[ad_1]

anilakkus

One of many key headwinds for the oil market this 12 months was the opportunity of a coordinated Strategic Petroleum Reserve (“SPR”) launch from the US and China. With this 12 months being a presidential election 12 months, the Biden administration will do no matter it takes to maintain oil costs from shifting larger.

In our April 17 report for subscribers titled, “This Is How I See The Oil Market Enjoying Out For The Relaxation Of 2024.” we wrote within the part on US and China SPR releases the next:

For the time being, US crude storage with SPR has been steadily constructing for 2024, however because the summer time driving season will get began and refinery throughput picks up, US business crude storage will retest the 2022 lows.

And if we’re proper about WTI reaching the structurally larger value vary of $85 to $95, then the Biden administration will absolutely make the most of the US SPR as soon as once more to fight larger oil costs.

Trying on the setup, I feel ~30 million bbls will probably be launched between August to October. Timing-wise, this coupled with the Saudis lowering its voluntary reduce (albeit slowly) will maintain oil costs capped for the 2nd a part of the 12 months.

Quick forwarding to at present, we put the percentages of the Biden administration releasing SPR of ~30 million bbls at 75%+. One key purpose for that’s, primarily based on present US business crude storage projections, we see storage falling to ~400 million bbls by mid-August. At this degree, WTI will probably be buying and selling nearer to $85 to $90/bbl, which is able to immediate a right away response.

Whereas in loads of methods, the SPR launch will probably be depending on oil costs, we expect that is nearly an inevitability, particularly if the incoming storage attracts are wherever near our assumptions.

For readers conscious of our view on this, we expect you must begin baking in an SPR launch beginning in August to November.

Why do the Saudis have the higher hand?

Following the OPEC+ assembly earlier this month, my preliminary ideas following the announcement had been that there will probably be no US SPR launch coming this 12 months. That is what I wrote:

Our base case view coming into 2024 was that the Saudis would begin to unwind their manufacturing reduce by H2 2024 attributable to 1) tight market balances and a couple of) US presidential election. Whereas we’ve got seen heaps of feedback stating that the Saudis hate the Biden administration, the fact is that with out the US, Saudis lack the navy functionality to defend themselves. Consequently, the US at all times holds the stronger hand in terms of negotiating.

However due to the gradual taper in voluntary manufacturing reduce publish Q3, we not count on the Biden administration to launch ~30 million bbls of SPR.

Indirectly, the way in which the Saudis structured this deal prevents a significant response from the US, which is extremely desired.

Quick forwarding to at present, I’m not so sure anymore. It seems to me that the OPEC+ announcement of progressively rising manufacturing post-Q3 was extra of a strategic transfer than one designed to please the Biden administration.

From a timing perspective, if the Biden administration needs to hit oil costs forward of the U.S. presidential election, then it has to begin releasing SPR between August and September. And since OPEC+ will not be assembly till the tip of September to finalize the voluntary reduce discount for This fall, it’s going to have the higher hand.

If the US decides to launch SPR, then OPEC+ can merely lengthen the voluntary manufacturing cuts for an additional quarter to offset the SPR. If the US decides to not launch SPR and oil market fundamentals are meaningfully tighter, then it may keep on the trail it has at present guided to. Both means, it is a win-win for OPEC+ or the Saudis.

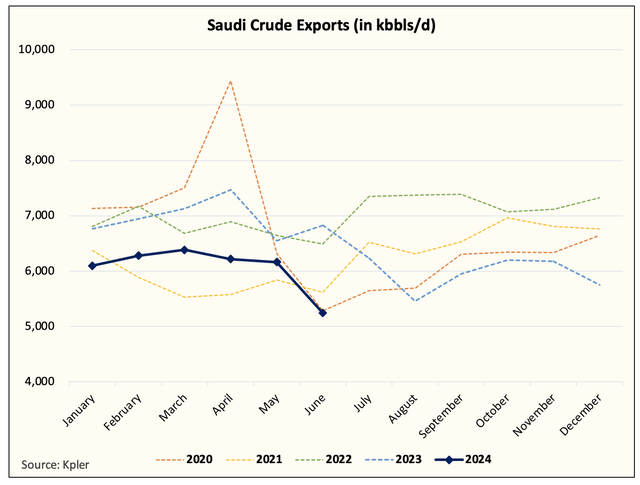

As well as, one more reason why I do not suppose the OPEC+ deal was made to appease the US is the present month-to-date crude export figures from the Saudis:

Kpler

At ~5.2 million b/d, Saudi crude exports are beneath that of 2020. Whereas we do not suppose this would be the finalized determine, it’s positively going to be decrease than ~6.2 million b/d (decrease than final month).

Consequently, we do suppose the Saudis are severe about pushing oil costs larger. If it was making an attempt to appease the US, then we might have seen exports keep flat or transfer larger as we go into H2 2024.

Maybe that is additionally a purpose why over the weekend, Amos Hochstein, an in depth power advisor to President Biden, mentioned:

We are going to do every thing we will to ensure that the market is equipped properly sufficient to make sure as low a value as doable for American shoppers.

Such a remark from an in depth advisor alerts to me that they’ll launch SPR in August.

However fortunately, the Saudis can have the higher hand from a timing perspective.

Oil Upside Capped

From an oil buying and selling perspective, we do not see the opportunity of a value spike this 12 months. As I’ve mentioned because the begin of this 12 months, oil will probably be vary sure, however at a structurally larger degree. Trying on the present value vary, the drop to $72 seems to have been a significant anomaly, and we’re again to the $77 to $85 vary. I feel this can proceed to carry, and solely within the case of oil demand stunning to the upside will we see WTI attain $90/bbl. Exterior this situation or some main provide outage, we do not see this taking place.

The mix of SPR launch from the US and China later this 12 months ought to cap the oil value upside. For power buyers, that is welcomed information, as the opportunity of costs going up and destroying oil demand will probably be a low-probability occasion. Power corporations, in the meantime, will proceed to generate excessive free money move yields, which ought to go in the direction of rewarding shareholders through dividends or share buybacks.

[ad_2]

Source link