[ad_1]

Morsa Pictures

Three months in the past, in early April of this yr, I wrote a bullish article relating to a reasonably small financial institution by the identify of Pathward Monetary (NASDAQ:CASH). In fact, small as relative. For context, the corporate has, as of this writing, a market capitalization of $1.14 billion. Again then, the scale of the enterprise was a bit smaller. However the market has rewarded good efficiency over this window of time. Because the publication of that article, shares have skyrocketed by 14.5%. That is properly above the 5.2% enhance seen by the S&P 500 over the identical window of time.

With such a transfer greater over such a small interval, you may assume that the aim of this text could be to downgrade the inventory. That may be a cheap expectation, particularly when you think about how costly shares are on a worth to guide and worth to tangible guide foundation. Nonetheless, the enterprise continues to attain enticing progress on each its high and backside traces. Moreover, shares are low cost relative to earnings, and the standard of the establishment’s property is sort of excessive. On the finish of the day, I imagine that there’s additional upside available. So due to that, I’ve determined to maintain the corporate rated a ‘purchase’ for now.

A stable play

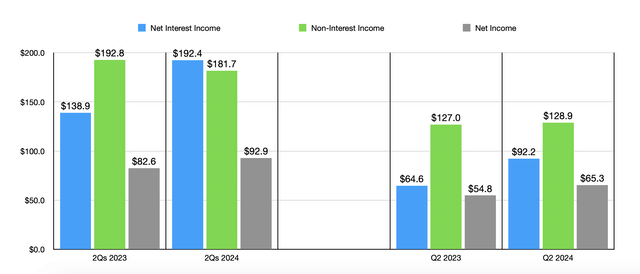

Once I final wrote about Pathward Monetary in April, we had information extending by way of the primary quarter of the 2024 fiscal yr. As we speak, that information now extends by way of the second quarter. In that prior article, I made clear that one of many the reason why I appreciated the enterprise was as a result of it continued to develop. And that sentiment hasn’t modified. Take, for instance, the online curiosity revenue generated by the establishment within the second quarter of 2024. Internet curiosity revenue for that point got here in at $92.2 million. That is 42.7% above the $64.6 million generated the identical time one yr earlier. A part of this enchancment was due to a $10.7 million yr over yr drop within the provision for credit score losses that the enterprise booked. Nonetheless, the corporate additionally benefited from different adjustments.

Writer – SEC EDGAR Knowledge

Most notably, curiosity revenue and charges managed to rise from $83.9 million to $102.8 million throughout this window of time. A variety of this was due to an increase within the complete worth of loans and leases from a median steadiness of $4.01 billion to $4.90 billion. There have been different contributors as properly. Usually with banks, you anticipate a big enhance in the price of deposits when rates of interest are on the rise. Nonetheless, solely 9.5% of the corporate’s common deposits throughout the latest quarter had been curiosity bearing in nature. So despite the fact that the price of these deposits grew from 2.19% to three.87%, the final word affect on the corporate’s high line was negligible. The truth that a lot of the deposits are non-interest bearing could be chalked as much as the agency’s general enterprise mannequin, basically working as a banking-as-a-service (or BaaS) supplier that offers with pay as you go playing cards, fee options, and that additionally engages in different actions like providing quick time period refund advance loans and short-term digital return originator advance loans.

Writer – SEC EDGAR Knowledge

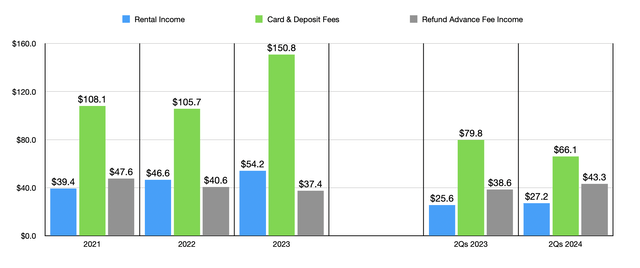

This isn’t the one a part of the corporate that has seen some progress. Within the second quarter of 2022, non-interest revenue was $128.9 million. In recent times, the financial institution had seen some enticing progress from sure market segments. Within the chart above, you’ll be able to see what a few of these have been. Nonetheless, the expansion skilled in some weak spot in these areas, corresponding to when it got here to card and deposit charges, and refund switch product charges. The rise, then, largely got here from an increase in refund advance charge revenue and a slight enhance in rental revenue. With internet curiosity revenue and non-interest revenue each rising, internet earnings for the establishment additionally improved. They finally rose from $54.8 million to $65.3 million. In fact, the second quarter was not a one-time blip. For the primary half of the yr as an entire, internet revenue elevated, rising from $82.6 million to $92.9 million.

Writer – SEC EDGAR Knowledge Writer – SEC EDGAR Knowledge

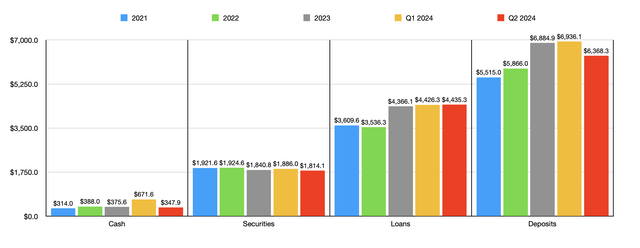

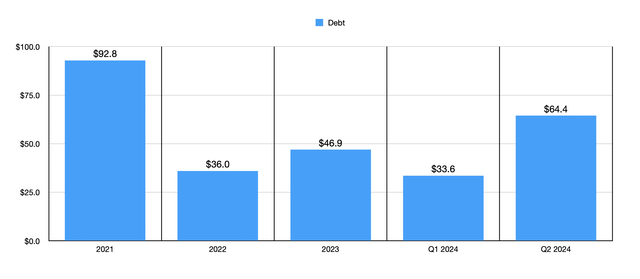

There have been different components of the corporate which have expanded as properly. However a giant exception to this might be the worth of deposits on its books. These truly contracted from $6.94 billion to $6.37 billion. Usually, I might discover this regarding. I might additionally discover the drop in money from $671.6 million to $347.9 million, and the decline in securities from $1.89 billion to $1.81 billion, regarding. Nonetheless, the worth of loans did enhance modestly from $4.43 billion to $4.44 billion, whereas debt remained low at solely $64.4 million. I additionally take consolation in the truth that uninsured deposits account for under 16.2% of complete deposits. This makes the chance of a disaster on the establishment, much like what we noticed in March of final yr all through the sector, fairly low.

Writer – SEC EDGAR Knowledge

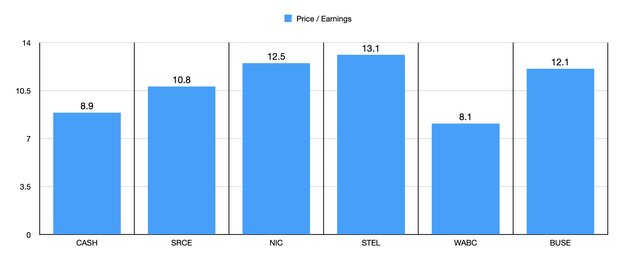

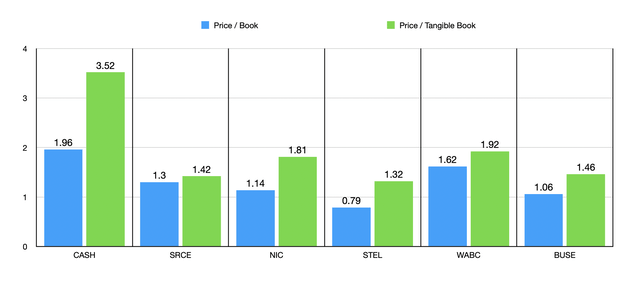

By way of valuation, the corporate is each low cost and costly. Within the chart above, you’ll be able to see how shares are priced relative to earnings. With a worth to earnings a number of of 8.9, we discover that solely one of many 5 firms I in contrast it to in that chart ended up being cheaper than it. Within the chart beneath, in the meantime, I regarded on the enterprise by way of the lens of the value to guide a number of and the value to tangible guide a number of. And in each of these cases, Pathward Monetary ended up being the costliest of the group.

Writer – SEC EDGAR Knowledge

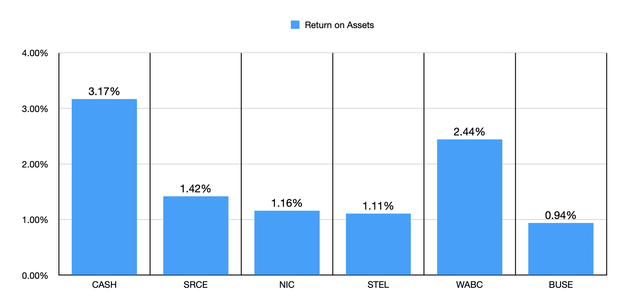

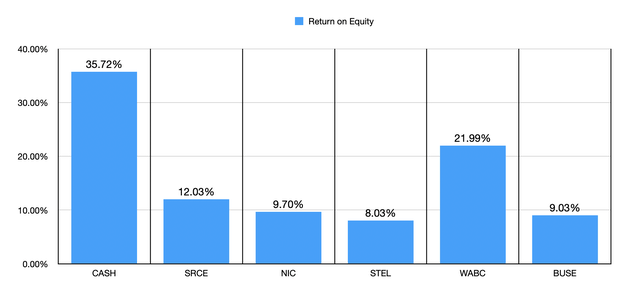

Normally, I might contemplate such a excessive worth to guide a number of a deal breaker for a monetary establishment, particularly a financial institution. Nonetheless, contemplating that almost all of the corporate’s income comes from non-interest revenue, I view the image a bit otherwise. At its core, Pathward Monetary is extra a various monetary establishment that simply so occurs to have banking operations, versus being the other. This additionally displays within the high quality of the establishment’s property. Within the first chart beneath, you’ll be able to see how the agency stacks up in opposition to 5 related companies in relation to the return on property metric. Of the group, Pathward Monetary ended up being the best. Within the subsequent chart, I did the identical factor when it got here to return on fairness. As soon as once more, our candidate was higher than its friends.

Writer – SEC EDGAR Knowledge Writer – SEC EDGAR Knowledge

Clearly, as with every funding, buyers could be clever to pay cautious consideration to danger components. I might argue that one of many greater dangers going through Pathward Monetary presently could be a decline in rates of interest. With many monetary establishments, rising rates of interest can show an issue. It’s because the rise in rates of interest could make it interesting for depositors to put funds elsewhere. Good seeing as how the overwhelming majority of Pathward Monetary’s deposits will not be curiosity bearing, the maths right here adjustments. The Federal Reserve started elevating rates of interest in March of 2022. In 2021, the online curiosity margin for the corporate was 3.84%. This quantity grew to six.05% in 2023. The truth that an awesome majority of its property are interest-bearing ($6.42 billion in comparison with $399.7 million that’s within the type of interest-bearing liabilities as of the top of the 2023 fiscal yr) is indicative {that a} discount in rates of interest might show painful for the corporate.

There are at all times different dangers as properly. In April of this yr, information broke that the corporate could be paying refunds and a penalty associated to an investigation by the New York Lawyer Basic Letitia James. The mixed quantity is simply over $700,000, with $627,000 of it within the type of a penalty. Based on the investigation, from 2016 to 2022, Pathward Monetary ‘illegally froze some 1,400 accounts belonging to New Yorkers’. It is supposedly instructed third occasion servicers to do that and to show over customers funds to debt collectors. This allegedly occurred a number of instances. This may finest be described as a compliance and managerial downside. However every time there’s something of this nature, the general public notion no less than is that there’s an elevated likelihood that there are different compliance and managerial points but to be found. So from a regulatory perspective, there may be some concern.

Takeaway

Essentially talking, Pathward Monetary is doing very well for itself. Current share worth efficiency has mirrored improved fundamentals, although it’s true that some components of the steadiness sheet declined in worth. The corporate’s high and backside traces proceed to develop, asset high quality is high notch, and shares are low cost relative to earnings. Given these components, I’ve no downside maintaining the enterprise rated a ‘purchase’ presently.

[ad_2]

Source link