[ad_1]

PeopleImages/iStock by way of Getty Photographs

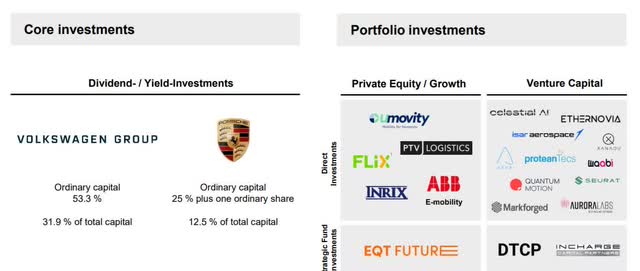

Porsche Holding (OTCPK:POAHY) (OTCPK:POAHF) is a German holding firm working within the automotive sector. Its two foremost subsidiaries are Volkswagen (31.9% of whole capital) and Porsche Auto (12.5% of whole capital). The corporate additionally holds a diversified funding portfolio, although its impression on the monetary efficiency is proscribed.

Firm’s investor presentation

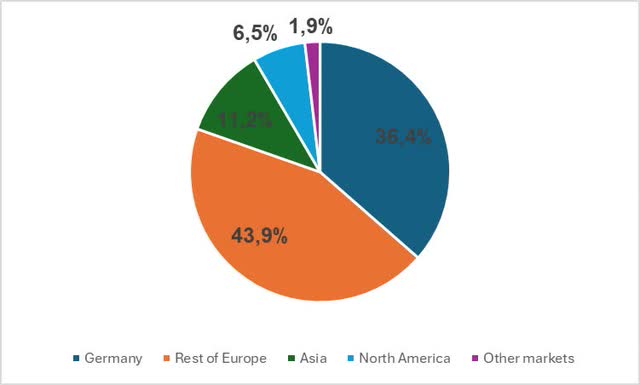

Porsche Holding generates the vast majority of its gross sales in Europe (80.4%), nevertheless it additionally has an publicity in Asia (11.2%) and North America (6.5%).

Firm’s information

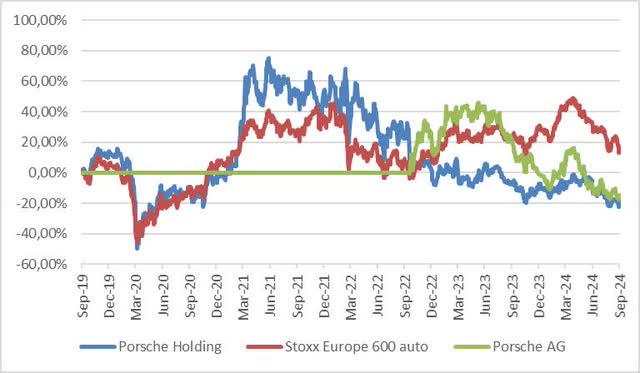

Having reached its highest worth since 2008 in June 2021, the inventory entered a downward pattern, underperforming the Stoxx Europe 600 Auto Index by practically 60%.

RadaEcoWatch calculations

This underperformance started after Porsche AG’s IPO in September 2022. Previous to this, Porsche Holding was the only manner for buyers to achieve publicity to premium world automotive producers that weren’t publicly traded. Following Porsche AG’s itemizing, buyers gained the power to take a position straight within the firm’s two foremost property, Volkswagen and Porsche AG, with out utilizing the holding firm.

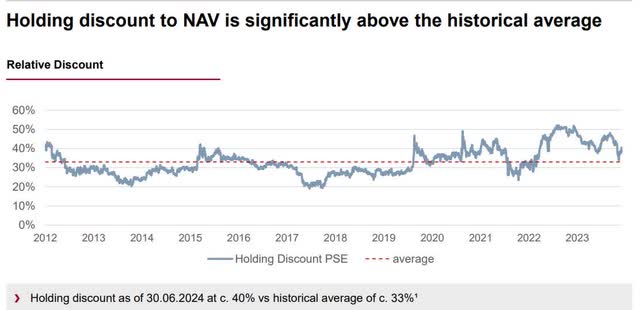

Consequently, the NAV low cost widened, reaching 50% by the tip of 2023, primarily based on the corporate’s estimates. As of June 30, the low cost stood at 40%, in comparison with a long-term common of 33%.

Firm’s investor presentation

We now consider that buyers will primarily give attention to Porsche Holding’s dividend, primarily based on the earnings generated by its two working subsidiaries. As a result of holding low cost, the corporate has the potential to supply greater dividend yields. Nevertheless, within the quick time period, the corporate’s EUR 5 billion debt may cut back its payout. Based mostly on 2024 consensus estimates, Porsche Holding is predicted to pay a 6.4% dividend yield, in comparison with 8.5% for Volkswagen and three.2% for Porsche AG.

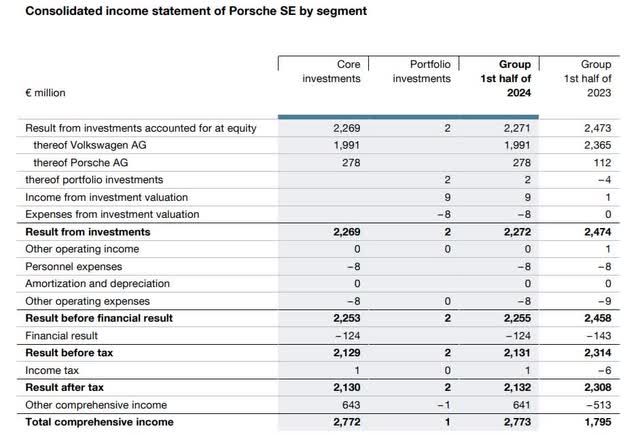

In H1 2024, Porsche Holding’s funding revenue declined from EUR 2.474 billion in H1 ’23 to EUR 2.271 billion, with each Volkswagen (from EUR 7.5 billion to EUR 6.4 billion) and Porsche (from EUR 2.8 billion to EUR 2.2 billion) posting weaker outcomes after tax and non-controlling pursuits.

Firm’s H1 steadiness sheet

Funding thesis

Though Porsche Holding’s present inventory valuations could seem very engaging (2024 P/E estimate of two.6x), we consider it is going to proceed to face destructive pressures from the worsening outlook for the car market.

We count on the latest indicators of financial softening within the USA and Europe, in addition to continued weak spot in China, to weigh on the auto sector’s efficiency. The graph beneath reveals that the European auto sector’s efficiency is carefully correlated with the German IFO enterprise confidence index, which stays at traditionally low ranges. This means a possible destructive pattern for the sector within the coming months.

RadaEcoWatch

We foresee continued downward revisions in earnings estimates for Volkswagen and Porsche AG as the principle dangers for his or her shares over the following few years.

For Volkswagen, each US and European gross sales might be hit by an financial slowdown and rising inventories, leading to decrease revenue margins. Gross sales in China may additionally stay weak, as highlighted by BMW’s latest revenue warning. Moreover, Volkswagen could proceed shedding market share to native rivals, notably within the electrical car sector. Volkswagen’s market share in China fell from 19.3% in 2020 to 14.5% in 2023, and its objective of sustaining a 15% share by 2030 appears overly formidable on this atmosphere. The necessity for larger funding in electrical autos, to maintain tempo with Chinese language rivals and meet European regulatory necessities, additional weighs on the corporate’s outlook.

Porsche can also be affected by a slowing automotive demand over the approaching quarters. Nevertheless, the launch of latest fashions in H2 2024 may present some assist to gross sales. Porsche’s July 2024 steering revision (income of EUR 39-40 billion, down from EUR 40-42 billion, and return on gross sales of 14-15% down from 15-17%) as a result of provide chain points could proceed to have an effect on its efficiency. Within the medium time period, the impression of R&D prices associated to electrical autos will want cautious monitoring. Though average income progress is predicted (pushed by new electrical fashions and rising markets), rising prices may compress revenue margins, difficult Porsche’s potential to satisfy buyers’ revenue progress expectations.

Valuation

We expect that buyers will give attention to the corporate’s dividend going ahead, so we worth Porsche Holding utilizing a dividend low cost mannequin primarily based on the next assumptions:

– Unchanged dividend within the interval 2024–2026 at USD 0.28, according to consensus estimates, to facilitate the corporate’s debt discount course of.

– A 6% annual progress within the following 7 years to mirror the constructive results of debt discount.

– A 3% perpetual progress price.

– A ten% value of capital, according to the corporate’s assumptions in H1 24 impairment exams.

It offers a inventory valuation of USD 4.73/share, implying an 8.7% upside potential.

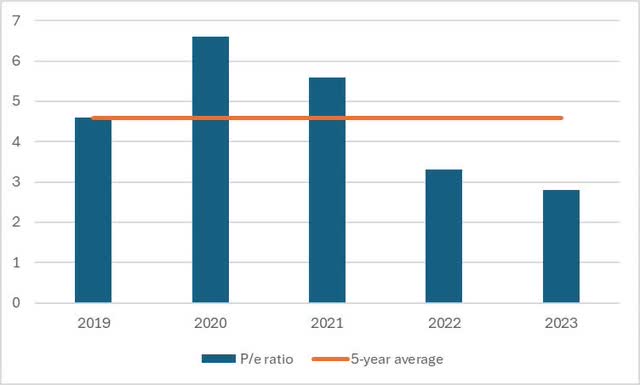

A a number of evaluation reveals the same upside potential. The 2024 estimated P/E is 2.6x, in comparison with a 5-years common of 4.6x. Nevertheless, in comparison with the final two years P/e quantity (3.3x in 2022, 2.8x in 2023) the change is proscribed. At a goal P/E ratio of three.0x, the inventory upside potential could be barely greater than 10%.

Firm’s information, RadaEcoWatch

The view from The Avenue

The analysts’ view on Porsche Holding is break up, with 5 ranking it purchase, and 6 ranking it maintain. Regardless of the inventory’s marked decline since 2021 and a big goal value discount (from EUR 115.18 at 2021-end to the present EUR 53.95), no analysts have a SELL advice on the inventory.

Conclusion

Porsche Holding’s shares could seem engaging with an estimated 2024 P/E a number of of two.6x, considerably decrease than the 5-year common. Nevertheless, we consider the corporate faces a number of short-term dangers, together with slowing gross sales, in addition to medium-term dangers comparable to elevated investments in electrical autos and rising competitors from Chinese language rivals. These components may result in additional downward revisions in estimates for the approaching years. The DDM evaluation reveals restricted upside potential except there’s a sturdy enchancment in long-term progress prospects.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

[ad_2]

Source link