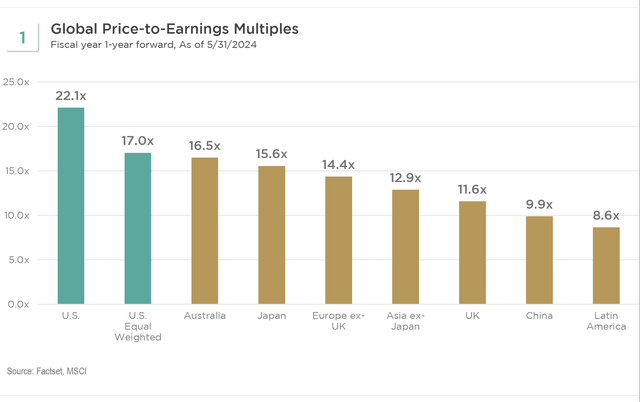

The premium valuation of U.S. shares in comparison with different markets worldwide is strikingly obvious (see Exhibit 1). A worldwide financial easing cycle has commenced, led by rising markets (see Exhibit 2). Latin America has already begun reducing rates of interest, whereas Canada and Europe have lately adopted swimsuit. We count on others to observe shortly, with the U.S. now more likely to lag. These areas provide catalyst-rich environments poised to profit from a reversal in central financial institution coverage. Latin American industrial actual property and UK housing are two sectors that seem extremely enticing to us as clear beneficiaries of falling rates of interest. The U.S. tech and web sector continues to dominate the worldwide benchmark, although a few of the largest gamers are experiencing setbacks this yr. We now have owned a few of these names earlier than when valuations have been favorable, however presently our macroeconomic analysis, coupled with a value-oriented mindset, means that there are way more compelling alternatives worldwide than merely investing in what everybody else already owns. Often, we establish {industry} catalysts with international implications. Our present favourite instance is the worldwide scarcity of economic plane ensuing from Boeing’s 5 years of manufacturing points. House owners of this more and more scarce asset, whether or not they’re airways in any area of the world or the biggest plane lessors, commerce at single-digit price-to-earnings (P/E) ratios. Fundamental provide and demand economics means that pricing is more likely to be fairly favorable transferring ahead.

As international buyers, we have now entry to the broadest attainable fairness alternative set, enabling us to attain important diversification whereas focusing on catalysts, whether or not they’re macro or industry-specific. An successfully executed international technique ought to all the time have a number of methods to win, in our view. Given the various geopolitical uncertainties and dangers within the second half of the yr, together with a U.S. election with the potential to generate extreme volatility in monetary markets, our broad mandate offers us the pliability to doubtlessly sidestep sure obstacles whereas capitalizing on alternatives created by diverging international financial coverage and financial cycles.

U.S. Equities Outlook

Worth Will Have Its Day

For a lot of the first half, the U.S. economic system has been surprisingly robust. In the meantime, inflation has been extra cussed, staying above 3%, than markets appeared to count on. Because of this, expectations for Federal Reserve price cuts have come down dramatically. Up so far, the Elementary Fairness staff has been within the “greater for longer” camp on each inflation and rates of interest. Nonetheless, as of mid-year, our view is beginning to evolve as indicators of financial slowing lastly could also be choosing up with preliminary unemployment claims up 20% from ranges early within the yr. Whereas this improvement doesn’t essentially sign an imminent recession fairly but, we imagine the pendulum could begin to swing again towards the market anticipating extra short-term price cuts. As we have now emphasised repeatedly, historic indicators recommend an inevitable recession, even when the timing has been tough.

One thriller has been that the broad market indexes, pushed by the massive weights of the “Magnificent Seven”—or Three or 4, relying on the day—have largely shrugged off most issues as AI-driven pleasure spreads to different components of the expertise chain. We nonetheless see dangers to market valuations and have leaned into a comparatively defensive publicity in comparison with our historical past. The present situation shouldn’t be fairly the never-happening Ready for Godot, and we’re sticking to our worth framework regardless of the challenges the model has skilled. We imagine that between a slowing economic system, an unsure election backdrop, and the problem in sustaining tech hype endlessly, worth may have its day.

View all Index Definitions.

Disclosure

Financial and market forecasts offered herein replicate a sequence of assumptions and judgments as of the date of this materials and are topic to alter with out discover. These forecasts don’t bear in mind the particular funding goals, restrictions, tax and monetary state of affairs or different wants of any particular shopper. Precise knowledge will differ and will not be mirrored herein. These forecasts are topic to excessive ranges of uncertainty that may have an effect on precise efficiency. Accordingly, these forecasts needs to be seen as merely consultant of a broad vary of attainable outcomes. These forecasts are estimated, primarily based on assumptions, and are topic to important revision and should change materially as financial and market circumstances change. Sure info or statements contained herein could represent a forward-looking assertion. Ahead- wanting statements are predictive in nature and communicate solely as of the date they have been made. Brandywine World assumes no responsibility to and doesn’t undertake to replace forward-looking statements. Ahead-looking statements check with future occasions or circumstances and are topic to plenty of assumptions, dangers and uncertainties that might trigger precise outcomes or occasions to vary materially from present expectations. Previous efficiency is not any assure of future outcomes.

Groupthink is dangerous, particularly at funding administration companies. Brandywine World subsequently takes particular care to make sure our company tradition and funding processes assist the articulation of various viewpoints. This weblog is not any completely different. The opinions expressed by our bloggers could generally problem energetic positioning inside a number of of our methods. Every blogger represents one market view amongst many expressed at Brandywine World. Though particular person opinions will differ, our funding course of and macro outlook will stay pushed by a staff strategy.

©2024 Brandywine World Funding Administration, LLC. All Rights Reserved.

Social Media Pointers

Brandywine World Funding Administration, LLC (“Brandywine World”) is an funding adviser registered with the U.S. Securities and Alternate Fee (“SEC”). Brandywine World could use Social Media websites to convey related info concerning portfolio supervisor insights, company info and different content material.

Any content material revealed or views expressed by Brandywine World on any Social Media platform are for informational functions solely and topic to alter primarily based on market and financial circumstances in addition to different components. They aren’t meant as a whole evaluation of each materials truth concerning any nation, area, market, {industry}, funding or technique. This info shouldn’t be thought of a solicitation or a suggestion to supply any Brandywine World service in any jurisdiction the place it could be illegal to take action underneath the legal guidelines of that jurisdiction. Moreover, any views expressed by Brandywine World or its staff shouldn’t be construed as funding recommendation or a suggestion for any particular safety or sector.

Brandywine World will monitor its Social Media pages and any third-party content material or feedback posted on its Social Media pages. Brandywine World reserves the correct to delete any remark or submit that it, in its sole discretion, deems inappropriate or forestall from posting any one that posts inappropriate or offensive content material. Any opinions expressed by individuals submitting feedback do not essentially signify the views of Brandywine World. Brandywine World shouldn’t be affiliated with any of the Social Media websites it makes use of and is, subsequently, not accountable for the content material, phrases of use or privateness or safety insurance policies of such websites. You might be suggested to assessment such phrases and insurance policies.

Click on to enlarge

Unique Submit

Editor’s Observe: The abstract bullets for this text have been chosen by In search of Alpha editors.

[ad_2]

Source link