[ad_1]

Iryna Tolmachova/iStock Editorial through Getty Photographs

In my earlier evaluation of Suncor Power (NYSE:SU) (TSX:SU:CA), I targeted on the corporate’s transformation below the brand new administration and the numerous potential I noticed within the inventory. At that time, I used to be arguing that the market had not given credit score to Suncor for its formidable turnaround story, and my PV12.5 valuation urged a ~30% upside. Since then, the oil costs are down from ~US$80 to ~US$75 WTI, whereas the shares of Suncor are buying and selling greater. The turnaround story up to now has been unveiled very positively, with nice quarterly updates and bullish information from administration addressing additional enhancements in efficiencies, greater manufacturing development, and strict budgeting.

On this replace, I’ll give attention to the latest developments in Suncor’s cost-cutting plan, overview the spectacular Q2 outcomes, and supply an up to date valuation with sensitivity evaluation.

Price Financial savings Plan

Suncor’s new administration, led by CEO Wealthy Kruger, has been laser-focused on operation and value effectivity, which is important for long-term success. In my earlier evaluation, I anticipated price reductions of C$5 per barrel.

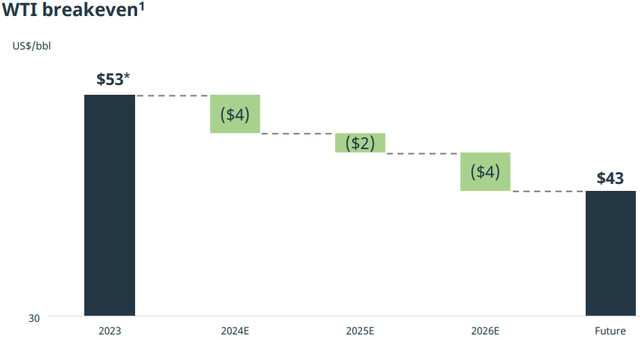

Goal breakeven (Suncor Traders Presentation)

When Suncor’s administration offered a objective to decrease breakeven by US$10 throughout their Might presentation, my jaw actually dropped. I initially questioned the feasibility of aggressive price cuts, given the necessity to enhance the protection requirements and fame of the corporate on this matter. Nonetheless, after digging deeper, it grew to become clear that these financial savings come from a mixture of upper manufacturing scale, strategic upfront Capex investments, and a collection of optimizations throughout the board with no dangers of potential security hazards.

Moreover, the corporate is finalizing its deleveraging. It can quickly hit its debt goal of C$8B, which can decrease its curiosity funds, and with an ongoing share-buyback program, there can be fewer shares, decreasing its dividend bills.

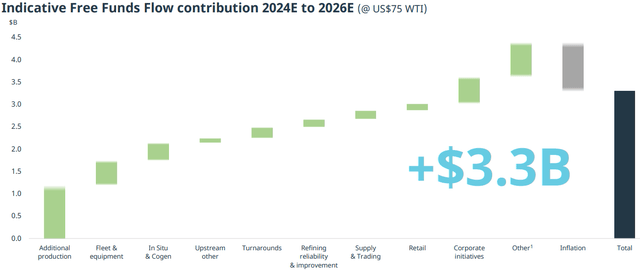

Price-cuts contributions (Suncor’s presentation)

The graph above illustrates the varied initiatives throughout the corporate departments which are anticipated to drive the Free Funds Stream by ~C$3.3B from 2024 to 2026 (assuming US$75 WTI). These initiatives embrace:

Further Manufacturing: Enhance in manufacturing throughput by 100k bbls/d, enhance effectivity in core oil sands operations. Fleet & Tools: Past autonomous vans, Suncor is investing in additional environment friendly tools, which reduces operational prices and will increase reliability. In Situ & Cogeneration: Enhancements in in-situ operations and cogeneration tasks that enhance power effectivity and scale back working prices. Turnarounds: Suncor is streamlining its turnaround processes, as highlighted by Shelley Powell, who talked about, “It is a new strategy to what we name risk-based inspection. It has allowed us to take a good quantity of labor out of the turnaround with out including any extra threat.” Refining Reliability & Enchancment: Upgrades to refining processes that improve effectivity and scale back downtime, contributing to greater margins. Provide & Buying and selling: Optimization in provide chain administration and buying and selling methods that seize worth from market alternatives. Retail: Enhancements in retail operations, driving greater margins and buyer satisfaction. Company Initiatives: Firm-wide initiatives aimed toward decreasing overhead and administrative prices. Different & Inflation: Mitigating the affect of inflation via effectivity positive aspects in numerous areas.

These initiatives should not solely about slashing prices however about making a extra agile group that may shortly react to adjustments in market circumstances and ship excellent returns for its shareholders.

We are able to already see the enhancements in Q2 outcomes.

Operations

Suncor’s Q2 outcomes solidify the corporate’s turnaround story and place it among the many leaders in oil sands operators. Suncor reported robust manufacturing of 771k bbls/d and refinery throughput of 431k bbls/d, reflecting the robust momentum that Suncor has been constructing all year long.

Wealthy Kruger summarized the quarter’s achievements throughout the earnings name: “The second quarter was about execution and momentum. Excessive-quality execution of main upstream and downstream turnaround actions and sustaining momentum in focused enchancment priorities, together with operational reliability and value administration.”

The refining utilization hit a formidable 92% in Q2 regardless of deliberate turnarounds at its Sarnia and Montreal refineries. Downstream operations achieved document refined product gross sales of 595k bbls/d, surpassing the earlier document set in 1Q24, additional solidifying shareholders’ belief within the turnaround story.

Financials

Financially, Suncor generated C$3.4B in AFFO and C$1.4B in FCF and returned over C$1.5B to shareholders via share repurchases and dividends, reflecting the dedication to shareholder returns. As Kris Smith, Suncor’s CFO, famous, “Our laser give attention to prices continued with whole working promoting and basic bills of $3.2 billion within the quarter, which is down over $250 million from Q1.” This constant give attention to price administration, coupled with robust operational efficiency, positions Suncor nicely for a sturdy second half of 2024.

The Affect on the Valuation

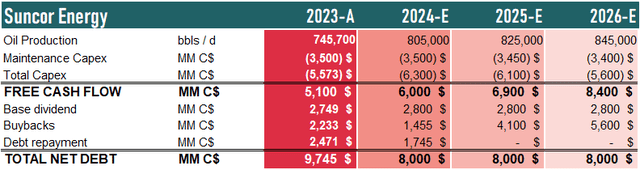

Throughout the Might presentation, administration supplied detailed steering as to what manufacturing, money stream, and Capex we will count on over the following three years. I constructed a easy mannequin primarily based on this steering. (Notice.: 2023 numbers should not precise however normalized).

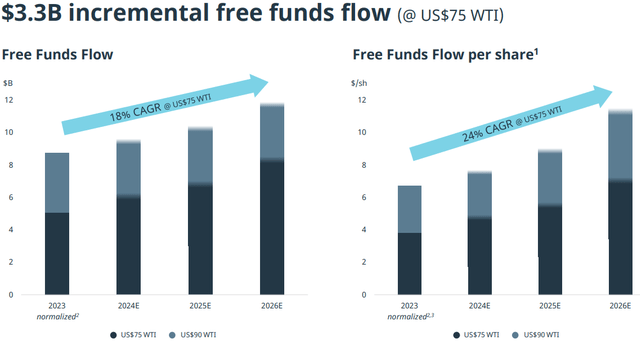

24% FCF CAGR (Suncor’s Presentation)

As a result of mixture of cost-savings, discount in share depend, and enhance in manufacturing output, Suncor expects to attain a 3-year CAGR of 24% in free money stream per share from 2023 normalized numbers, assuming US$75 WTI.

Writer’s mannequin (Based mostly on Suncor’s steering)

The corporate is anticipated to attain its debt goal within the first half of subsequent yr. (It is likely to be even this yr if WTI averages over US$75.) Every thing above the bottom 4% dividend yield can be pointed in direction of the discount of shares excellent. To this point, with the speed of change in Suncor, I see this projection as being conservative. Throughout the Q2 name, Kruger emphasised, “We’re exceeding our fee of anticipated enchancment on the amount aspect of it… and we’re fairly happy with the elemental efficiency of the group on these components that we will management.

For my valuation, I’m merely discounting the ensuing dividends and buybacks. Within the last yr, I’m discounting a “sustainable free money stream”, which is deliberate FCF+Development Capex, and pretending that the corporate switches to a 100% payout ratio with no spending for development or any additional price effectivity enhancements.

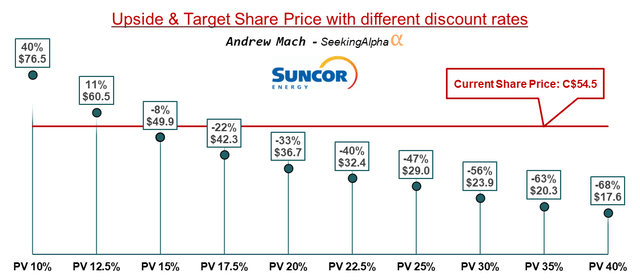

DCF with totally different low cost charges (Writer’s mannequin)

Discounting with totally different low cost charges reveals me that Suncor is presently priced for ~14% annual returns going ahead if the WTI stays flat at US$75.

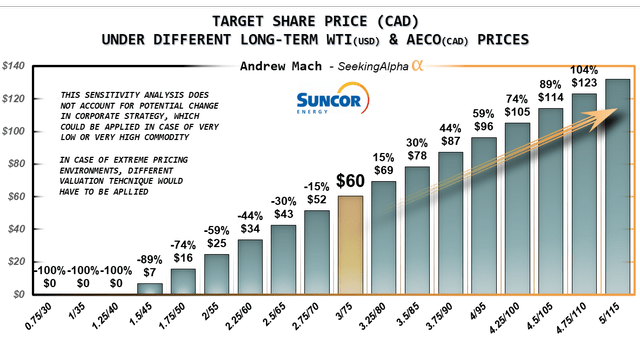

Affect of various oil costs

To grasp the primary threat, it is important to contemplate how an organization’s profitability is impacted by oil worth fluctuations. Given Suncor’s built-in enterprise mannequin that mixes forth upstream manufacturing and downstream refining, the corporate is comparatively resilient to the volatility in crude costs.

Every US$5 transfer in WTI costs strikes the worth of future free money flows by ~15%, which is brought on by low breakeven prices. In Might’s presentation, Administration said that their present breakeven prices are ~C$53. After additional commentary, you’ll be able to see that they calculate the breakeven price with the bottom dividend included. This reveals that administration does not contemplate dividends as one thing non-obligatory; they merely account for them as non-negotiable prices. Approx. C$10 from every barrel offered goes in direction of dividends. In my sensitivity evaluation, I’m defining breakeven as a degree earlier than the dividend funds. That is presently sitting at ~US$46 WTI, however because of the cost-cutting measures, it’s anticipated to drop to ~US$36 WTI.

Sensitivity evaluation (Writer’s mannequin)

For comparability, we will have a look at the opposite aspect of the spectrum, the place the FCF of Surge Power (SGY:CA) strikes by ~30% with a US$5 transfer. Traders wish to name it as having a torque to the oil worth. What it actually means is low-margin, higher-risk play with greater potential if oil costs rise.

Closing Ideas

Based mostly on the present trajectory, Suncor is nicely positioned to succeed in its objective of ~C$7 FCF per yr by 2026. The inventory may commerce at 10-12x FCF, making it a C$70-84 (US$50-60) inventory. As Suncor continues to execute its turnaround story, decreasing its breakeven prices and enhancing its FCF, the market will seemingly comply with and acknowledge the total worth of those enhancements, resulting in a re-rating of the inventory.

In conclusion, the turnaround has nice momentum, and the give attention to effectivity is driving substantial worth creation. With strong Q2 efficiency and a transparent path to additional enhancements, Suncor nonetheless stays a Sturdy Purchase with vital upside potential over the approaching years. In my view, traders who imagine within the turnaround story ought to contemplate including Suncor to their portfolio earlier than the market absolutely costs in these optimistic developments.

[ad_2]

Source link