[ad_1]

sankai

PDF Options (NASDAQ:PDFS), a differentiated software program and engineering companies firm, is arguably buying and selling at a comparatively sustainable valuation in the intervening time within the close to time period, regardless of it being valued greater in comparison with the broader business. Given the sturdy development for FY25 estimated and a big backlog supporting this, I’m bullish on PDFS inventory within the close to time period, with a 12-month to 18-month market cap development goal of round 25%.

Firm Profile, Aggressive Threats, & Market Shifts

PDF Options makes a speciality of software program and engineering companies, significantly for the semiconductor business. It’s targeted on reworking semiconductor manufacturing and take a look at information into actionable insights. It helps firms to interrupt down information silos inside their provide chains, leveraging this information to enhance key efficiency indicators. Their options are utilized by over 500 purchasers, together with main business gamers like TSMC (TSM), Intel (INTC), and Qualcomm (QCOM), to help the manufacturing and testing of ICs and SoCs. Their companies are particularly designed to assist purchasers scale back prices and enhance profitability in manufacturing and take a look at environments, and its Exensio platform acts as an end-to-end analytics answer to empower semiconductor engineers and information scientists.

PDF options are thought of a comparatively uncommon asset within the semiconductor business, largely due to their specialised concentrate on yield and course of automation software program. The corporate gives open connection and information evaluation for varied instruments, which distinguishes it from rivals that provide extra closed methods. Nonetheless, the corporate does face direct rivals, together with yield administration and prediction methods, akin to KLA-Tencor (KLAC), Siemens (OTCPK:SIEGY), Onto Innovation (ONTO), and Synopsys (SNPS).

Nonetheless, maybe extra considerably, PDF Options additionally faces a rising risk from inside groups inside IC firms that will develop customized options in-house that cater to their particular wants. As tech firms search to consolidate their moats and grow to be extra vertically built-in, I do consider this might grow to be extra of an issue for PDF Options in the long run. Regardless of the problem right here, there’s the chance for PDF Options to place itself as a complementary associate somewhat than a competitor.

PDF Options reported a big backlog of $243.2M as of June 30, 2024, indicating sturdy future demand for its services and laying the muse for strong income development in FY25. Moreover, the semiconductor business is experiencing a shift in direction of superior nodes and the emergence of latest foundries, which helps the expansion potential of PDF Options’ progressive instruments like Design-for-Inspection (‘DFI’), bettering the power to research chips throughout manufacturing for high quality management and improved yield.

Q2 Earnings, Valuation Evaluation, & Monetary Concerns

In Q2, reported on 8/8/24, PDF reported income of $41.7M, which is comparatively flat YoY and barely up from the prior quarter. Its EPS was $0.18, an enchancment from the $0.15 within the earlier quarter. Moreover, as I discussed, its backlog elevated to $243.2M, up from $229.8M on the finish of 2023, reflecting sturdy future demand and development potential. As well as, it ended the quarter with $118M in money and ST investments, down from $123M in Q1, largely as a consequence of capex investments in its DFI system.

Within the earnings name, administration outlined that its DFI system noticed excessive utilization from key prospects, signaling a powerful demand pipeline and the potential for multi-year contracts. As well as, its MLOps product, which leverages AI for testing, is gaining traction, and administration is anticipating whole income development of round 20% YoY in H2. That is largely anticipated to be pushed by continued demand for superior semiconductor options in AI, machine studying, and digital transformation.

In my view, the earnings outcomes and name point out a cause to be bullish on the inventory, particularly because it beat the non-GAAP EPS estimate by $0.04 and the income estimate by $0.22M.

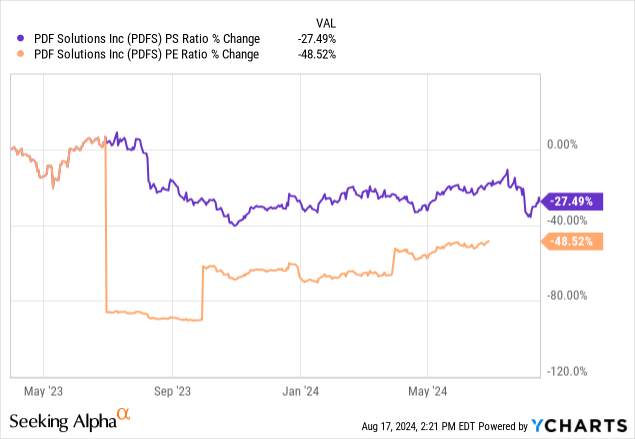

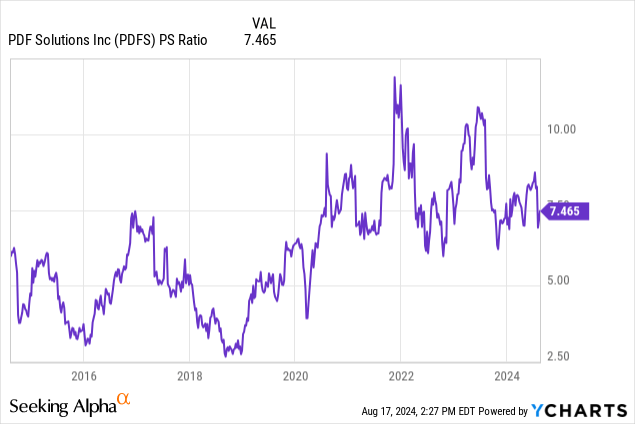

Regardless of the energy in its latest earnings outcomes, PDFS inventory is richly valued, with a ahead P/E non-GAAP ratio of 41 and a ahead P/S ratio of 6.86, each of that are over 100% greater than the sector median. That being mentioned, each the GAAP P/E ratio and P/S ratio are down considerably in comparison with 5 years in the past.

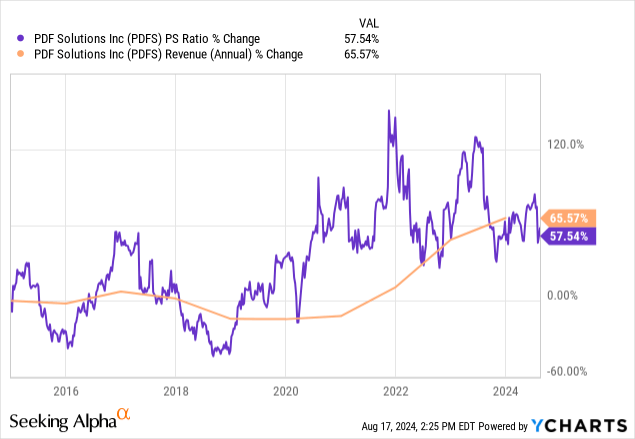

As the corporate is working at a loss in the intervening time, with a internet margin of -1.67%, I feel that the inventory is finest evaluated via its P/S ratio. This has elevated barely lower than its whole income in % change over the previous 10 years. Due to this fact, whereas the inventory is richly valued, it’s arguably not too costly, in my view.

Nonetheless, as a result of its YoY income development is just 2.28%, which is far decrease than its five-year common of ~15%, there’s probably some trigger for volatility concern. Regardless of this, the valuation is affordable sufficient at current to permit traders to capitalize on the sturdy FY25 development estimates from Wall Avenue:

In search of Alpha In search of Alpha

Primarily based on these estimates and its present P/S ratio, I feel that it’s prone to attain a market cap of $1.58B in some unspecified time in the future in FY25 if Wall Avenue estimates are realized and the P/S ratio is ~7 on the time. This means a possible 26.5% development in simply over a yr, primarily based on my evaluation.

These sturdy development charges are supported by its order backlog, which I discussed in my operational evaluation. Moreover, the corporate is deploying new methods like its Sapience Manufacturing Hub, in partnership with SAP (SAP) and MLOps, the latter of which is AI-based and is gaining traction amongst prospects. On that notice, the demand for semiconductors fueled by the large tech AI arms race is predicted to proceed to be accretive for PDFS via 2025.

Regardless of the unfavourable profitability in the intervening time, PDFS does have sturdy free money circulation, which, whereas not traditionally linear in development, is at present $0.19 per share. That is largely attainable regardless of its internet loss due to its excessive ranges of SBC. This makes its earnings assertion extra tolerable, however I nonetheless assume development from PDFS inventory will probably be average as a result of its earnings are clearly cyclical, and because the valuation is already fairly excessive, whereas it probably has extra room to develop in worth over the following few years, I count on plenty of draw back volatility following a peak.

Lengthy-Time period AI Semiconductor Outlook, Financial Progress Slowing, & Volatility Dangers

The combination of AI applied sciences continues to be a big driver of demand within the semiconductor business. As generative AI capabilities proceed to develop, the necessity for high-performance semiconductors will increase, benefiting firms like PDF Options that present analytics and course of management instruments important for superior semiconductor manufacturing.

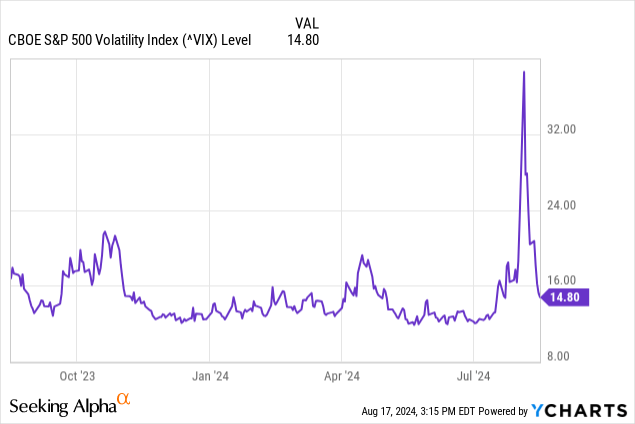

Nonetheless, this development curve isn’t going to final indefinitely, and with the worldwide financial system experiencing a slowdown, there are potential implications for firms like PDF Options on account of diminished client spending and funding in know-how. As well as, the Volatility Index (‘VIX’), also called the “worry gauge”, had an excessive peak in early August, signifying greater volatility danger, though this has since declined considerably.

There are additionally now rising issues about layoffs that massive tech firms will probably be instigating as a consequence of issues of income contraction from macroeconomic pressures, together with a extremely inflationary setting with plenty of federal debt. I consider that we’re coming into a fragile interval, particularly with China’s rise, and I consider that if america authorities doesn’t place itself with extra budgetary restraint, PDFS might be negatively impacted by a recessionary interval within the West. That is very true as 56% of its working income comes from the U.S.

Conclusion

In my view, there’s a potential 12-month alpha play right here that might ship round 25% worth development. Nonetheless, there’s additionally important volatility danger associated to each the corporate’s excessive valuation and broader macroeconomic strain and indications of bearish sentiment coming into the market via the VIX. Nonetheless, within the close to time period, the inventory is a Purchase, but it surely have to be monitored as a result of it’s a cyclical play, and I consider taking revenue in FY25 round my market cap estimate might be clever except, after evaluation throughout that yr, its development prospects look set to proceed. I’ll endeavor to offer follow-up protection to evaluate this nearer the time.

[ad_2]

Source link