[ad_1]

jamesbenet

Procept Biorobotics (NASDAQ:PRCT) has been one of many strongest performers within the medical machine house over the previous yr. The corporate has a novel product offering reduction to older males affected by BPH – benign prostatic hyperplasia. The minimally invasive process is seeing robust progress as each system gross sales and procedures develop considerably. I wrote in regards to the firm in Could 2023 when it traded at $31.40 – a 142% acquire since. Procept nonetheless has good potential with a brand new and improved system named HYDROS now FDA authorised, permitting for an additional leg of progress within the quarters to come back. Whereas PRCT has good potential, it’s nonetheless at a small scale and buying and selling a premium valuation, giving it excessive danger into 2025. Let’s dive into the latest outcomes and new approval potential for Procept.

Improved AI-powered Hydros System authorised

The corporate took their time engaged on the system, with data gained in 50,000 procedures to enhance any level factors a physician could have. The product has AI powered FirstAssist expertise to create a process plan. The picture has been improved, and the steps have been streamlined to make it simpler for physicians to make use of successfully. The FDA authorised the platform on August twenty first permitting the corporate to start critically promoting the product. Sadly, we do not have actual launch particulars for the reason that approval was after the latest earnings name in August. Nevertheless, you’d hope the launch could be rolling considerably in 2025 and assist vital 2025 income progress. Present estimates are for 40% income progress in 2025, which is already a excessive bar to clear in a troublesome working setting. Nevertheless, Hydros might permit for upside to this quantity, with 2026 prone to see even stronger progress because of this.

On the Wells Fargo convention on September 4th, administration identified the numerous enhancements in options. The launch is not going to have a adverse influence on gross margins. The preliminary technique is to deal with 2700 greenfield hospitals within the US that do remedy and never change older methods. 860 of these hospitals do 70% of the quantity, and PRCT expects to be in nearly all of these hospitals within the coming years. The system will value $380,000 within the second half of 2024 with that to extend probably in 2025. New surgeons needs to be prepared to come back onboard over the primary system because of the enhancements, serving to to enhance utilization. Q3 can have some small disruption as gross sales reps are educated on the brand new system with This autumn principally at full pace of gross sales. Total the improved system will principally be an enormous tailwind to 2025 with a lot of the legacy methods to stay in place with rising utilization.

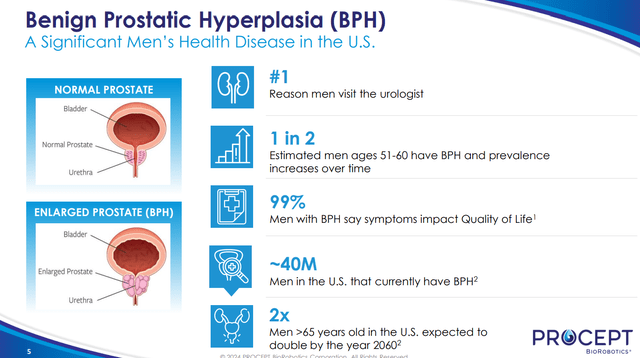

BPH in Males (PRCT IR)

Q2 – Continued hypergrowth

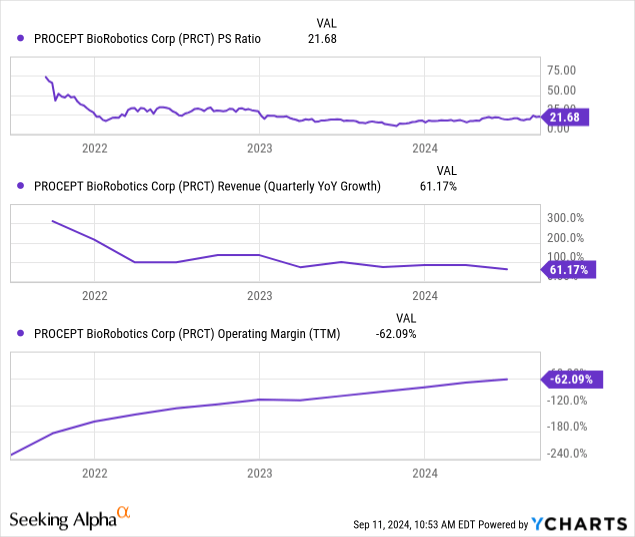

Procept has continued to scale its enterprise fairly rapidly, with spectacular income progress. They proceed to promote their present Aquablation system with a robust cadence, with 47 gross sales of recent methods within the quarter. The position of methods is crucial to the upper margin gross sales of handpiece revenues, making it the perfect main indicator of future progress. Final yr, they bought 40 in Q2, for a progress fee of 17.5% y/y in new methods. Consumable income was up 101% y/y, however the base remains to be fairly small with $27.3m income. 8000 hand items had been shipped in Q2, with a 15% improve in system utilization y/y. This could enhance drastically with HYDROS as newer physicians can be drawn to the better to make use of interface, superior expertise and ease of use by way of AI help. As process volumes at every system placement improve, income will proceed to scale together with margins. Complete gross margin is as much as 59%, up from 56% from 2023 on the improved mixture of procedures versus system deployments. On the draw back, because of the persevering with ramp of gross sales and advertising and marketing, the corporate is making vital losses with -62% working margin enhancing over time. Long run, the corporate is making an attempt to deal with prostate most cancers, with potential for an enormous market there if they’ll succeed of their present scientific trial on their older Aquablation system.

Dangers

Procept is small with just one space of experience in the mean time with its BPH merchandise specializing in massive unmet want. The big TAM with many males experiencing points with their prostate offers the corporate vital runway on this first indication. Nevertheless, after that, the following space for the corporate stays unclear and can stay so for a number of years. Additionally, the corporate remains to be making sizable losses because it grows its analysis and gross sales organizations to assist future progress. The corporate has $214m in money available, with a 2024 loss anticipated to be $97.5 million. Nevertheless, a few of that’s dilution by way of stock-based compensation to an inexpensive variety of workers to gasoline progress. A future fairness dilution to lift extra money is feasible, particularly with the excessive value of a debt issuance for a smaller firm proper now. This does put a possible damper on shares in some unspecified time in the future in 2025 as a risk.

Maintain – Procept shares pretty valued

Procept shares noticed a major increase after HYDROS was authorised, with pleasure from the road on the following leg of progress. The long-term potential might enhance if prostate most cancers finally ends up a possible market down the street. Shares are actually buying and selling close to all-time highs with a value of $76 pricing in robust progress in 2025 of 40%. Hydros adoption ought to give potential upside to the steerage subsequent yr, however gross sales modifications might trigger disruptions as nicely in coming quarters. Nevertheless, long-term scaling of the enterprise is the largest query, and the present valuation doesn’t go away a lot room for error on the present value. We’ve seen different firms within the medical expertise house see their multiples contract considerably as soon as they attain the $300 to $500 million mark. Thus, I’ve the shares at a maintain on the present time, till a pullback happens to present buyers a extra favorable entry value.

[ad_2]

Source link