[ad_1]

MAGNIFIER

About 10 days in the past, Scorpio Tankers Inc. (NYSE:STNG), one of many largest product tanker operators on the planet, launched its Q2-2023 outcomes displaying sturdy figures. On this article, I’ll present an evaluation of the Q2-2023 earnings and I’ll clarify why I consider Scorpio Tankers is an efficient BUY alternative.

In case you are excited about tanker firms, I additionally cowl Teekay Tankers and Worldwide Seaways.

About Scorpio Tankers

Based in 2009, Scorpio Tankers is without doubt one of the leaders within the worldwide marine transportation of refined oil merchandise. Based mostly in Monaco and listed on the NYSE, Scorpio Tankers has a contemporary fleet of 112 vessels with a median age of seven.5 years. Notably, the fleet consists of 14 Handymax, 59 MR and 39 LR2. As well as, 87 Scorpio Tankers’ vessels are outfitted with the scrubber mechanism that’s wanted to eradicate sulfur and nitrogen oxides from the exhaust gases, thus making the fleet extra sustainable from an environmental viewpoint.

Inventory worth

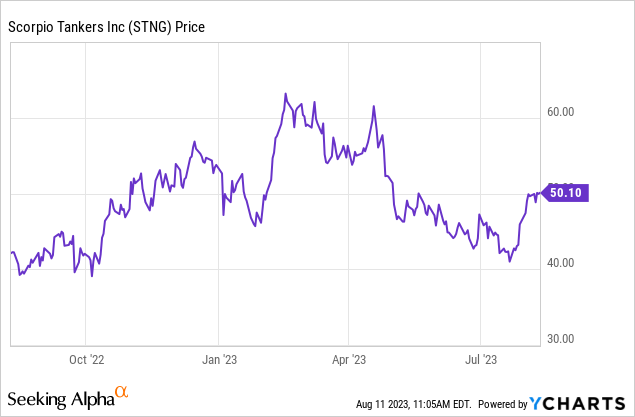

The inventory is at the moment buying and selling at $49.9/share, equal to a market cap of $2.59 B, and is up 18.6% year-on-year whereas, for the reason that starting of the 12 months, Scorpio Tankers misplaced about 7%. The 52-week minimal was touched on October fifth, 2022, at $39.1/share whereas the 52-week most was recorded within the early months of this 12 months at $63.2/share (February sixteenth, 2023).

Q2-2023 outcomes

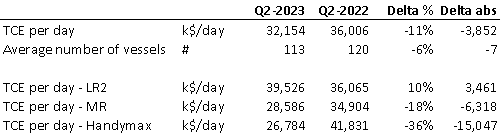

Scorpio Tankers generated revenues of $329 M in Q2-2023, down 19% from the $405 M generated in the identical quarter of the earlier 12 months. The discount in revenues could be defined by time constitution equal (TCE) charges that have been 11% decrease year-on-year (from $36k/day in Q2-2022 to $32.1k/day in Q2-2023) and by the discount within the common variety of working vessels (from 120 in Q2-2022 to 112 in Q2-2023). As could be seen from the chart beneath, charges dropped among the many MR class vessels (-18%) and Handymax (-36%) whereas LR2 was the one class that noticed a rise in TCE day charges, from $36k/day to $39.5k/day.

Scorpio Tankers

Complete working expenditure decreased by 10% (or $17 M) year-on-year to $158 M. The most important value objects have been vessel working prices ($79 M, up 3% y-o-y on account of inflationary stress) and depreciation ($51 M, steady y-o-y). G&A elevated 19% to $27 M principally on account of an increase within the amortization plan of restricted inventory awards.

Since revenues decreased greater than prices, EBIT was down 26% to $171 M. Throughout Q2-2023, Scorpio Tankers reported a web revenue of $132 M, down 31% year-on-year.

Money movement from operations for the primary six months of the 12 months was optimistic at $501 M, whereas money movement from investing was destructive at -$12 M on account of investments carried out in vessel gear equivalent to scrubbers and ballast water therapy programs. Money movement from financing was destructive at -$552 M for the reason that firm carried out some initiatives to restructure its capital and scale back its debt publicity. Particularly, there was a repurchase of frequent inventory for a complete of $399 M, compensation of debt of $260 M adopted by new debt issuance ($391 M) at a decrease rate of interest. The aim of this refinancing is to scale back Scorpio’s value of debt, releasing up capital for different value-added initiatives. On the finish of Q2-2023, Scorpio Tankers’ web debt is $1.4 B, about $100 M lower than the $1.5 B of the earlier quarter.

Shares repurchase program

As talked about above, Scorpio Tankers carried out a big share repurchase program that began in July 2022 and, thus far, led to the repurchase of 12.5 M shares price $582 M. The rationale behind this share repurchase program is that Scorpio’s administration believes that the corporate is buying and selling at a reduction to its NAV and subsequently it prefers shopping for again shares relatively than paying out dividends.

Refined product tanker market

The refined product tanker market was disrupted originally of 2022 with the primary rumors a few potential Russian-Ukrainian battle. Since then, day charges for oil and refined product tankers rallied to ranges by no means seen earlier than on account of sanctions imposed on Russian oil that utterly modified the oil distribution dynamics world wide. Since Q1-2022, excessive TCE charges have supported sturdy FCF era for many of the tanker firms, together with Scorpio Tankers, and I consider that the FCF bonanza is way from over.

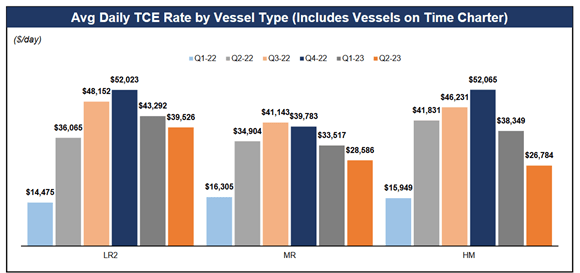

Despite the fact that charges are steadily declining, they’re nonetheless at extremely excessive ranges as could be seen from the image beneath.

Scorpio Tankers

From my viewpoint, charges will stay at the next stage than these of Q1-2022, thus guaranteeing a shiny future for refined product tanker firms, for various causes.

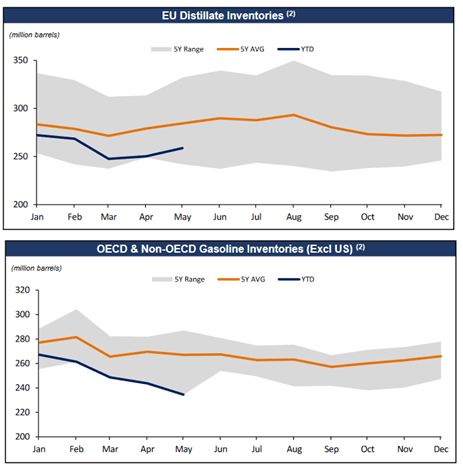

To begin with, each day demand for refined merchandise in H2-2023 is predicted to exceed 2022 demand by about 2 or 3 Mbbl/day reaching 70.6 Mbbl/d in This autumn-2023. Demand progress shall be principally supported by China’s restoration after COVID lockdowns and by the EU which wants to exchange refined merchandise that it had been sourcing from Russia. As well as, international inventories of refined merchandise are at low ranges (see image beneath) resulting in an elevated demand for seaborne refined merchandise from international locations with greater inventories to international locations with decrease ranges. Nevertheless, the provision of tankers is at the moment restricted and even sooner or later it won’t enhance an excessive amount of since order books for new-built vessels are at traditionally minimal ranges. So as phrases, whereas demand for tankers is growing, provide is scarce. These dynamics are more likely to assist excessive tanker charges for the following quarters.

Scorpio Tankers / IEA

Dangers

One of many foremost dangers to which Scorpio Tankers is uncovered is represented by oil (and refined merchandise) demand developments. As of in the present day, IEA forecasts a rise in oil demand for the following years (which might be good for tanker firms), nonetheless, because the COVID pandemic has taught us, even essentially the most surprising occasion might grow to be actuality. Regardless of the chance of a disruptive occasion of a magnitude like COVID is low, it can’t be utterly excluded.

The opposite related danger I see for Scorpio is related to potential environmental points, both on account of stricter laws on CO2 emissions or on account of potential refined product leaks with consequent environmental damages and prices to incur.

Nevertheless, as talked about originally, Scorpio’s vessels have a median age of seven.5 years and are fairly trendy thus limiting the danger of incidents and CO2 emissions.

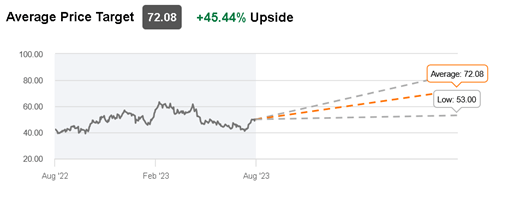

Goal Value

Scorpio Tankers is at the moment coated by 11 fairness analysis analysts. Ten of them have offered a purchase (2) or sturdy purchase (8) score whereas just one has issued a maintain suggestion. The common goal worth forecast from analysts is $72/share, which might indicate a forty five% upside versus the present inventory worth.

In search of Alpha

Conclusion

I consider that Scorpio Tankers is an attention-grabbing purchase alternative because it operates in an trade that’s benefiting from favorable dynamics. Throughout the trade, Scorpio distinguishes itself from friends for having a big and trendy fleet that may enable the corporate to reduce capital expenditure within the subsequent years. From a monetary viewpoint, Scorpio Tankers is a sturdy firm and administration has been working to scale back the leverage and enhance the stability sheet. On the present worth of $49.9/share, Scorpio Tankers is a purchase.

[ad_2]

Source link

{kind=link}