[ad_1]

littleclie

MSCI (NYSE:MSCI) reported outcomes that have been in step with my base case for the corporate, reaffirming my thesis that the weak spot we noticed within the enterprise within the first quarter was not the beginning of a worsening pattern, however quite, extra of a one-off and short-term prevalence.

Administration demonstrated within the quarter that regardless of the robust market circumstances, MSCI continued to develop solidly, type new partnerships and spend money on its core and new companies.

The ESG & local weather section and personal belongings section are two promising segments, that are within the early levels for MSCI, and the place MSCI has structural benefits on which it could lean on.

Whereas the atmosphere stays troublesome and administration stays cautious, I’m cautiously optimistic that we are going to see the headwinds from 1Q24 slowly dissipate because the yr progresses.

Temporary introduction

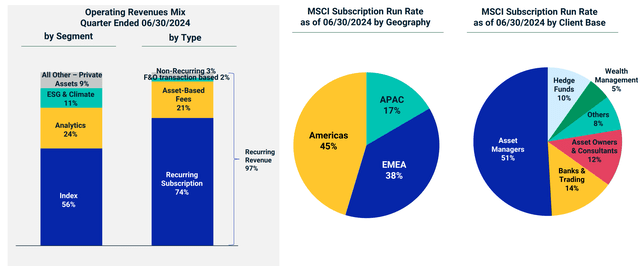

For individuals who are new to the MSCI story, MSCI has three primary segments, the index section makes up 56% of revenues, analytics section makes up 24% of revenues and ESG & Local weather makes up 11% of revenues.

By consumer base, asset managers, hedge funds, asset homeowners and banks have historically shaped the majority of its enterprise. MSCI has been specializing in a brand new group of consumer segments with robust potential, together with insurance coverage firms, wealth managers, common companions, corporates and company advisers.

Income and consumer combine (MSCI)

2Q24 outcomes

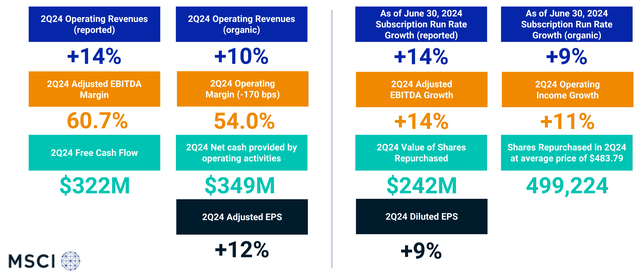

Revenues got here in at $708 million, up 14% from the prior yr (Beat consensus by 2%).

Working revenue got here in at $385 million, up 11% from the prior yr (Beat consensus by 4%).

EPS got here in at $3.64, up 11% from the prior yr (Beat consensus by 4%).

Outcomes overview (MSCI)

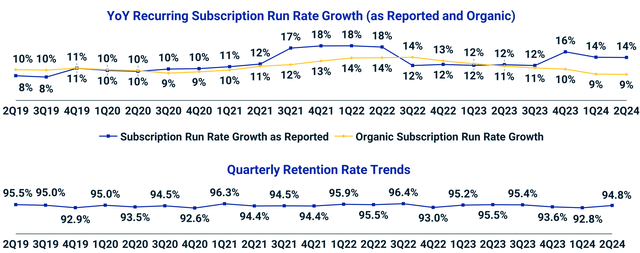

Most significantly, as might be seen under, the retention ratio shortly recovered to 94.8%, which is round its common retention ratio, after the metric fell to 92.8% in 1Q24.

This helped relieve fears that we may see additional deterioration after the 1Q24 weak spot as a result of retention ratios rebounded instantly as I initially anticipated.

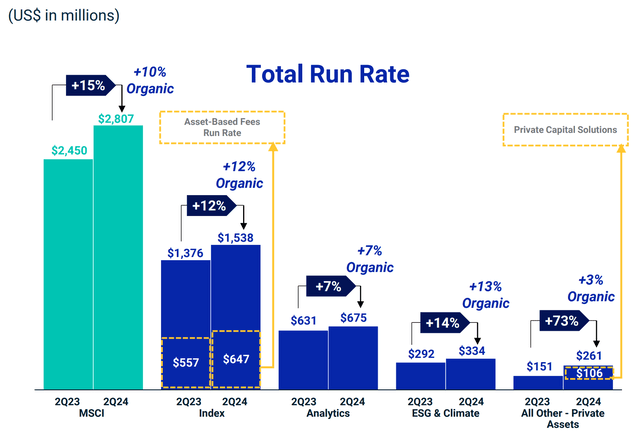

Run-rate and retention ratio (MSCI)

Index section

The index section subscription run charge progress got here in at 9%.

By geography, each EMEA and APAC contributed 10% progress in subscription charge progress in index.

By consumer base, the 2 extra vital index consumer segments which make up 68% of index subscription run charge, asset managers and asset homeowners, grew at 8% and 12% respectively. The hedge funds and wealth managers section noticed their index subscription run charge develop 24% and 11% respectively.

By merchandise or modules, the customized indexes and particular package deal section grew 17% from the prior yr. Particularly, in 2Q24, MSCI helped a big asset supervisor consumer launch a brand new customized ETF local weather collection linked to the MSCI Transition Conscious Choose indexes. As well as, MSCI closed the Foxberry acquisition, which is able to result in an enhanced customized index platform launch within the second half of 2024.

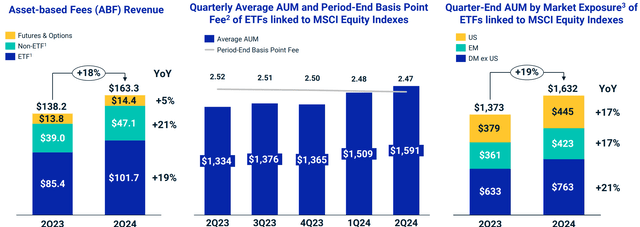

Asset-based charges grew 18% from the prior yr, benefiting from a rise in AUM by 19% from the prior yr, and within the quarter, MSCI noticed $28 billion money inflows into MSCI-linked fairness ETFs and $21 billion in market appreciation within the second quarter.

Index section metrics (MSCI)

Particularly, ETF merchandise linked to MSCI indexes proceed to develop, which strengthened MSCI’s place as a prime index for ETF merchandise, with the variety of fairness ETFs linked to MSCI indexes doubling from the prior yr. This introduced in $2.5 billion in money flows and represents virtually 30% market share within the new fairness ETF fund flows.

Analytics, ESG and Local weather and Personal Belongings

Relative to the dimensions of the index section, the analytics, ESG & local weather, and personal belongings segments when mixed is smaller than the index section, however they do deliver some distinctive traits and diversification to the enterprise mannequin.

Run charge breakdown (MSCI)

First, within the analytics section, natural subscription run charge progress was 7% and income progress for the section was 11%. Analytics achieved new recurring subscription revenues of greater than $21 million, which was the very best ever second quarter achieved and likewise the very best ever retention charge for the second quarter of 96%. This efficiency is a results of a robust quarter with hedge funds, the place MSCI’s fairness threat fashions achieved a big win for a brand new consumer’s latest fund launch. Nearly $4 million in new recurring subscription revenues got here from asset homeowners, which was up 63% from the prior yr, as asset homeowners look to enhance their enterprise threat administration. When it comes to drivers, the robust analytics efficiency was pushed by an atmosphere the place its prospects are more and more specializing in funding threat, credit score threat and liquidity dangers, and MSCI is a pacesetter on these. As well as, one other driver is innovation inside the analytics section, which incorporates delivering threat analytics by means of visualization and integrating AI capabilities inside the enterprise.

Second, within the ESG & local weather section, natural subscription run charge progress was 14% and income progress was 12%. There was additionally a 30% local weather run charge progress. Other than the Moody’s partnership, MSCI continues to launch new merchandise within the ESG & local weather section, with a brand new information set to assist prospects align higher with company sustainability reporting directive in Europe. MSCI additionally launched the MSCI GeoSpatial Asset Intelligence, which has already led to 2 signed offers, considered one of which is with a big non-public credit score common associate. The MSCI GeoSpatial Asset Intelligence product supplies prospects with AI capabilities that may establish bodily and nature-based dangers on greater than 1 million areas for 70,000 private and non-private firms. Administration shared that the preliminary consumer curiosity has been encouraging.

Third, within the non-public belongings section, natural subscription run charge progress was 3% and income progress was 72%. The robust income progress was a results of an acquisition of Burgiss, and excluding the influence of Burgiss, there was a 17% progress within the subscription run charge for personal belongings. The retention charge for personal belongings is at present about 93%

Cautiously optimistic

Provided that 2Q24 outcomes have been encouraging, I’m cautiously optimistic concerning the outlook for MSCI.

Particularly, I do suppose that my base case that the final quarter’s cancellations and weak gross sales efficiency weren’t the beginning of a deteriorating pattern is affirmed.

The truth that we noticed stable progress and rebound in retention charges from the prior quarter was a constructive, and administration additionally commented that there was no deterioration within the present 2Q24 quarter.

That stated, I added the time period cautious there due to administration commentary.

MSCI continues to count on cancels to be elevated in 3Q24 in comparison with the prior yr and that longer gross sales cycles proceed to persist.

In my opinion, this is because of two elements. Firstly, after the one consumer occasion that resulted in $7 million in cancels on account of a merger between two main world banks in Europe, whereas most of that headwind occurred in 1Q24, there are nonetheless some near-term market headwinds from that in 3Q24. Secondly, 3Q24 tends to be a seasonally softer quarter for MSCI.

Roughly $7 million price of cancels got here from a single consumer occasion, a historic merger of two main world banks in Europe that affected us throughout index, ESG and analytics

Administration noticed excessive ranges of consumer engagement world wide in 2Q24. Shoppers have been keen on new areas of collaboration with MSCI. For instance, Moody went right into a strategic partnership with MSCI to deliver MSCI’s sustainability information and fashions to Moody’s purchasers. This can be a win-win partnership that not solely demonstrates how Moody views MSCI as a pacesetter in ESG, however MSCI additionally advantages from this because it will get entry to Moody’s Orbis, which is a personal firm database. That is helpful for MSCI given it has been centered on getting higher information, particularly within the ESG and local weather house, which might be troublesome to acquire, so this partnership advantages MSCI in a number of methods.

As well as, MSCI simply launched MSCI non-public capital closed finish fund indices as purchasers have been requesting for such merchandise and rising investor curiosity in non-public markets. There are 130 of such indexes, constructed from a universe of personal capital funds with greater than $11 trillion in capitalization. This contains every kind of personal belongings, like non-public fairness, non-public credit score, non-public infrastructure, amongst others.

That is an fascinating new alternative for MSCI to give attention to, the place MSCI is uniquely positioned to handle this market and in a position to tackle the technical challenges that others could not have the ability to. The primary one is the $15 trillion of underlying information throughout all non-public belongings, with $11 trillion used to construct the 130 indexes introduced above, and $4 trillion for its different actual asset indices. MSCI has the most important and highest high quality information throughout all gamers, which is a big benefit. The second is the understanding and functionality to grasp the funding course of and metrologies to create indices, the place MSCI clearly has spent many years to construct. The final one is the distribution, the place MSCI as soon as once more has a big consumer base of asset homeowners and managers.

Lastly, as there may be rising consumer curiosity in utilization of AI applied sciences, MSCI launched the MSCI AI Portfolio Insights device, which is a brand new threat product suite that mixes generative AI with superior analytical instruments and modeling capabilities to assist prospects establish dangers.

Administration sees that AI might be carried out within the enterprise to enhance price efficiencies and improve revenues. MSCI is seeing some engaging economics when it comes to how AI might be deployed inside MSCI to drive price efficiencies, and this can be embedded into the budgeting for 2025 specifically. MSCI has additionally seen how AI can assist with new product growth throughout totally different segments and companies.

I believe that robust consumer engagement world wide and throughout consumer segments, together with constructive momentum within the fairness markets, ought to result in momentum within the gross sales entrance.

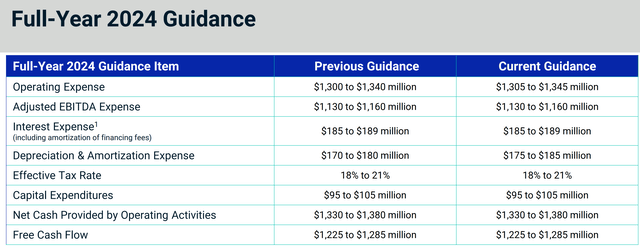

On the steerage entrance, MSCI reiterated a lot of the 2024 steerage, excluding a lower than 0.5% improve in working bills coming from barely increased D&A. This improve got here from an acquired intangible amortization expense from the Foxberry acquisition, which was closed in April.

2024 steerage (MSCI)

Valuation

The 2Q24 outcomes have been a affirmation of my mannequin, with only a modest revision to the working bills line.

One factor that I needed to regulate the mannequin for was the numerous share buybacks that MSCI was doing, which resulted in EPS being revised increased because of the decrease share rely.

There was a 2% discount in share rely for the reason that prior quarter, and I assume a modest 1% discount in share rely every year (MSCI diminished share rely by 1.5% every year on common since 2019).

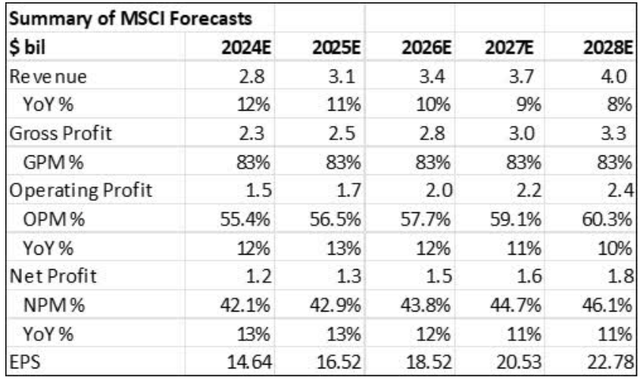

As such, my MSCI 5-year forecasts as proven under. I forecast MSCI’s EPS CAGR to be 11% over the 5-year interval, which relies on assumptions that the cancellation charges don’t worsen from right here and that the macro and market atmosphere stays secure, with continued effectivity enhancements within the enterprise driving working margin enlargement, as proven under:

Abstract of my 5-year monetary forecasts for MSCI (Creator generated)

My intrinsic worth for MSCI is $627, once more utilizing the discounted money circulate mannequin and assuming the 40x terminal a number of and 11% price of fairness. The 40x terminal a number of is affordable right here, given that previously 5 years, MSCI’s 5-year common P/E is 52x. Once I excluded MSCI’s irregular P/E of 71x in 2021, the 5-year common P/E goes all the way down to 46x. As well as, it has a 10-year common P/E of 42x. In consequence, I believe that 40x 2028 P/E is truthful for the corporate based mostly on historic valuations, continued management within the house, and a extremely engaging enterprise mannequin with excessive retention charges and recurring revenues.

My 1-year and 3-year worth targets are $678 and $859 respectively, which suggest 40x 2025 and 2027 P/E. Once more, I believe these multiples are affordable given what was talked about above.

Conclusion

As I’ve urged a number of instances within the article, I believe that the 2Q24 earnings for MSCI ought to assist relieve fears about worsening fundamentals.

Regardless of a troublesome working atmosphere, MSCI continues to excel because the market chief and exhibit the standard of its enterprise mannequin.

The brand new companies through which it’s investing in ought to drive incremental progress sooner or later, whereas its management in its core index enterprise continues to shine.

As we transfer previous the headwinds that we noticed in 1Q24, and because the atmosphere turns into a extra favorable one for MSCI, we are going to probably see the corporate’s investments in innovation and new merchandise ship sustainable long-term progress for the corporate.

[ad_2]

Source link