[ad_1]

Henrik5000

By Carrie King

This fall earnings revealed a story of two markets within the U.S., with tech and web gamers hitting house runs as different sectors and industries performed small ball compared.

But, Basic Equities investor Carrie King sees the market broadening within the quarters forward, opening up a wider taking part in discipline for inventory pickers.

Dispersion on show

S&P 500 earnings have been optimistic for a second consecutive quarter, with the lion’s share of This fall progress powered by the tech and web shares that led markets larger in 2023.

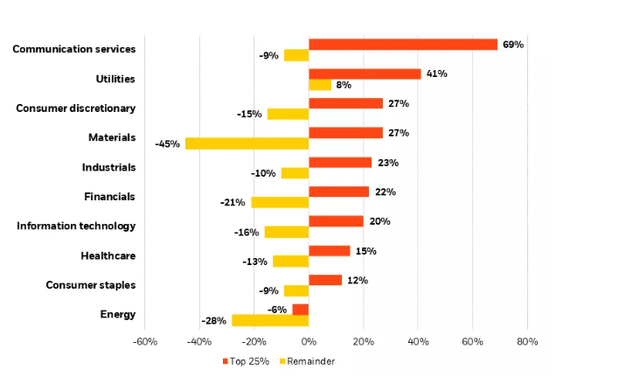

Earnings progress of 4.4% on the index stage masks dispersion in year-over-year (YoY) outcomes not solely between sectors, however inside them.

Client discretionary (+52%) and communication providers (+43%), collectively holding 4 of the “Magnificent 7” mega-cap shares, have been This fall standouts. Power (-25%) and supplies (-20%) have been the primary laggards as commodities costs fell with moderating inflation.

Healthcare, considered one of our favored sectors, noticed destructive earnings as effectively, but this was pushed by solely 4 names in a class that features greater than 50.

This illustrates the differentiation we’re seeing inside sectors (see chart beneath) in addition to the significance of inventory choice to parse potential winners and losers and maximize a portfolio’s return prospects.

Whereas earnings dispersion shouldn’t be new or surprising, we consider it may be extra informative in an surroundings the place firm fundamentals could also be poised to drive extra worth motion after an prolonged interval during which macro considerations dominated markets.

Uneven earnings

Yr-over-year earnings progress by sector, This fall 2023

Supply: BlackRock Basic Equities, with knowledge from Refinitiv and FactSet, Feb. 22, 2024. Information displays earnings outcomes with 421 S&P 500 corporations (86.5% of market cap) reporting. The chart reveals common yoy earnings progress for the highest quartile of earners in every sector and the common for the rest of constituents in every sector. Previous efficiency shouldn’t be indicative of present or future outcomes. Indexes are unmanaged. It isn’t attainable to take a position instantly in an index.

Broadening past tech-plus

Earnings expectations for the so-called tech-plus shares which have been driving market returns since final 12 months have been exceptionally excessive – and but they surpassed even that lofty bar.

Wholesome income progress plus a price base that was “right-sized” in 2023 contributed to the sturdy outcomes. Yr-over-year comps additionally weren’t laborious to beat after a dismal 2022.

We nonetheless like tech shares and anticipate momentum from generative AI to proceed powering earnings progress. But the most important numbers are in all probability in, with comps getting more durable and earnings prone to decelerate from This fall’s very sturdy ranges.

In the meantime, we see motive to consider that earnings progress for the rest of the S&P 500 may decide up. The know-how sector broadly has been experiencing a distinct enterprise cycle than the remainder of the market.

Bloated investing and hiring throughout the COVID-induced digitization of every little thing in 2020 and 2021 was adopted by a reining in and normalization in 2022 and 2023.

Different sectors have been having the alternative expertise, struggling throughout COVID and nonetheless re-adjusting upward right now. Healthcare procedures and journey plans that have been delayed throughout the pandemic are again on and shoppers are nonetheless taking part in catch-up on missed experiences.

This fall outcomes for motels, eating places and leisure confirmed 88% YoY earnings progress and revenue margins which are simply now returning to pre-COVID ranges.

One main lodge chain famous their expectation for slower however nonetheless rising leisure revenues into 2024. We’re watching the buyer carefully, given pockets of stress that we famous final quarter, and are acutely attuned to the influence that larger rates of interest are having on wallets and buying choices.

The instance in EVs

This fall earnings supplied one notable instance of the place shoppers are rising extra guarded – available in the market for electrical autos (EVs). The EV chief within the Magazine 7 was the one identify within the group to put up destructive YoY earnings progress within the quarter.

One other main U.S. EV producer famous in its earnings name “the influence of traditionally excessive rates of interest” on demand whereas additionally saying job cuts.

To make sure, the impact of upper charges on whole buy worth shouldn’t be the one issue within the EV slowdown. The market is experiencing rising pains as early adopters are at saturation and producers look to penetrate the following layer of potential consumers.

Technical points round battery vary and infrastructure for charging are additionally being addressed, and a few conventional carmakers are refocusing efforts on hybrid autos over absolutely battery-powered fashions.

But the pullback in demand amongst EVs and different big-ticket objects speaks to a extra discerning shopper who’s starting to really feel the chew of upper charges and prioritize purchases.

A significant house enchancment chain, for instance, famous that the buyer remains to be “wholesome” and “engaged” ― however in smaller initiatives at this juncture.

As basic inventory pickers, we need to establish these corporations greatest positioned to climate a possible consumption slowdown as consumers develop extra discriminating of their spending.

Backside line

We anticipate a slowdown within the blockbuster tech-plus earnings alongside a pick-up within the fee of earnings progress in these areas of the market the place COVID hangover results are nonetheless being labored off.

Dispersion in earnings is clear between and inside sectors as corporations regulate to a brand new period of upper charges and volatility.

This, we consider, creates a fertile searching floor for lively inventory pickers to supply larger alpha alternatives in an surroundings the place we consider beta, or market return, may underwhelm expectations.

This put up initially appeared on the iShares Market Insights.

[ad_2]

Source link

(NYSE:CB)")

")

")

")

: Cold Climate, Warming Sentiment")

")

{kind=link}