[ad_1]

Alvin Man/iStock Editorial by way of Getty Photographs

I not too long ago lined Aukland Airport and from there it is just a small step to additionally cowl Air New Zealand. It ought to be stored in thoughts that this can be a fully totally different enterprise in comparison with airports which for my part have a decrease danger profile. So, Air New Zealand would be the topic of this report through which I’ll focus on the latest earnings, the dangers and alternatives and supply a inventory worth goal in addition to a score for the inventory.

Air New Zealand: Challenges To Revenues And Prices

Air New Zealand

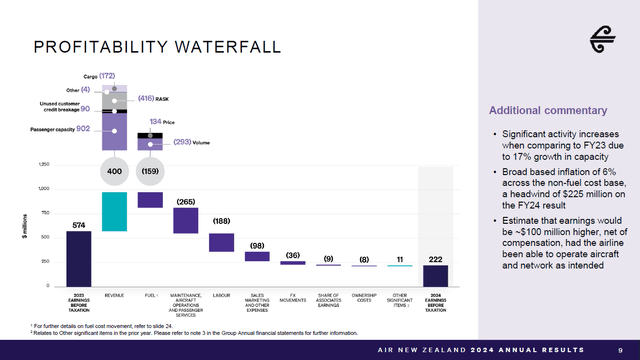

The chart with the profitability waterfall is one thing that I do love, as a result of it fairly clearly exhibits how any adjustments in profitability attributable to revenues stacked towards prices in comparison with final 12 months. Whole revenues climbed 7% to $6.75 billion NZD on a 17% improve in cargo and passenger capability. Passenger revenues elevated 11% to $5.9 billion NZD on a 23% improve in passenger capability, exhibiting that a lot of the capability progress was offset by weakening in unit revenues. Passenger unit revenues decreased 11%. Cargo revenues declined 27% to $459 million NZD whereas contract providers and different revenues remained kind of secure. This led a $400 million NZD raise to EBIT. Nonetheless, this was totally offset by increased gas prices pushed by increased consumption and better pricing, and better working prices together with upkeep and labor in addition to increased gross sales prices leading to EBIT to say no 61% to $222 million NZD. Resulting from plane supply delays, there was a $100 million NZD impression on the earnings.

On unit income decline of 11% decline in unit revenues excluding breakage of buyer credit, the unit prices declined by 1.6% and elevated by 0.6% on adjusted foundation which excludes gas worth actions, international alternate charges and third-party upkeep to point out the working price effectivity with unit prices with solely the gas prices excluded elevated 6%. So, what the outcomes of Air New Zealand confirmed is what we see with many airways and that’s vital capability additions to stay aggressive with different airways thereby eroding unit revenues.

What Are The Dangers And Alternatives For Air New Zealand?

The dangers and alternatives are the identical for Air New Zealand as they’re for different airways. The chance to the highest line is the continued weakening in unit revenues with out benefiting from higher fastened price absorption as prices within the trade base stay elevated. Moreover, fluctuations in gas costs pose a danger in addition to continued delays in deliveries of latest fuel-efficient airplanes. Any reversal of that danger would clearly present a chance for enhancing outcomes or on the very least for the margins to be much less pressured.

Air New Zealand Inventory Is A Promote

The Aerospace Discussion board

To find out multi-year worth targets The Aerospace Discussion board has developed a inventory screener which makes use of a mixture of analyst consensus on EBITDA, money flows and the latest steadiness sheet knowledge. Every quarter, we revisit these assumptions, and the inventory worth targets accordingly. In a separate weblog I’ve detailed our evaluation methodology.

I don’t take into account Air New Zealand inventory enticing for funding as EBITDA is predicted to lower additional in FY25 and free money move is predicted to be detrimental within the coming two years, which I imagine would require the corporate to borrow cash whereas the demand surroundings stays difficult and working prices are elevated. None of this makes for a compelling risk-reward profile and I mark the inventory a promote.

Conclusion: Air New Zealand Holds Little Worth

The outcomes that Air New Zealand posted for FY24 clearly confirmed the pressures on unit revenues and an incapability to meaningfully cut back unit prices whereas dramatically rising capability. Within the years forward, we don’t see EBITDA get well considerably till FY26 and within the meantime the corporate will seemingly must borrow extra money to fund the CapEx. Because of this, I don’t see a compelling funding case for Air New Zealand inventory.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.

In order for you full entry to all our stories, knowledge and investing concepts, be a part of The Aerospace Discussion board, the #1 aerospace, protection and airline funding analysis service on Searching for Alpha, with entry to evoX Knowledge Analytics, our in-house developed knowledge analytics platform.

[ad_2]

Source link