[ad_1]

The Impression of Methodological Decisions on Machine Studying Portfolios

Research utilizing machine studying methods for return forecasting have proven appreciable promise. Nevertheless, as in empirical asset pricing, researchers face quite a few selections round sampling strategies and mannequin estimation. This raises an necessary query: how do these methodological selections impression the efficiency of ML-driven buying and selling methods? Current analysis by Vaibhav, Vedprakash, and Varun demonstrates that even small selections can considerably have an effect on total efficiency. It seems that in machine studying, the outdated adage additionally holds true: the satan is within the particulars.

This simple paper is a superb reminder that methodological selections in machine studying (ML) methods (similar to utilizing EW or VW weighting, together with micro caps, and so on.) considerably impression the outcomes. It’s essential to think about these selections like conventional cross-sectional issue methods, and practitioners similar to portfolio managers ought to all the time maintain this in thoughts earlier than deploying such a method.

The novel integrations of AI (synthetic intelligence) and deep studying (DL) methods into asset-pricing fashions have sparked renewed curiosity from academia and the monetary trade. Harnessing the immense computational energy of GPUs, these superior fashions can analyze huge quantities of monetary knowledge with unprecedented velocity and accuracy. This has enabled extra exact return forecasting and has allowed researchers to deal with methodological uncertainties that have been beforehand tough to handle.

Outcomes from greater than 1152 alternative mixtures present a sizeable variation within the common returns of ML methods. Utilizing value-weighted portfolios with dimension filters can curb portion of this variation however can not remove it. So, what’s the resolution to non-standard errors? Research in empirical asset pricing have proposed numerous options. Whereas Soebhag et al. (2023) counsel that researchers can present outcomes throughout main specification selections, Walter et al. (2023) argue in favor of reporting all the distribution throughout all specs.

Whereas the authors of this paper agree with reporting outcomes throughout variations, it’s clever to advise in opposition to a one-size-fits-all resolution for this subject. Regardless of an intensive computation burden, It’s doable to compute and report all the distribution of returns for characteristic-sorted portfolios, as in Walter et al. (2023). Nevertheless, when machine studying strategies are used, documenting distribution as an entire will possible impose an excessive computational burden on the researcher. Though a whole distribution is extra informative than a partial one, the prices and advantages of each selections must be evaluated earlier than giving generalized suggestions.

What are extra methods to manage for methodological variation whereas imposing a modest burden on the researcher? Widespread suggestions favor first figuring out high-impact selections (e.g., weighting and dimension filters) on a smaller-scale evaluation. Researchers can then, on the very least, report variations of outcomes throughout such high-priority specs whereas retaining the remaining non-obligatory.

Authors: Vaibhav Lalwani, Vedprakash Meshram, and Varun Jindal

Title: The impression of Methodological selections on Machine Studying Portfolios

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4837337

Summary:

We discover the impression of analysis design selections on the profitability of Machine studying funding methods. Outcomes from 1152 methods present that appreciable variation is induced by methodological selections on technique returns. The non-standard errors of machine-learning methods are sometimes increased than the usual errors and stay sizeable even after controlling for some high-impact selections. Whereas eliminating micro-caps and utilizing value-weighted portfolios reduces non-standard errors, their dimension continues to be quantitatively corresponding to the standard customary errors.

As all the time, we current a number of thrilling figures and tables:

Notable quotations from the tutorial analysis paper:

“[T]right here is ample proof that implies that researchers can use ML instruments to develop higher return forecasting fashions. Nevertheless, a researcher must make sure selections when utilizing machine studying in return forecasting. These selections embrace, however aren’t restricted to the dimensions of coaching and validation home windows, the result variable, knowledge filtering, weighting, and the set of predictor variables. In a pattern case with 10 resolution variables, every providing two resolution paths, the whole specification are 210, i.e. 1024. Accommodating extra complicated selections can result in hundreds of doable paths that the analysis design might take. Whereas most research combine some degree of robustness checks, maintaining with all the universe of prospects is just about unimaginable. Additional, with the computationally intensive nature of machine studying duties, this can be very difficult to discover the impression of all of those selections even when a researcher needs to. Subsequently, a few of these calls are normally left to the higher judgment of the researcher. Whereas the sensitivity of findings to even apparently innocent empirical selections is well-acknowledged within the literature1, we’ve got solely very not too long ago begun to acknowledge the dimensions of the issue at hand. Menkveld et al. (2024) coin the time period to Non-standard errors to indicate the uncertainty in estimates as a consequence of totally different analysis selections. Research like Soebhag et al. (2023) and Walter et al. (2023), and Fieberg et al. (2024) present that non-standard errors might be as giant, if not bigger than conventional customary errors. This phenomenon raises necessary questions in regards to the reproducibility and reliability of monetary analysis. It underscores the necessity for a probably extra systematic method to the selection of methodological specs and the significance of transparency in reporting analysis methodologies and outcomes. As even seemingly innocuous selections can have a major impression on the ultimate outcomes, until we conduct a proper evaluation of all (or not less than, most) of the design selections collectively, it will likely be laborious to know which selections matter and which don’t by pure instinct.Even in asset-pricing research that use single attribute sorting, there are literally thousands of alternatives (Walter et al. (2023) use as many as 69,120 potential specs). Extending the evaluation to machine learning-based portfolios, the doable checklist of selections (and their doable impression) additional expands. Machine-learning customers must make many extra selections for modeling the connection between returns and predictor traits. With the variety of machine studying fashions out there, (see Gu et al. (2020) for a subset of the doable fashions), it will not be unfair to say that students within the subject are spoilt for selections. As argued by Harvey (2017) and Coqueret (2023), such a lot of selections would possibly exacerbate the publication bias in favor of constructive outcomes.

Curiosity in functions of Machine studying in Finance has grown considerably within the final decade or so. For the reason that seminal work of Gu et al. (2020), many variants of machine studying fashions have been used to foretell asset returns. Our second contribution is to this rising physique of literature. That there are various selections whereas utilizing ML in return forecasting is properly understood. However are the variations between specs giant sufficient to warrant warning? Avramov et al. (2023) reveals that eradicating sure kinds of shares significantly reduces the efficiency of machine studying methods. We increase this line of thought utilizing a broader set of selections that embrace numerous concerns that hitherto researchers might need ignored. By offering a big-picture understanding of how the efficiency of machine studying methods varies throughout resolution paths, we conduct a sort of large-scale sensitivity evaluation of the efficacy of machine studying in return forecasting. Moreover, by systematically analyzing the results of assorted methodological selections, we are able to perceive which components are most infuential in figuring out the success of a machine learning-based funding technique.

To summarise, we discover that the alternatives concerning the inclusion of micro-caps and penny shares and the weighting of shares have a major impression on common returns. Additional, a rise in sampling window size yields increased efficiency, however giant home windows aren’t wanted for Boosting-based methods. Based mostly on our outcomes, we argue that financials and utilities shouldn’t be excluded from the pattern, not less than not when utilizing machine studying. Sure methodological selections can scale back the methodological variation round technique returns, however the non-standard errors stay sizeable.

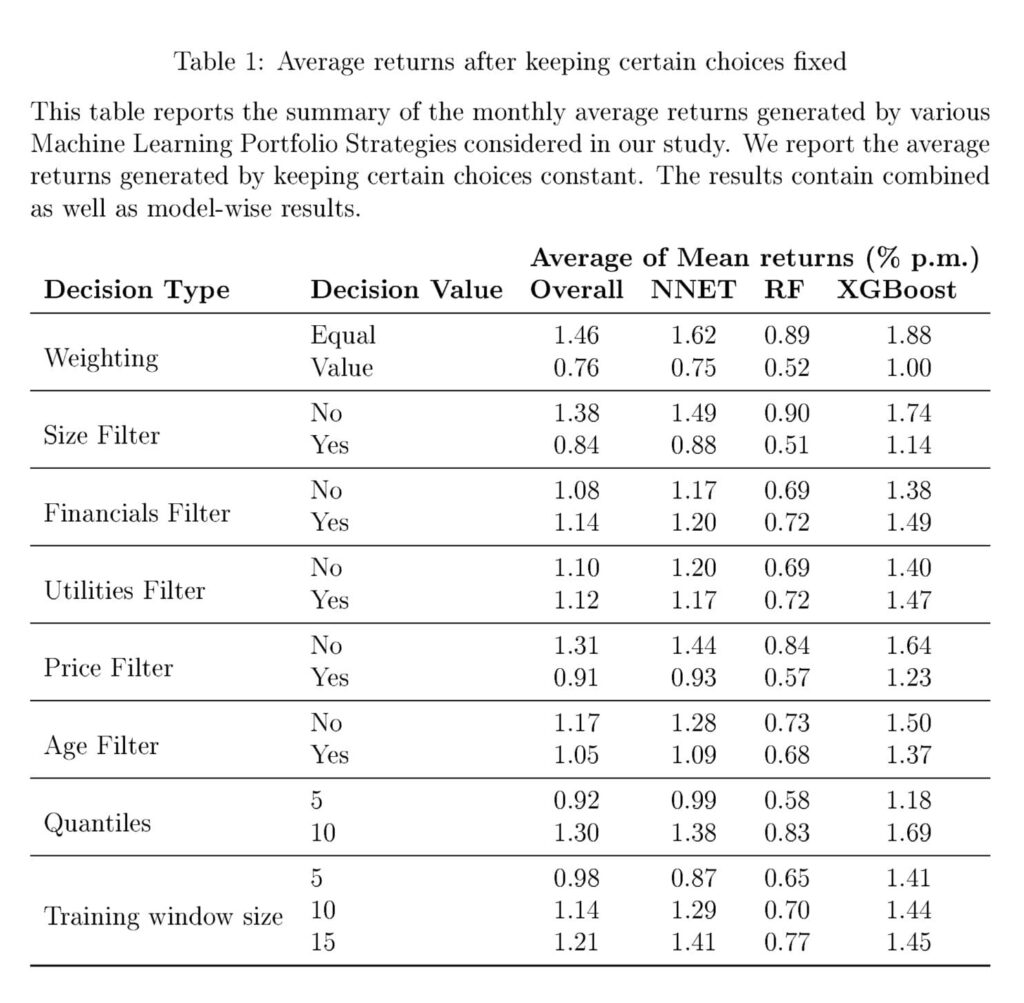

Determine 1 reveals the distribution of returns throughout numerous specs. We observe a non-trivial variation within the month-to-month common returns noticed throughout numerous selections. The variation seems to be a lot bigger for equally-weighted portfolios in comparison with value-weighted portfolios, a end result we discover fairly intuitive. The determine additionally factors in direction of just a few giant outliers. It will be attention-grabbing to additional analyze if these excessive values are pushed by sure specification selections or are random. The variation in returns might be pushed by the selection of the estimator. Research like Gu et al. (2020) and Azevedo et al. (2023) report important variations between returns from utilizing totally different Machine Studying fashions. Subsequently, we plot the return variation after separating fashions in Determine 2. Determine 2 makes it obvious that there’s a appreciable distinction between the imply returns generated by totally different ML fashions. In our pattern, Boosted Timber obtain the most effective out-of-sample efficiency, intently adopted by Neural Networks. Random Forests seem to ship a lot decrease efficiency in comparison with the opposite two mannequin varieties. Additionally, Determine 2 reveals that the general distribution of efficiency is comparable for uncooked returns in addition to Sharpe Ratios. Subsequently, for the remainder of our evaluation, we take into account long-short portfolio returns as the usual metric of portfolio efficiency.All in all, there’s a substantial variation within the returns generated by long-short machine studying portfolios. This variation is impartial of the efficiency variation as a consequence of alternative of mannequin estimators. We now shift our focus towards understanding the impression of particular person selections on the common returns generated by every of the specs. Subsequently, we estimate the common of the imply returns for all specs whereas retaining sure selections mounted. These outcomes are in Desk 1.The leads to Desk 1 present that some selections impression the common returns greater than others. Equal weighting of shares within the pattern will increase the common returns. So does the inclusion of smaller shares. The inclusion of monetary and utilities seems to have a barely constructive impression on the general portfolio Efficiency. Identical to a dimension filter, the exclusion of low-price shares tends to cut back total returns. Additional, grouping shares in ten portfolios yields higher efficiency in comparison with quintile sorting. On common, bigger coaching home windows look like higher. Nevertheless, this appears to be true largely for Neural Networks. For Neural Networks, the common return will increase from 0.87% to 1.41% per thirty days. For enhancing, the acquire is from 1.41% to 1.45%. XGBoost works properly with simply 5 years of knowledge. It takes not less than 15 years of knowledge for Neural Networks to realize the identical efficiency. Apparently, whereas Gu et al. (2020) and (Avramov et al., 2023) each use Neural Networks with a big increasing coaching window, our outcomes present that comparable efficiency might be achieved with a a lot smaller knowledge set (however with XGBoost). Lastly, the method of retaining solely shares with not less than two years of knowledge reduces the returns, however as mentioned, this filter makes our outcomes extra relevant to real-time traders.”

Are you searching for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to study extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing provide.

Do you wish to study extra about Quantpedia Professional service? Test its description, watch movies, overview reporting capabilities and go to our pricing provide.

Are you searching for historic knowledge or backtesting platforms? Test our checklist of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a buddy

[ad_2]

Source link

, Boeing (NYSE:BA)")

{kind=link}