[ad_1]

eyewave

Funding thesis

Our present funding thesis is:

Nissan is in a turnaround course of, as a number of years of decline go away the enterprise in a despair. Margins are poor and rivals have taken market share. The transformation appears to be like to be sound foundationally, with sturdy car curiosity and innovation underpinning the advance. Nissan’s place within the trade appears to be like engaging. It’s important to additional develop car differentiation and extract higher worth from the Alliance. Relative to friends, Nissan stays unattractive, nonetheless, and its valuation doesn’t present enough upside to make this a worthy valuation.

Firm description

Nissan Motor (OTCPK:NSANY) is a world automotive producer headquartered in Japan. It operates within the automotive trade, producing and promoting a variety of autos, together with passenger vehicles, SUVs, electrical autos, and business autos. The corporate has a presence in numerous areas worldwide and is thought for its widespread manufacturers similar to NISSAN, INFINITI, and Datsun.

Share value

Nissan’s share value has carried out extremely poorly during the last decade, dropping over 50% of its worth, because the enterprise has struggled to take care of its constant monetary efficiency achieved beneath Carlos Ghosn.

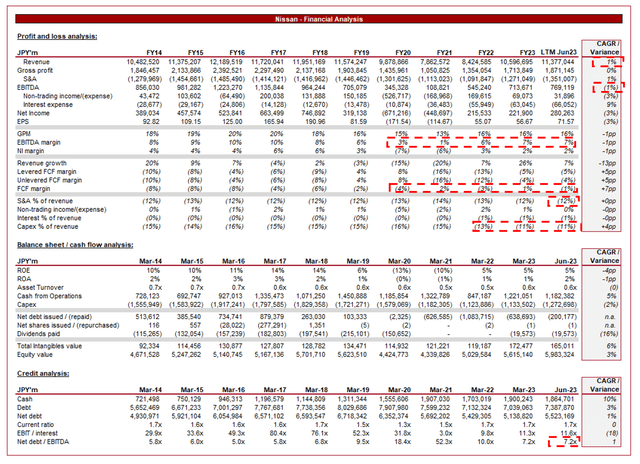

Monetary evaluation

Nissan financials (Capital IQ)

Offered above is Nissan’s monetary efficiency for the final decade.

Income & Industrial Elements

Nissan’s income has grown at a mean price of 1% within the final 10 years, because the enterprise has skilled 4 years of decline in 11 years. The enterprise is materially fighting attaining consistency, creating damaging sentiment across the enterprise.

Enterprise Mannequin

Nissan designs, manufactures, and markets autos by means of its international manufacturing and meeting services. Just like different automotive producers, the corporate has international hubs from which to export its autos into key areas. The corporate sells its autos by means of an intensive community of dealerships and distributors throughout totally different markets.

Nissan’s downward trajectory is pushed by quite a lot of components that inherently mirror its lack of market share and identification amongst customers, with constant retail quantity decline. Firstly, the Nissan CVT, though helpful as a result of its gas financial system and driving expertise, has seen a number of class-action lawsuits and complaints as a result of recurring issues of safety, in addition to upkeep necessities. The problems primarily coated this era c.2012-2018, creating the affiliation of unreliability with the model, at a time when Japanese manufacturers have been hailed as essentially the most dependable manufacturers on this planet, making Nissan the issue youngster.

Secondly, Carlos Ghosn. Carlos was a formidable chief and is arguably one of many best CEOs of all time, identified for his potential to remodel companies within the automotive trade. A number of main companies similar to Ford (F) and GM (GM) had tried to poach him over time. Following turnarounds at Michelin and Renault (OTCPK:RNSDF), he brokered an alliance between Nissan and Renault and joined Nissan, and later included Mitsubishi on this, with Nissan buying c.34% of its shares. Lengthy story quick, he took a struggling, debt-burdened Nissan, which solely had 3 profitability autos, and fully reworked the enterprise as a part of his “Nissan Revival Plan”. Ghosn was early within the improvement of EVs (Dedicated €4bn in 2007), believing it to signify a major progress alternative. The Ghosn management construction collapsed in 2018 following an arrest and subsequent scandals. This represents a pivotal second in Nissan’s historical past, with the enterprise on a noticeable decline since.

The Alliance stays in place, though has been equalized with the tip of its widespread buying settlement. The implications are that Nissan will additional develop its personal EV capabilities, with Renault lowering its possession in Nissan to fifteen%, aligning with Nissan’s possession of Renault (in addition to taking a stake in Ampere, the long run Renault EV spin-off). In rebalancing talks, Nissan has pushed for the safety of its EV/battery expertise, which it believes is usually a key worth driver going ahead because the migration towards a totally electrical new automotive market continues. As a part of the Alliance, no matter the way it develops going ahead, Nissan will proceed to profit from shared elements procurement with Renault, supporting operational excellence.

Though Nissan’s monetary efficiency has declined, the corporate appears to be like to be leveling off, suggesting it has bottomed.

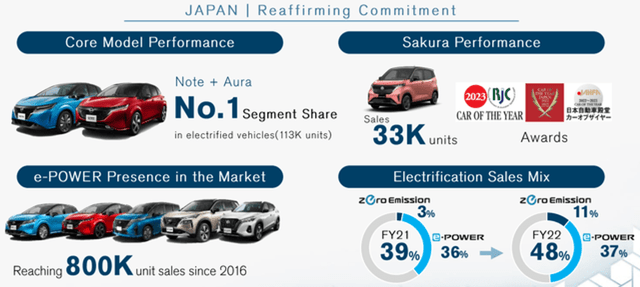

Within the Japanese market, the Word and Aura are the #1 autos within the section, with its electrified fleet reaching nearly 50% of gross sales, a lot of which is using its proprietary e-power expertise.

Japan (Nissan)

Additional, the US section is seeing market share progress in conventional ICE-powered autos, implying model and design energy, regardless of the weak spot. The US is a key marketplace for the enterprise, particularly given the energy in non-EV fashions, permitting the enterprise to steadiness its transition in gross sales.

US (Nissan)

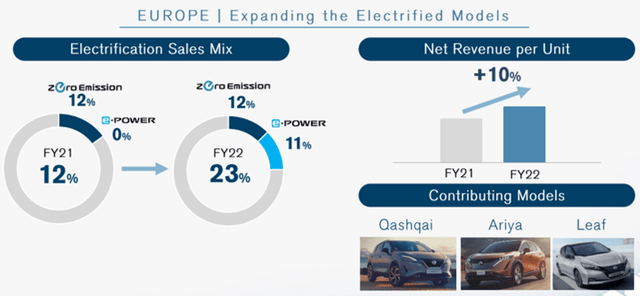

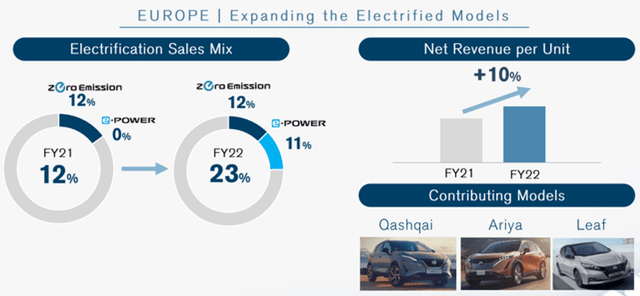

Europe continues to carry out effectively, pushed by Nissan’s efficiency within the UK, a key nation for the enterprise. This area is dominated by the Qashqai, Nissan’s compact SUV providing. Nissan has already developed an EV/E-Energy model of this car, which ought to help progress within the coming years.

Europe (Nissan)

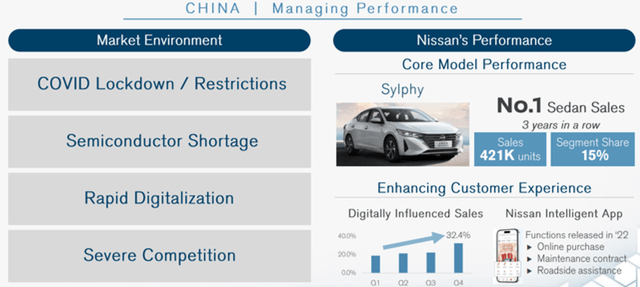

Lastly, China. Just like different operators within the nation, the zero-Covid coverage has materially impacted demand, as numerous lockdowns restricted the power to attain constant gross sales. Once more, Nissan has a robust presence within the area, as its Sylphy mannequin is the #1 sedan for 3 years operating.

China (Nissan)

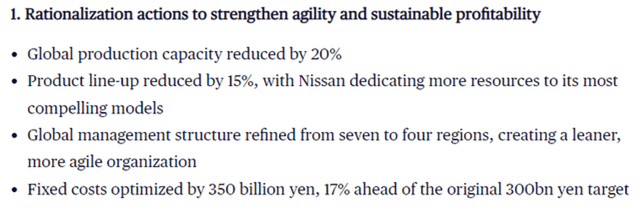

Nissan NEXT is the purpose to rationalize capability and streamline operations, prioritizing its core markets, fashions, and applied sciences, looking for to revitalize the enterprise. This entails the next targets:

Nissan NEXT half 1 (Nissan)

Nissan NEXT half 2 (Nissan)

The corporate is basically looking for to cut back its bloated operations following the decline in measurement, adopted by a partial reinvestment within the enterprise to help its new progress trajectory. On paper, this plan appears to be like appropriate and may help monetary enchancment within the coming years.

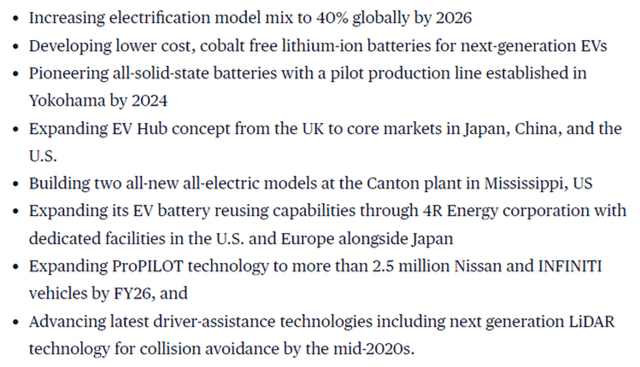

The next autos have been launched as a part of the transition to the second a part of Nissan NEXT (second screenshot above).

Nissan NEXT (Nissan)

Automotive Trade

Companies compete based mostly on components similar to model energy, car high quality, pricing methods, and technological developments.

Main rivals of Nissan embody Toyota (TM), Honda (HMC), Volkswagen (OTCPK:VWAGY), Common Motors, and Ford, Stellantis (STLA), amongst others. Nissan additionally faces competitors from EV specialists, together with Tesla (TSLA), BYD (OTCPK:BYDDF), and NIO (NIO).

The automotive is forecast to develop at a CAGR of seven% into 2030, pushed by elevated demand for EVs, as socio-economic components, alongside regulation, encourage the transition to those autos. International EV gross sales have been up 32% YoY in Q1-23, reflecting the resilience of this progress trajectory.

There have been two key developments within the trade throughout 2023. Firstly, China eradicated its NEV buy subsidy in China, contributing to diminished demand within the area, regardless of the tip of its zero-Covid coverage. Secondly, Tesla diminished its costs in February, contributing to a mini value conflict within the trade, as an estimated 40 automakers slashed costs in response.

The rising demand for electrical autos and tightening emissions rules has contributed to a lot of EVs coming into the market. On account of this, corporations are more and more pressured to diversify past simply creating an EV different to their conventional autos. Nissan’s concentrate on modern options and applied sciences, together with autonomous driving, represents a possibility to seize market share by means of technological superiority. The market stays rife for disruption.

Financial & Exterior Consideration

Present financial situations signify a near-term headwind. With heightened inflation and elevated charges, customers are deterred from making giant purchases as funds are squeezed and the price of financing purchases will increase. This mentioned, Nissan has navigated this effectively to date, because it has skilled a +15% improve in US gross sales throughout Q3 and top-line manufacturing progress of +2.8%.

That is partially because of the overhang from the chip disaster, as manufacturing is comfortably growing, permitting demand to be met. We count on a continuation of the downward trajectory of manufacturing, nonetheless, notably as Sep 23 manufacturing was down (2.8)%. The development from manufacturing coming on-line has slowly been wholly offset by client demand.

Margins

Nissan has struggled with margin consistency, experiencing a noticeable decline within the final 10 years. In the newest 12 months, the corporate had an EBITDA-M of seven% and a GPM of 16%.

The decline in margins is a mirrored image of top-line weak spot at the side of operational inefficiencies with a discount in scale. The enterprise has basically misplaced any benefits from the Alliance, illustrating why Nissan’s Administration is sad with the state of affairs. With the brand new settlement, we count on a change in fortunes, though it’s far too early to quantify this.

The problem is that the enterprise should enhance the top-line earlier than the underside will comply with.

Steadiness sheet & Money Flows

Though the corporate has a big ND/EBITDA, curiosity funds signify 1% of income, with enough protection at 12x. This provides us consolation that there isn’t any near-term solvency threat however the steadiness is a matter. Fitch assigns a BBB- score.

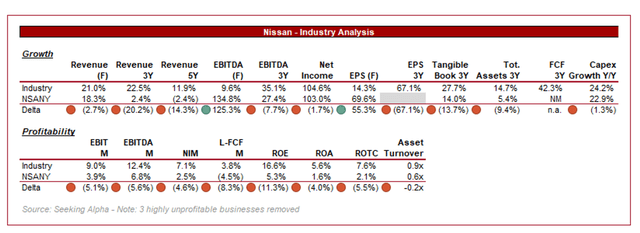

Trade evaluation

Automotive trade (Searching for Alpha)

Offered above is a comparability of Nissan’s progress and profitability to the typical of its trade, as outlined by Searching for Alpha (29 corporations).

Nissan’s sluggish efficiency is mirrored by its relative efficiency to friends. The corporate’s progress is considerably beneath the trade common. The trade has usually carried out effectively in the previous couple of years because of the improvement of EVs, with Nissan unable to translate this to top-line efficiency.

Margins are unsurprisingly poor, particularly given the dimensions Nissan has. Enchancment doesn’t must be vital to succeed in parity however the enterprise has an extended option to go to return to its prior ranges. Administration is hopeful that the change to the Alliance’s phrases ought to enable for an enchancment within the coming years.

Based mostly on this, and our prior evaluation, Nissan ought to commerce at a big low cost to its historic common and friends.

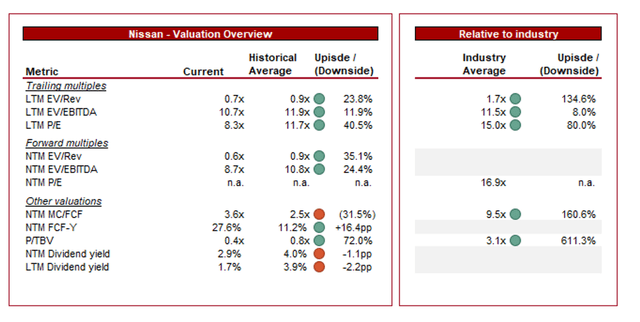

Valuation

Valuation (Capital IQ)

Nissan is at present buying and selling at 11x LTM EBITDA and 9x NTM EBITDA. It is a low cost to its historic common.

A reduction to its historic common and peer group is undeniably warranted in our view, owing to the corporate’s decline in monetary efficiency and uninspiring EV transition, in addition to lack of market share. This has contributed to a major improve in its FCF yield, though with a corresponding heightened threat of progress declining.

Conversely, the trade is dealing with tailwinds into 2030 and Nissan appears to be like to be on the up following an prolonged interval of problem. Nonetheless, we don’t consider that is enough to recommend the inventory is undervalued but. We recommend traders stay affected person for additional proof of enchancment.

Closing ideas

We consider Nissan’s model remains to be extremely regarded regardless of its weak spot in recent times, supporting the resurgence efforts of Administration. We consider the corporate is on an upward trajectory, because the Nissan NEXT technique appears to be like to be yielding outcomes and will probably be compounded by the brand new Alliance settlement.

This mentioned, the corporate nonetheless has a lot progress remaining, together with considerably bettering margins. We don’t consider the valuation adequately costs within the dangers round enchancment and near-term dangers.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.

[ad_2]

Source link

(NYSE:CB)")

")

")

")

Entry Point")

{kind=link}