[ad_1]

JHVEPhoto

Funding Thesis

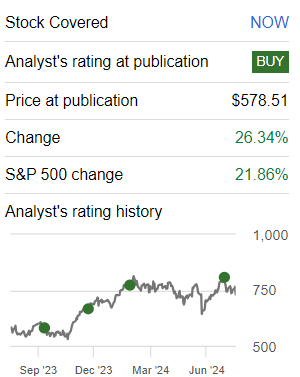

ServiceNow (NYSE:NOW) (NEOE:NOWS:CA) delivered an earnings report that was met with cheer from buyers, as its inventory jumped 6% premarket. However particulars matter. I assert, as I’ve executed earlier than, that ServiceNow is on the trail towards turning into a megacap inventory, a family title.

Certainly, I argue that buyers are getting a particularly reasonable entry worth proper now whereas paying 35x subsequent yr’s free money circulate. ServiceNow shouldn’t be solely delivering +20% premium progress, however it’s able to sustaining this progress within the medium time period. What’s extra, its steadiness sheet has substantial monetary sources, which offer this inventory with an added margin of security.

All in all, I stay steadfast in my view that ServiceNow is a purchase.

Speedy Recap

Final month, I stated,

It is a giant cap, on the trail in the direction of being a mega-cap. Traders are usually not going to seek out this kind of inventory on sale. ServiceNow is an organization with robust prospects, that provides buyers peace of thoughts. And that comes at a excessive worth.

Writer’s work on NOW

And that succinctly explains my thesis. ServiceNow goes to develop into a megacap inventory. I am a powerful believer on this assertion. There shall be minor blips alongside the way in which, however this inventory will not go on sale for lengthy. Consequently, on the again of this earnings report and improved steering, I reiterate my stance on this title.

ServiceNow’s Close to-Time period Prospects

ServiceNow gives cloud-based software program options designed to assist companies handle digital workflows. It permits organizations to streamline operations throughout numerous departments similar to IT, human sources, and customer support by automating routine duties and processes. ServiceNow’s platform incorporates GenAI to reinforce effectivity and productiveness, making it simpler for companies to deal with advanced workflows.

Within the close to time period, ServiceNow’s prospects seem robust. The corporate reported strong progress in subscription income and notable success in new product launches, notably its AI-driven options like Now Help. With elevated adoption throughout numerous industries and spectacular efficiency metrics, ServiceNow is poised for continued enlargement.

Nonetheless, ServiceNow faces challenges too. The enterprise software program market is extremely aggressive, with quite a few gamers vying for dominance throughout numerous segments similar to cloud computing, AI, and workflow automation. Main rivals embody tech giants like Microsoft (MSFT), Salesforce (CRM), and Oracle (ORCL), which additionally provide complete suites of enterprise options.

Given this balanced background, let’s now focus on its fundamentals.

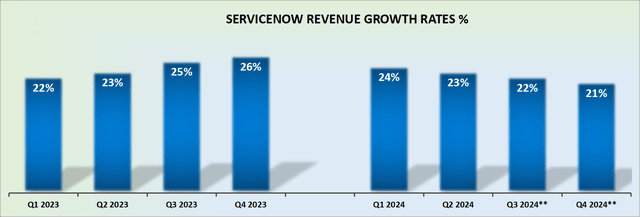

Income Progress Charges Level to 23% CAGR in 2024

NOW income progress charges

ServiceNow has upwards revised its steering for 2024 by $10 million out of $10 billion, or a morsel. But it surely’s sufficient to verify to buyers that ServiceNow has what it takes to ship premium progress. Premium progress means regular, constant, predictable, and dependable progress of greater than 20% CAGR.

To be clear, it is not a lot that ServiceNow raised its steering right here that issues, however slightly that it did not pull again on its steering, as many IT-related SaaS firms have been making noises concerning the powerful macro setting and struggling to satisfy the guides they set out earlier within the yr.

Evidently, that is not the case with ServiceNow. And this has implications with regards to the premium buyers who’re prepared to pay for the inventory. A inventory with a powerful constructive narrative, with a plan to succeed in $15 billion whereas delivering +20% CAGR, is few and much between. The truth is, in my thoughts, I depend fewer than 5 names (however I could also be unsuitable). Given this context, let’s now focus on NOW’s valuation.

NOW Inventory Valuation — 35x Subsequent 12 months’s Free Money Stream

Earlier this month, I wrote,

Supposing ServiceNow can increase its free money circulate margin by 100 foundation factors subsequent yr, to 32%, this could see ServiceNow delivering roughly $4.3 billion in free money circulate [next year].

Provided that we’re midway by means of 2024, and ServiceNow has already raised its full-year steering for its working earnings by 50 foundation factors, this means that the again finish of 2024 shall be extra worthwhile than buyers beforehand anticipated.

Therefore, this confirms my competition that ServiceNow is greater than more likely to increase its adjusted free money circulate margin by 100 foundation factors subsequent yr.

Due to this fact, listed below are my tough assumptions, ServiceNow grows its prime line subsequent yr by 22% whereas increasing its free money circulate margin to roughly 32%, this could see about $4.3 billion on the playing cards exhibiting up in some unspecified time in the future in 2025. Even when this determine is not hit in 2025, ServiceNow will assuredly be on this path by means of 2025 into 2026.

On prime of that, ServiceNow holds roughly $4 billion of web money, not together with the roughly $3.5 billion of long-term investments. In different phrases, buyers have a excessive free money circulate producing enterprise, with a rock-solid steadiness sheet, in a well-positioned space of the market. Paying 35x subsequent yr’s free money circulate for ServiceNow strikes me as an affordable entry level for brand spanking new buyers to this title.

The Backside Line

Paying 35x subsequent yr’s free money circulate for NOW is smart for brand spanking new buyers because of the firm’s robust progress trajectory, strong monetary well being, and skill to maintain +20% premium progress in a extremely aggressive market.

With its strong steadiness sheet and substantial monetary sources, ServiceNow gives a margin of security that enhances its attractiveness. Furthermore, the corporate’s strategic place and modern AI-driven options set it on a path towards turning into a megacap inventory. Thus, getting into at this valuation affords a good alternative to put money into a high-potential, industry-leading enterprise software program supplier.

ServiceNow’s progress trajectory ensures that buyers will “now” be within the service of spectacular returns.

[ad_2]

Source link