[ad_1]

Buying and selling Arbitrage Portfolios Based mostly on Picture Representations

Convolutional neural networks (CNNs), impressed by the human mind’s capacity to acknowledge visible patterns, excel in duties like object detection, facial recognition, and picture classification, making them highly effective instruments for extracting insights from visible information. Nevertheless, we’re merchants, so a pure query arises: Can we use that in buying and selling? A latest paper reveals that we are able to truly do it. Using CNNs, Niklas Paluszkiewicz introduces a novel strategy to pairs buying and selling by visually analyzing historic worth actions whereas changing conventional time sequence information into picture representations.

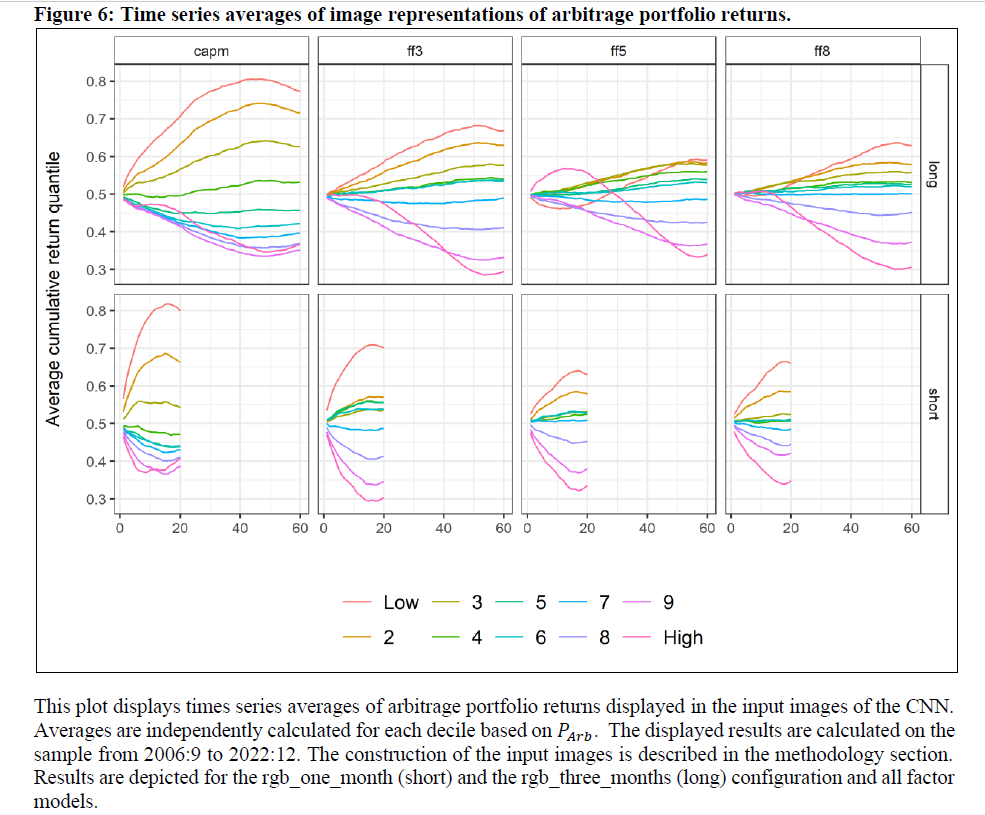

Pair buying and selling methods revenue from worth variations between comparable securities by taking reverse positions and ready for the costs to converge. The creator creates indicators for buying and selling through the use of CNNs to investigate pictures of cumulative residuals, that are returns not associated to systematic danger components. The CNN estimates the likelihood of upward actions throughout numerous hedge portfolios. Based mostly on these possibilities, portfolios are constructed by taking lengthy positions in excessive predicted possibilities and brief positions in these with low predicted possibilities. In keeping with the evaluation, the best risk-adjusted returns are achieved based mostly on three months’ pictures. General, this paper contributes to the rising use of other information representations in monetary forecasting, demonstrating the effectiveness of image-based evaluation for creating worthwhile buying and selling methods.

Authors: Niklas Paluszkiewicz

Title: From Pixels to Income: Buying and selling Arbitrage Portfolios based mostly on Picture Representations

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4612557

Summary:

This paper explores a novel strategy to statistical arbitrage by using Convolutional Neural Networks (CNNs) to foretell directional shifts in extra returns of arbitrage portfolios, that are constructed based mostly on multifactor fashions. Utilizing picture representations of historic return co-movements to establish nonlinear predictive relationships, the research applies CNNs to extract related geometrical return patterns from the information. The empirical outcomes illustrate that the proposed image-based arbitrage methods yield vital extra returns, which aren’t defined by widespread danger components. Additional investigations into the sources of those extra returns – specifically omitted issue momentum, leverage and margin constraints, and lottery demand – don’t conclusively account for the noticed income.

As at all times we current a number of attention-grabbing figures:

Notable quotations from the tutorial analysis paper:

„Following the monetary literature on risk-based asset pricing fashions, the return of a safety could be decomposed into systematic and idiosyncratic elements. The systematic portion could be estimated by linear regression, the place the return sequence of the safety is regressed towards the returns of the danger components within the mannequin. The idiosyncratic half is given by the residuals of this regression, that are orthogonal to the danger components and, if the issue mannequin is correctly specified, they need to carry no danger premium, i.e., the unconditional imply of those residuals is zero. Because of the inherent idiosyncratic danger, the cumulative residuals over a interval might fluctuate round this worth, however ought to ultimately converge to their imply. In what follows, I assemble tradable arbitrage portfolios based mostly on residuals which are ex ante unrelated to systematic danger. The purpose of this strategy is to establish indicators within the time sequence of cumulative residuals to foretell the change within the subsequent interval.

Predicting the change within the residuals is similar as predicting the motion of the underlying arbitrage portfolio, which is captured by the unfold between the return on the safety and the hedge portfolio, i.e. the systematic return element. The convolutional neural community is subsequently used to supply a likelihood estimate of upward actions within the area of all attainable hedge portfolios. From these likelihood estimates, portfolios are created by going lengthy in such portfolios with excessive estimated possibilities and brief in these with low estimated possibilities.

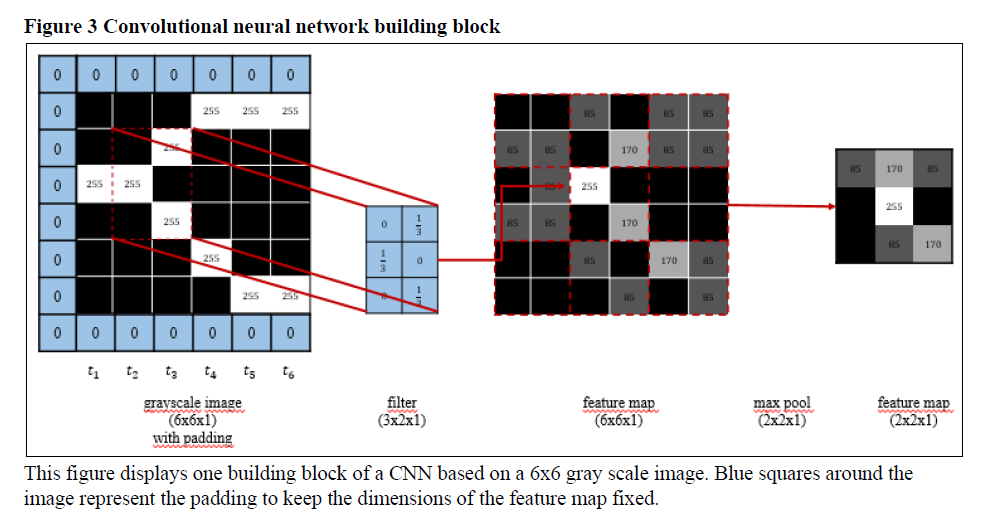

The motivation behind reworking time sequence information to pictures is threefold: First, Convolutional Neural Networks (CNNs) have proven nice success within the laptop imaginative and prescient literature within the latest previous for which their efficiency is described as “superhuman” (He et al. (2015)…. Second, neural networks are impressed by the human mind, which is adept at shortly figuring out geometrical patterns…. Third, reworking information into pictures standardizes the information in a gridlike construction. The method of scaling and normalizing time sequence information can doubtlessly lower noise and improve comparability of the information throughout a number of cases, thereby facilitating sample recognition.

The unfold between the inventory and the hedge portfolio is predicted through the use of a CNN. The enter to the CNN consists of pictures composed of day by day time sequence information of the inventory, the hedge portfolio, and the unfold. Every picture is generated by stacking particular person time sequence information on prime of one another, making a three-channel picture. The CNN is educated to establish patterns and correlations inside the enter time sequence which are related to foretell the likelihood of the unfold to be increased than the cross-sectional median throughout shares within the subsequent interval. Utilizing a CNN has the benefit that it will probably mechanically be taught options from the prediction activity with out requiring express function engineering. By sustaining the construction of the enter pictures, a CNN can exploit spatial info such because the orientation and relational positioning of objects inside the picture.

Particularly, the evaluation reveals that the best risk-adjusted returns are achieved on the premise of three months’ pictures, suggesting that these configurations higher seize complicated return dynamics.

In abstract, the research supplies convincing proof of the potential of CNN in predicting the efficiency of arbitrage portfolios based mostly on inventory residuals. It additionally highlights the restricted function of issue momentum, margin and leverage constraints and lottery demand in driving these portfolios.“

Are you searching for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you need to be taught extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you need to be taught extra about Quantpedia Professional service? Test its description, watch movies, assessment reporting capabilities and go to our pricing supply.

Are you searching for historic information or backtesting platforms? Test our checklist of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConfer with a buddy

[ad_2]

Source link

, Boeing (NYSE:BA)")

{kind=link}