[ad_1]

Solskin

Funding Thesis

Teladoc (NYSE:TDOC) is about to report its Q2 2024 outcomes subsequent week, Wednesday, after hours.

Having been bearish on Teladoc inventory for a while, I now now not imagine it is sensible to maintain this bearish outlook. Whilst I acknowledge that Teladoc immediately operates as a shadow of its former self, I however contend that this perception has already been priced into its inventory.

At roughly 5x subsequent 12 months’s free money circulation, there’s a higher risk-reward than there’s been in fairly a while. Subsequently, I now change my thoughts and improve my ranking from a promote to a impartial stance. Whilst I begin to flip optimistic concerning the future.

Speedy Recap

Again in February, I mentioned,

I need to be clear, that the issue with Teladoc shouldn’t be that the inventory is dear. Certainly, I make it clear that paying 13x ahead free money flows shouldn’t be costly.

Somewhat, the issue right here is that this enterprise’ progress charges have petered out as Teladoc strikes to the ex-growth a part of its cycle.

Parts that have been beforehand a vexing detraction, corresponding to its elevated stock-based compensation will now acquire a lifetime of themselves.

I imagine that within the subsequent twelve months, buyers will look again to $16 per share as a excessive value to aspire in the direction of.

All in all, I like to recommend promoting TDOC inventory.

Creator’s work on TDOC

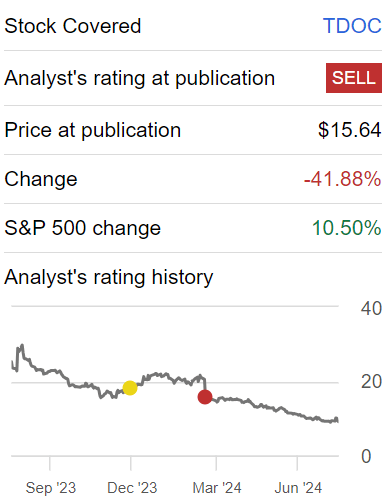

Since I issued a promote on TDOC, the inventory has dropped 42%, underperforming the S&P500 by almost 50 proportion factors in a number of months. A terrific name, I am assured you may agree. And now, here is why I’ve modified my thoughts.

Teladoc’s Close to-Time period Prospects

Teladoc supplies digital healthcare providers, connecting sufferers with healthcare professionals via on-line platforms. They provide a spread of providers, together with major care and psychological well being help, geared toward delivering care with out the necessity for in-person visits. Teladoc seeks to make healthcare extra handy for sufferers.

Nonetheless, Teladoc faces challenges, in sustaining progress (extra on this quickly). What’s extra, Teladoc is in a interval of transition, beneath its new CEO whereas making certain that strategic initiatives proceed with out disruption. We are going to undoubtedly hear extra about Teladoc’s CEO’s plans in its upcoming earnings name.

This management change comes at a essential time as the corporate goals to speed up progress, which requires sturdy management to regain investor confidence.

Moreover, Teladoc should navigate the complexities of integrating new shoppers and sustaining excessive enrollment charges of their continual care applications, all of the whereas managing the operational and strategic shifts that include a brand new management method.

Furthermore, Teladoc’s BetterHelp phase, which focuses on psychological well being providers, has been beneath stress with declining revenues and challenges in consumer acquisition prices. The corporate has seen a decline in paying customers and has needed to alter its promoting methods to stability progress and profitability.

Given this context, let’s now delve into the primary bearish argument dealing with Teladoc.

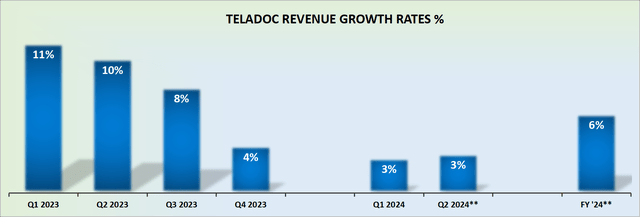

Income Progress Charges Average to Mid-Single Digits

TDOC income progress charges

The graphic above depicts the onerous fact — Teladoc is now not a progress firm. This can be a firm that’s more likely to see some acceleration on its topline within the again half of 2024, however that is easy since its comparables out of the blue ease up.

Because it stands, I believe that Teladoc’s progress charges will average to the mid-single digits, within the medium time period.

Consequently, I like to recommend that buyers don’t overly obsess with the share value chart, and ponder and deliberate over the place the share value was final 12 months and value anchor to the place it might return in time.

Actually, one among my prime bits of recommendation for my mates and followers isn’t to have a look at the place the share value was as a sign of the place it might go. This performs out in additional methods than one. However suffice it to say, finally, the share value will approximate the expectations that free money circulation will head in the direction of. And every little thing else is a distraction. With this in thoughts, let’s focus on its valuation.

TDOC Inventory Valuation — 5x Free Money Movement

Teladoc makes the case that by 2025, it is going to be on a path in the direction of roughly $450 million of EBITDA. Of that determine, roughly talking, $150 million will likely be plowed again as both capex or capitalized software program.

Subsequently, in one of the best case, Teladoc guarantees buyers about $300 million of free money circulation subsequent 12 months. That is the carrot for buyers.

This leaves Teladoc priced at 5x free money circulation. Sure, I acknowledge that Teladoc carries roughly $1.5 billion of convertible notes. And sure, its stability sheet additionally has different pesky minimal liabilities laying declare to its $1.1 billion of money and equivalents.

Nonetheless, when all is claimed and executed, its stability sheet, whereas removed from blemish-free, is not in such a nasty state that it may well’t be repaired with a little bit time and concrete focus.

Therefore, beneath this consideration, whilst I acknowledge that Teladoc has a number of obstacles that it should overcome to stabilize its operations, I can now not maintain a promote ranking on its inventory. Thus, I am now impartial.

The Backside Line

In conclusion, paying 5x ahead free money circulation for Teladoc is already pricing in a mess of unfavourable components, together with its moderated progress charges, management transitions, and challenges inside its BetterHelp phase.

This valuation means that the market has already accounted for the corporate’s present operational hurdles and its journey from a progress inventory to a extra mature section.

With Teladoc’s stability sheet being manageable and its future free money circulation projections indicating potential stability, the inventory presents a extra balanced risk-reward profile than beforehand. Subsequently, sustaining a bearish outlook appears unwarranted at this juncture.

In essence, it seems that Teladoc’s valuation has gone via fairly a “check-up” already and is now more healthy.

[ad_2]

Source link