[ad_1]

DNY59

We beforehand coated PayPal Holdings, Inc. (NASDAQ:PYPL) in Could 2024, discussing its rising Lively customers and increasing working margins, because the administration drove engagement and optimized prices in FQ1’24.

Mixed with its inherent undervaluation and strong shareholder returns, we believed that the inventory’s bullish help had lastly materialized, with it more likely to be slowly upgraded nearer to its fintech friends and historic means, providing buyers with the opportunistic probability of a terrific upside potential.

Since then, PYPL has additional rallied by +12.6%, outperforming the broader market at +7.8%. Even so, we’re sustaining our Purchase score right here, as the brand new administration workforce delivers excessive double-digit adj EPS development in H1’24 whereas elevating their FY2024 adj EPS steering.

Mixed with Braintree’s enhancing profitability and the launch of Fastlane within the US, we imagine that the fintech continues to supply a compelling development funding thesis for opportunistic buyers.

PYPL’s Reversal Is Right here – Behemoth Fintech In The Making

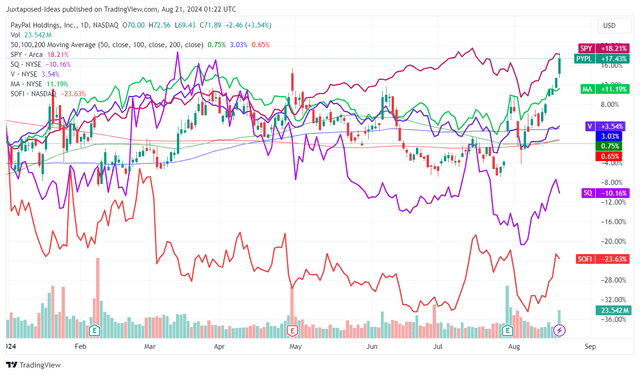

PYPL YTD Inventory Value

TradingView

After dropping -82.6%, or the equal of -$307.11B of its market cap because the July 2021 peak, PYPL has began to outperform its fintech friends on a YTD foundation, together with SoFi Applied sciences, Inc. (SOFI), Block, Inc. (SQ), Visa Inc. (V), and Mastercard Included (MA).

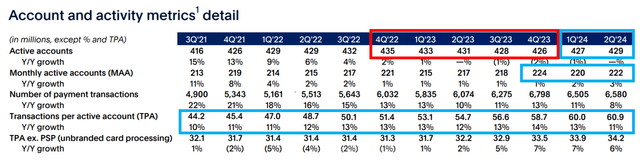

PYPL’s Promising Reversal In Lively Account Churn

PYPL

Maybe a part of the tailwinds could also be attributed to PYPL’s promising reversal within the Lively Accounts churn noticed since FQ4’22, with issues seemingly bottoming by FQ4’23 and sequentially enhancing via FQ2’24.

Its fintech platform seems to be extraordinarily sticky for its present customers as effectively, primarily based on the constant enlargement in its Whole Cost Quantity [TPV] and Transactions Per Lively Accounts [TPA] over the previous few years, with it underscoring why the large sell-off noticed within the inventory has been unwarranted.

The inventory’s strong YTD efficiency might also be attributed to PYPL’s double beat FQ2’24 earnings outcomes, with complete revenues of $7.88B (+2.4% QoQ/ +8.2% YoY) as the brand new administration workforce delivers spectacular early outcomes.

Transferring ahead, we imagine that it stays effectively positioned to report strong topline development via Fastlane, with the administration already highlighting that “knowledge from our early adopters exhibits that returning Fastlane customers, convert at practically 80% versus the trade common visitor checkout conversion nearer to 50%.”

That is additionally why PYPL has aimed to combine Fastlane throughout its giant retailers on Braintree and small-to-medium retailers on PayPal Commerce Platform together with its gross sales companions, corresponding to Salesforce (CRM), Adobe (ADBE), and BigCommerce (BIGC) by H2’24.

With Fastlane permitting the fintech to faucet into the ~60% share of e-commerce purchases made via guide card entry, we imagine that it might be able to develop its customers together with revenue margins, considerably aided by Venmo’s rising month-to-month actives by +30% YoY.

It’s obvious from these developments that PYPL’s well-diversified and vertically built-in platform throughout retail P2P, small-to-medium retailers, and enormous enterprises, has been extremely strategic in driving person development, service provider adoption, and high/ bottom-lines.

If something, the administration is already trying to faucet into the excessive margin promoting market via PayPal Adverts on its end-to-end fintech platform, with it probably being an enormous development driver, primarily based on Meta’s (META) $153.28B in FQ2’24 annualized promoting revenues via social media and Google (GOOGL) (GOOG) at $258.44B via its market main search engine/ streaming.

Transferring forward, PYPL has additionally executed effectively on its strategic value financial savings plan, as noticed in its stabilizing transaction margin of 45.8% (+0.8 factors QoQ/ -0.1 YoY/ -8 from FQ4’19 ranges of 53.8%), increasing working margin of 18.5% (+0.3 factors QoQ/ +2.3 YoY/ -5.5 from FQ4’19 ranges of 24%) and wealthy adj EPS of $1.19 (+10.1% QoQ/ +36.7% YoY).

Most significantly, Braintree has lastly achieved financial system of scale due to the administration’s strategic deal with price-to-value in areas throughout its giant enterprise companions, with it “now meaningfully contributing to transaction margin greenback development for the primary time in over two years,” probably resulting in the fintech’s revenue margin restoration nearer to 2019 ranges.

Because of the strong high/ bottom-line development, PYPL has been in a position to retire -6% of its float over the LTM and -11.7% since FY2019 as effectively, with the administration trying to return all of their projected FY2024 Free Money Circulate technology of $6B (+30.4% YoY) to long-term shareholders, primarily based on the raised FY2024 share repurchase goal from $5B to $6B.

The decrease share depend has additionally aided the rising adj EPS, with the fintech’s stability sheet nonetheless extraordinarily wholesome at a web money place of $6.1B (-8.9% QoQ/ +56.4% YoY).

Because of this, it’s unsurprising that PYPL has raised their FY2024 steering, with adj EPS development within the “low-to-mid-teens” at roughly ~$4.32 (+12.5% YoY) in comparison with the unique steering of “mid-to-high-single-digits” at ~$4.12 (+7.5% YoY) from FY2023 numbers of $3.83 (+23.9% YoY).

With the raised steering constructing upon the adj EPS development at +31.9% YoY noticed in H1’24, we imagine that the administration’s steering has been on the overly prudent aspect certainly, with one other beat and lift efficiency very doubtless within the FQ3’24 earnings name – naturally justifying the inventory’s YTD restoration.

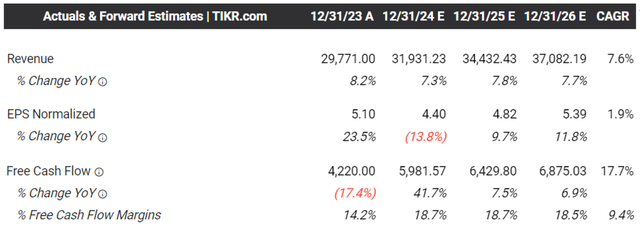

The Consensus Ahead Estimates

Tikr Terminal

And that is additionally why the consensus has already raised their ahead estimates, with PYPL anticipated to generate an accelerated bottom-line development at a CAGR of +8.94% from the LTM adj EPS of $4.39 to FY2026 numbers of $5.39, together with Free Money Circulate at +17.7%.

Even so, we imagine that these estimates are on the low aspect, given the excessive double-digit growths noticed in H1’24, with one other improve doubtless.

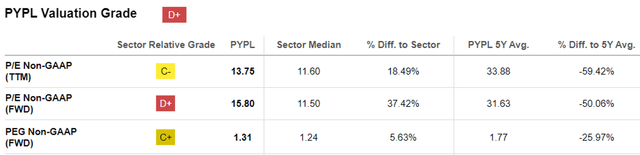

PYPL Valuations

Looking for Alpha

Because of this, we imagine that PYPL continues to be buying and selling fairly at FWD P/E valuations of 15.80x, regardless of the notable improve from its 1Y imply of 12.44x and the sector median of 11.38x.

Even when evaluating PYPL’s PEG ratio at 1.31x to its fintech friends, together with SOFI at 1.22x, SQ at 0.50x, V at 2.14x, and MA at 2.00x, it’s obvious that PYPL continues to be fairly valued right here – providing buyers with a wonderful margin of security.

So, Is PYPL Inventory A Purchase, Promote, or Maintain?

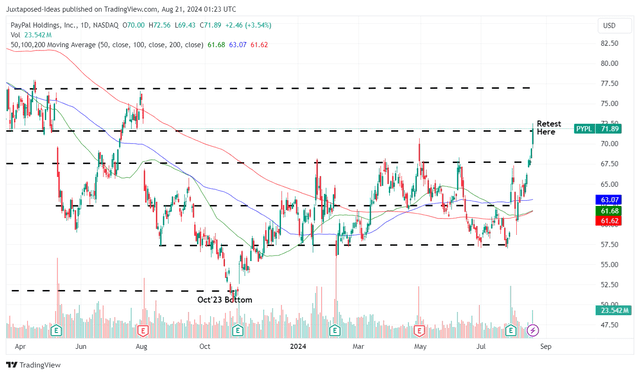

PYPL 1Y Inventory Value

TradingView

For now, PYPL has traded sideways because the finish of 2023, with the inventory now retesting the 2024 resistance ranges of $70s whereas operating away from its 50/ 100/ 200 day shifting averages.

For context, we had provided a fair-value estimates of $60.70 in our final article, primarily based on the FWD P/E of 14.92x and the (new methodology) LTM adj EPS of $4.07 ending FQ1’24.

Based mostly in the marketplace’s just lately upgraded FWD P/E valuations of 15.80x and the LTM adj EPS of $4.29 ending FQ2’24, it seems that PYPL continues to be buying and selling close to to our up to date base-case estimated honest worth of $67.80.

Based mostly on the consensus FY2026 adj EPS estimates of $5.39 and the identical P/E valuation, we’re a good upside potential of +18.3% to our long-term value goal of $85.10 as effectively.

This isn’t forgetting a possible upward re-rating in its FWD P/E valuations to its 5Y imply of ~30x (nearer to its friends primarily based on PYPL’s accelerated bottom-line development prospects), with it bringing forth a bull-case honest estimate of $128.70 and long-term value goal of $161.70, respectively.

Because of the nonetheless engaging threat/ reward ratio at present ranges, we’re sustaining our Purchase score for the PYPL inventory.

Danger Warning

Whereas we could have provided a fairly bullish value goal, readers should notice that PYPL’s inventory value reversal is predicted to be extended since it’s unsure if the churn noticed in its Lively Accounts since FQ4’22 has ended and whether or not the sequential development from FQ1’24 onwards could proceed.

On the similar time, Fastlane’s widespread adoption/ monetization could also be slower than anticipated, since it’s only just lately launched in early August 2024, with a chance of minimal high/ bottom-line increase in FQ3’24. With the outcomes doubtless solely in by FQ4’24, buyers could wish to mood their near-term expectations certainly.

That is particularly since PYPL has guided greater non-transaction working bills, partially attributed to intensified advertising efforts and the normalization in transaction/ credit score losses, with it probably triggering a near-term bottom-line affect on a sequential foundation.

[ad_2]

Source link