[ad_1]

Torsten Asmus

Permian Sources (NYSE:PR) reported robust Q1 2024 outcomes after making quick progress in integrating its acquisition of Earthstone Vitality. It elevated its full-year steering for each whole manufacturing and oil manufacturing by 2%. That does not embody the influence of some further acquisitions that Permian made (totaling $270 million in consideration) that ought to increase its 2H 2024 manufacturing by one other %.

Permian is now anticipating an additional $50 million per yr in value financial savings (as much as $225 million per yr) from its Earthstone acquisition. The extra prices financial savings plus Permian’s elevated manufacturing helps increase its estimated worth to $18 per share, up $1 from once I final appeared on the firm.

Q1 2024 Manufacturing

Permian Sources introduced robust Q1 2024 outcomes with 319,514 BOEPD in whole manufacturing, together with 151,794 barrels per day in oil manufacturing. Permian famous that its oil manufacturing elevated by 11% in comparison with This fall 2023, though that quarter solely included two months contribution from Earthstone since that acquisition closed one month into the quarter. Permian’s oil manufacturing would have been pretty related quarter-over-quarter if the Earthstone acquisition had closed initially of This fall 2023.

The higher than anticipated Q1 2024 manufacturing outcomes have been attributed to glorious effectively outcomes together with the quick integration of Earthstone. Permian has decreased the manufacturing downtime related to Earthstone’s property.

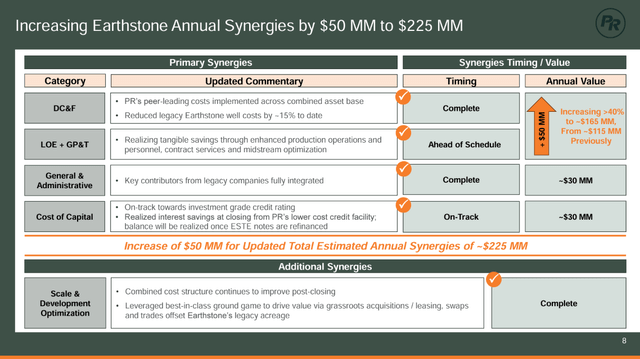

Elevated Synergies

Permian introduced that its integration of Earthstone was completed forward of schedule and that it elevated its annual synergy goal by $50 million. Permian now’s aiming for $225 million in annualized financial savings.

This $50 million in further financial savings is predicted to return from a mixture of additional reductions in D&C prices and working prices. Permian has now decreased Earthstone’s D&C prices by roughly 15%, greater than the roughly 12% discount it talked about a couple of months in the past. By Could 1st, Permian was not utilizing any of Earthstone’s drilling rigs or completion crews.

Earthstone Deal Synergies (permianres.com (Q1 2024 Presentation))

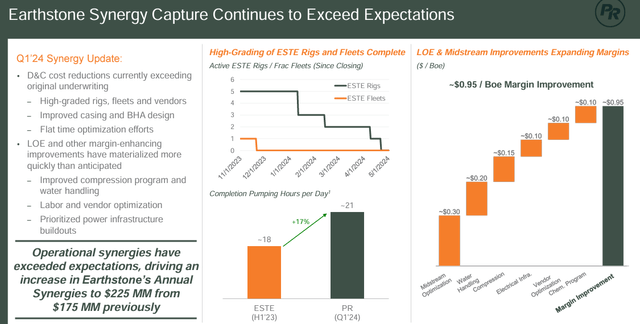

Permian additionally talked about that it had considerably decreased Earthstone’s manufacturing downtime and improved margins on Earthstone’s manufacturing by almost $1 per BOE by midstream optimization initiatives and different efforts.

Margin Enhancements (permianres.com (Q1 2024 Presentation))

Administrative Liquidation

Permian introduced that it liquidated Lynden Vitality Corp. as an administrative transfer. This transfer simplifies Permian’s company construction and reduces its go ahead tax obligations and does not have an effect on its steering.

Earthstone introduced its acquisition of Lynden Vitality in 2015 to enter the Permian. On the time, Earthstone was principally an Eagle Ford producer. Lynden Vitality was a Canadian (British Columbia) firm that was a subsidiary of Earthstone attributable to that 2015 acquisition. Though Lynden was Canadian, its oil and gasoline property have been American and almost all within the Permian Basin.

This strikes saves Permian the work of being a reporting issuer in Canada, however is in any other case extra fascinating for the way it highlights how briskly Earthstone grew by acquisitions.

In Q3 2015 (pre-Lynden acquisition), Earthstone was producing underneath 5,000 BOEPD. By the point of its acquisition by Permian Sources it was producing round 130,000 BOEPD and now Permian is anticipating to common round 320,000 BOEPD in 2024. Centennial Useful resource Improvement (which mixed with Colgate Vitality to type Permian Sources) solely averaged a bit over 7,300 BOEPD in 2015.

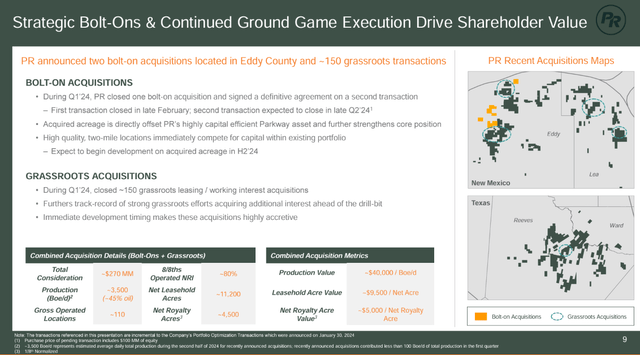

Further Acquisitions

Permian additionally lately introduced some further transactions. For the mixed transactions it added 11,200 internet leasehold acres and 4,500 internet royalty acres for about $270 million in whole consideration, together with $170 million in money. The acquired royalty acreage helps the royalty burden to roughly 20% in comparison with the standard 25% within the space.

The acquired property contributed lower than 100 BOEPD to Permian’s Q1 2024 outcomes however are anticipated to contribute 3,500 BOEPD (45% oil) to its 2H 2024 outcomes. Permian talked about that it expects to start improvement on its bolt-on acquisitions in 2H 2024, whereas its grassroots acquisitions have been accomplished simply forward of quick improvement efforts on that acreage.

Permian’s Acquisitions (permianres.com (Q1 2024 Presentation))

As a result of 2H 2024 improvement, Permian expects roughly $50 million in incremental capex associated to those acquisitions within the second half of the yr.

Up to date 2024 Outlook

Permian elevated its full-year steering midpoint to 320,000 BOEPD, together with 150,000 barrels of oil per day (47% oil lower). This was a 2% enhance in each whole manufacturing and oil manufacturing steering.

This does not have the influence of the latest acquisitions that Permian expects so as to add 3,500 BOEPD (45% oil) to its 2H 2024 manufacturing. Thus, I’m modeling Permian’s full-year 2024 outcomes at round 322,000 BOEPD, together with roughly 151,000 barrels per day of oil manufacturing.

At that degree of manufacturing and at present strip costs of roughly $80 WTI oil and $2.50 Henry Hub pure gasoline for 2024, Permian is projected to generate $5.310 billion in revenues after hedges.

Sort Models $/Unit $ Million Oil (Barrels) 55,115,000 $79.00 $4,354 NGLs (Barrels) 27,224,910 $26.00 $708 Pure Fuel [MCF] 212,163,150 $1.30 $276 Hedge Worth -$28 Whole Income $5,310 Click on to enlarge

Permian’s capital expenditure funds ought to be round $2.05 billion now, with the incremental $50 million in capex related to its latest acquisitions.

Bills $ Million Lease Working, Money G&A and GP&T $943 Manufacturing Taxes $400 Money Curiosity $260 Capital Expenditures $2,050 Money Revenue Taxes $45 Merger Integration Prices $20 Whole Bills $3,718 Click on to enlarge

Permian is now projected to generate $1.592 billion in free money stream in 2024 regardless of the modest enhance in spending.

The extra $50 million in 2H 2024 capex will doubtless solely be round half paid again by the top of 2024 from the web revenues generated by the three,500 BOEPD in added 2H 2024 volumes. Thus, that funding has a slight detrimental impact on 2024 free money stream however will profit Permian’s 2025 outcomes.

Notes On Valuation

I’ve elevated my estimate of Permian’s worth by $1 per share to a brand new estimate of $18 per share. That is primarily based on my long-term (after 2024) commodity costs of $75 WTI oil and $3.75 Henry Hub pure gasoline.

The rise in Permian’s estimated worth displays the constructive revision to its 2024 manufacturing steering, in addition to the extra $50 million in annual synergies it believes it will probably obtain from the Earthstone deal.

With Permian buying and selling at a bit over $16 per share now, I think about it a greater worth than a couple of months in the past and have moved it to a purchase score once more. Permian traded at a bit over $18 in April 2024.

Conclusion

Permian Sources delivered robust Q1 2024 outcomes that contributed to its rising its full-year manufacturing steering by 2%. It ought to have the ability to generate near $1.6 billion in 2024 free money stream at present strip costs now.

Permian now additionally expects to realize $225 million in annual synergies from its Earthstone Vitality deal, up from $175 million earlier than. The mixture of elevated synergies and improved manufacturing expectations will increase Permian’s estimated worth to $18 per share at long-term $75 WTI oil and $3.75 Henry Hub pure gasoline now. I think about it simply undervalued sufficient to warrant a purchase score now.

[ad_2]

Source link